What Is Single Entry System In Accounting?

The single entry system in accounting is an accounting approach under which every accounting transaction is recorded with only a single entry in the accounting records, centered on the business enterprise’s results, which are shown in the statement of income of the company.

You are free to use this image on your website, templates, etc, Please provide us with an attribution linkHow to Provide Attribution?Article Link to be Hyperlinked

For eg:

Source: Single Entry System in Accounting (wallstreetmojo.com)

The definition of a single entry system specifies the primary use of the process in the manual accounting process by small firms that do not have the financial capability and resources necessary for a full-fledged accounting system. Mainly all the computerized accounting systemsAccounting SystemsAccounting systems are used by organizations to record financial information such as income, expenses, and other accounting activities. They serve as a key tool for monitoring and tracking the company's performance and ensuring the smooth operation of the firm.read more use double-entry accounting.

Table of contents

Key Takeaways

- A single-entry system keeps one side of each transaction and records each transaction as a single entry. Most of the entries used it to populate the revenue statement.

- Small businesses that lack the resources and financial capacity to support a comprehensive accounting system typically employ the single-entry approach in manual accounting processes.

- Contrary to double-entry transactions, which demand expertise, single-entry transactions are straightforward and don’t require in-depth account knowledge. Single-entry systems keep incomplete records, whereas double-entry systems capture both sides of the record.

- It is rather straightforward to understand and put into practice. It doesn’t require specialists; anybody with a working knowledge of accounting or business may implement a single-entry system.

Single Entry System In Accounting Explained

A single entry system records a transaction with a single entry and only maintains one side of every transaction. It is the oldest method of recording financial transactions and is less popular than the double entry systemDouble Entry SystemDouble Entry Accounting System is an accounting approach which states that each & every business transaction is recorded in at least 2 accounts, i.e., a Debit & a Credit. Furthermore, the number of transactions entered as the debits must be equivalent to that of the credits. read more and is mainly used for entries recorded in the income statementIncome StatementThe income statement is one of the company's financial reports that summarizes all of the company's revenues and expenses over time in order to determine the company's profit or loss and measure its business activity over time based on user requirements.read more. This term describes the problems associated with the accounts from an incomplete transaction and is popularly called ‘Preparation of accounts from incomplete records.

The core information involves cash receiptsCash ReceiptsA cash receipt is a small document that works as evidence that the amount of cash received during a transaction involves transferring cash or cash equivalent. The original copy of this receipt is given to the customer, while the seller keeps the other copy for accounting purposes.read more and cash disbursements rather than asset and liability records. The primary form is the cash bookCash BookThe Cash Book is the book that records all cash receipts and payments, including funds deposited in the bank and funds withdrawn from the bank according to the transaction date. All the transaction which is recorded in the cash book has the two sides i.e., debit and credit.read more, an expanded form of the check register. It mainly has columns that record particular sources and uses of cash, starting with the opening balance and ending with the closing balance.

Accounting for Financial Analyst (16+ Hours Video Series)

–>> p.s. – Want to take your financial analysis to the next level? Consider our “Accounting for Financial Analyst” course, featuring in-depth case studies of McDonald’s and Colgate, and over 16 hours of video tutorials. Sharpen your skills and gain valuable insights to make smarter investment decisions.

Features

Some of the features of the single entry system in accounting are as follows:

- It is comparatively simple and easy to implement.

- No professionals are required; resources with a basic understanding of accounting or business can perform a single entry system.

- This type of accounting suits small firms at the starting stage and startups.

- Income and expenses are accounted for daily.

- Only limited accounts are opened since all the transactions related to personal accounts are recorded relating to personal and real accounts.

- As mentioned in the previous point, limited accounts are opened, and the books are scarce, expenses to maintain these accounts are also limited.

- This system is purely based on the income statement. Hence, it becomes easier to determine the profit and loss.

Please note that Profits under this system can only be an estimate and, therefore, cannot necessarily be true and correct.

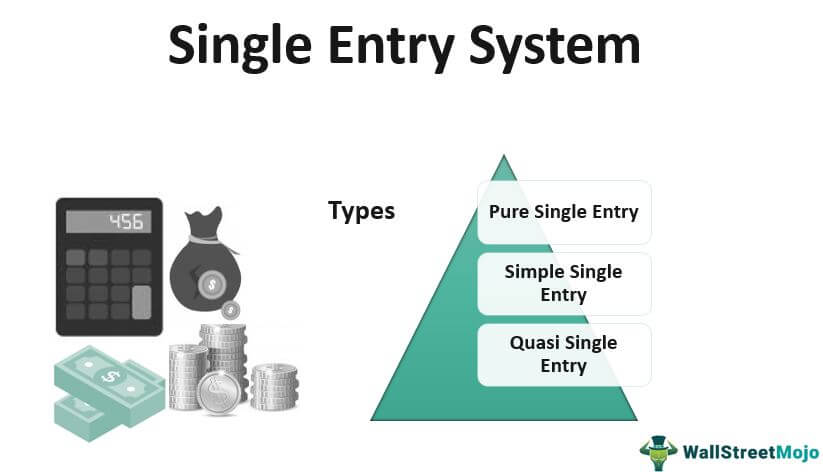

Types

The types of this system include:

You are free to use this image on your website, templates, etc, Please provide us with an attribution linkHow to Provide Attribution?Article Link to be Hyperlinked

For eg:

Source: Single Entry System in Accounting (wallstreetmojo.com)

#1 – Pure Single Entry

No information is available on sales, purchases, and cash and bank balances; only personal accounts are considered. Therefore, this method cannot be used practically since it does not provide cash or daily transaction information.

