- Stripe: Best for Omnichannel Businesses

- Stax (Fattmerchant): Best for High-Volume Sellers

- Square: Best for Mobile Transactions

- PayPal: Best for Versatility

- Clover: Best for Food Service and Service Providers

- Payment Depot: Best for Lowest Card Processing Rates

- Helcim: Best for Startups and Seasonal Businesses

- Gravity Payments: Best for Niche Industries

- Merchant One: Best for Non-Tech-Savvy Users

- Elavon Payment Processing: Best for Global Businesses

Kelly Main is a Marketing Editor and Writer specializing in digital marketing, online advertising and web design and development. Before joining the team, she was a Content Producer at Fit Small Business where she served as an editor and strategist covering small business marketing content. She is a former Google Tech Entrepreneur and she holds an MSc in International Marketing from Edinburgh Napier University. Additionally, she is a Columnist at Inc. Magazine.

With 20 years of experience, Kiran Aditham has navigated the field in editorial and writing, from working with major pubs like Adweek, AdAge and PSFK to now working at Forbes Advisor.

Kelly Main,

Kelly Main is a Marketing Editor and Writer specializing in digital marketing, online advertising and web design and development. Before joining the team, she was a Content Producer at Fit Small Business where she served as an editor and strategist covering small business marketing content. She is a former Google Tech Entrepreneur and she holds an MSc in International Marketing from Edinburgh Napier University. Additionally, she is a Columnist at Inc. Magazine.

Kiran Aditham

With 20 years of experience, Kiran Aditham has navigated the field in editorial and writing, from working with major pubs like Adweek, AdAge and PSFK to now working at Forbes Advisor.

Jeff Luna's career is a testament to his deep expertise and significant contributions to the fields of payment processing, insurance billing, claims disbursements and SaaS billing and payments. For more than 15 years, starting from his foundational roles at merchant services companies and Allied Business Schools, Jeff has consistently demonstrated an innate ability to navigate the complexities of financial transactions and operational efficiency. His early work laid the groundwork for a profound understanding of the technological and regulatory landscapes that govern these sectors.

Ascending to leadership positions, Luna's role as Sr. VP of Sales & Partnerships at Tranzpay LLC since 2011 has been marked by innovative sales strategies and business development initiatives that have significantly impacted the payment solutions industry. Concurrently, his directorship at NLR Resources Inc. and ownership of JJCS Business Consulting Services have enabled him to influence the operational strategies of numerous businesses, optimizing their billing processes and enhancing their claims disbursements mechanisms. Jeff’s holistic view of the financial services ecosystem, coupled with a strategic approach to business operations, has positioned him as a key figure in transforming traditional billing and payment processes.

Beyond his operational and leadership roles, Jeff’s expertise extends into strategic consulting, where he leverages his comprehensive knowledge to advise companies on optimizing their SaaS billing systems and payment processing frameworks. His insights into the integration of emerging technologies with traditional financial services have made him a sought-after expert for businesses looking to innovate their payment and billing practices. Jeff’s dedication to excellence and his forward-thinking approach have not only advanced his career but also contributed significantly to the evolution of payment and billing solutions across industries.

Ascending to leadership positions, Luna's role as Sr. VP of Sales & Partnerships at Tranzpay LLC since 2011 has been marked by innovative sales strategies and business development initiatives that have significantly impacted the payment solutions industry. Concurrently, his directorship at NLR Resources Inc. and ownership of JJCS Business Consulting Services have enabled him to influence the operational strategies of numerous businesses, optimizing their billing processes and enhancing their claims disbursements mechanisms. Jeff’s holistic view of the financial services ecosystem, coupled with a strategic approach to business operations, has positioned him as a key figure in transforming traditional billing and payment processes.