#2 – Simple Single Entry

This account is kept based on a double-entry system, but only two accounts are considered, i.e., the personal and the cash account. Therefore, entries are made only from these accounts, and no other account is considered.

#3 – Quasi Single Entry

Apart from the personal and cash accounts, other subsidiary accounts are also maintained in this type of accounting. The main ones are sales, purchase accounts, and bill books. Discounts are also recorded in the personal account. Additional vital information like wages, rent, and salaries is also available. This method is adopted as a substitute for a double-entry accounting system.

By looking at the types, we can determine that the single-entry accounting system can be defined as a system that is a mixture of Single-entry double entry and no-entry.

Example

Below is the single entry system in accounting example to show the format of the account book –

| # | Date | Particulars | Revenue | Expenses | Inventory | Payroll |

|---|---|---|---|---|---|---|

| Balance Forward | $20,000 | $5,000 | $7,000 | $3,000 | ||

| 1000 | Jul -18 | Wages | $1,500 | |||

| 1001 | Jul -19 | Utilities | $200 | |||

| 1002 | Jul – 20 | Deposit | $15,000 | |||

| 1003 | Jul – 21 | Goods | $2,000 | |||

| Ending Balance | $35,000 | $5,200 | $9,000 | $4,500 |

It is an inaccurate and unscientific way of recording transactions with no linkage among the transactions or the available information. For example, there is no real and personal accounts record, and the cash book mixes up the business and individual transactions.

Problems

#1 – Assets

This system does not track assets in terms of keeping recording or tracking. Thus, it makes it easier for them to be lost or stolen.

#2 – Audited Statements

The double entry system is necessary for auditing financial statements necessary for the checks and balances of each account. It is impossible to audit statements in a single entry system. Even if one wants to do it, they will have to convert the single entry to double entries and balance it for auditing.

#3 – Increased Risk of Errors

There is no check for other accounts in this system, and they cannot be balanced. This issue makes it more challenging to keep a check or find missing entries and track errors.

#4 – Performance Analysis

Financial position cannot be determined since there is no proper balance sheetBalance SheetA balance sheet is one of the financial statements of a company that presents the shareholders' equity, liabilities, and assets of the company at a specific point in time. It is based on the accounting equation that states that the sum of the total liabilities and the owner's capital equals the total assets of the company.read more maintained and limited information. Therefore, it is difficult for the management to analyze its performance and estimate future metrics.

#5 – Incomplete Records

This system only focuses mainly on those transactions that involve business or transactions with external parties and ignores the other vital transactions that may be necessary to determine the company’s financial position and should have a place in the financial statements.

#6 – Accuracy

Arithmetical accuracy cannot be achieved since this system does not prepare a trial balancePrepare A Trial BalanceTrial Balance is the report of accounting in which ending balances of a different general ledger are presented into the debit/credit column as per their balances where debit amounts are listed on the debit column, and credit amounts are listed on the credit column. The total of both should be equal.read more

Single Entry System In Accounting Vs Double Entry System In Accounting

The major differences between single entry accounting and double entry accounting systems are:

- It can be defined as a system where only one aspect of each transaction is maintained, i.e., either debitDebitDebit represents either an increase in a company’s expenses or a decline in its revenue. read more or credit; on the contrary, in a double method accounting system, both these transactions are recorded, and all the aspects of every transaction are

- Single-entry transactions are simple and do not require detailed knowledge of accounts, whereas double-entry transactions require expertise.

- Incomplete records are maintained in a single entry system, while double-entry captures both the sides and records.

- The single entry system maintains cash accounts and personal accounts, while the double-entry system maintains all kinds of accounts, i.e., real, nominal, and personal.

- Since small firms do not have single financial capabilities and resources, entry accounting is suitable. On the contrary, for large firms, it is necessary to have a double-entry accounting system.

- Frauds and errors are more accessible to identify in a double-entry accounting system than in a single entry system.

- Compared with the double-entry system, a single entry system has no standardization, and there is no uniformity between the different businesses following the same method. Each business maintains accounts as per its convenience and requirements.

Frequently Asked Questions (FAQs)

Single-entry accounting systems are of three types. These include; pure single-entry, where only personal accounts are considered; simple single-entry, wherein personal and cash accounts are created; and quasi-single-entry, wherein cash, personal, and subsidiary accounts are maintained.

The problems of single-entry accounting systems include assets, audited statements, increased risk of errors, performance analysis, incomplete records, and accuracy.

Single-entry transactions are simple and don’t require in-depth account knowledge, unlike double-entry transactions involving experience. In addition, double-entry systems record both sides of the record, whereas single-entry systems only keep one side.

Recommended Articles

This article is a guide to what is Single Entry System in Accounting. Here we explain it with an example, features, problems, vs double entry system, and types. You may also take a look at the below useful accounting article –

Thank you very much