Beyond his operational and leadership roles, Jeff’s expertise extends into strategic consulting, where he leverages his comprehensive knowledge to advise companies on optimizing their SaaS billing systems and payment processing frameworks. His insights into the integration of emerging technologies with traditional financial services have made him a sought-after expert for businesses looking to innovate their payment and billing practices. Jeff’s dedication to excellence and his forward-thinking approach have not only advanced his career but also contributed significantly to the evolution of payment and billing solutions across industries.

Expert Reviewed

Jeff Luna

Jeff Luna's career is a testament to his deep expertise and significant contributions to the fields of payment processing, insurance billing, claims disbursements and SaaS billing and payments. For more than 15 years, starting from his foundational roles at merchant services companies and Allied Business Schools, Jeff has consistently demonstrated an innate ability to navigate the complexities of financial transactions and operational efficiency. His early work laid the groundwork for a profound understanding of the technological and regulatory landscapes that govern these sectors.

Ascending to leadership positions, Luna's role as Sr. VP of Sales & Partnerships at Tranzpay LLC since 2011 has been marked by innovative sales strategies and business development initiatives that have significantly impacted the payment solutions industry. Concurrently, his directorship at NLR Resources Inc. and ownership of JJCS Business Consulting Services have enabled him to influence the operational strategies of numerous businesses, optimizing their billing processes and enhancing their claims disbursements mechanisms. Jeff’s holistic view of the financial services ecosystem, coupled with a strategic approach to business operations, has positioned him as a key figure in transforming traditional billing and payment processes.

Beyond his operational and leadership roles, Jeff’s expertise extends into strategic consulting, where he leverages his comprehensive knowledge to advise companies on optimizing their SaaS billing systems and payment processing frameworks. His insights into the integration of emerging technologies with traditional financial services have made him a sought-after expert for businesses looking to innovate their payment and billing practices. Jeff’s dedication to excellence and his forward-thinking approach have not only advanced his career but also contributed significantly to the evolution of payment and billing solutions across industries.

Ascending to leadership positions, Luna's role as Sr. VP of Sales & Partnerships at Tranzpay LLC since 2011 has been marked by innovative sales strategies and business development initiatives that have significantly impacted the payment solutions industry. Concurrently, his directorship at NLR Resources Inc. and ownership of JJCS Business Consulting Services have enabled him to influence the operational strategies of numerous businesses, optimizing their billing processes and enhancing their claims disbursements mechanisms. Jeff’s holistic view of the financial services ecosystem, coupled with a strategic approach to business operations, has positioned him as a key figure in transforming traditional billing and payment processes.

Beyond his operational and leadership roles, Jeff’s expertise extends into strategic consulting, where he leverages his comprehensive knowledge to advise companies on optimizing their SaaS billing systems and payment processing frameworks. His insights into the integration of emerging technologies with traditional financial services have made him a sought-after expert for businesses looking to innovate their payment and billing practices. Jeff’s dedication to excellence and his forward-thinking approach have not only advanced his career but also contributed significantly to the evolution of payment and billing solutions across industries.

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors' opinions or evaluations.

Credit card processors are a critical component in processing transactions, whether online, in-store or over the phone. With so many to choose from—and with varying fees, pricing structures, capabilities, ease of use, inclusions and support quality—choosing one for your business is no easy feat. To help, the team at Forbes Advisor analyzed dozens of the leading companies to determine the best credit card processing companies for small business.

Read more

Featured Partners

Advertisement

1

Stax

Free Trial

No

Offers

First Month Free

Pricing

$99 per month, 7 cents to 15 cents per transaction plus interchange rate

2

Finix

Free Trial

No

Offers

Save up to 40% on credit card processing

Pricing

Transparent subscription-based pricing with 0% markup on interchange fees

3

Payment Depot

Free Trial

No

Offers

$0 Setup & No Cancellation Fees

Pricing

Customized Interchange+ Pricing – Rates as low as 0.2% – 1.95%

4

Paysafe

Free Trial

No

Offers

SAVE or get a $200 gift card + FREE payment equipment*

Pricing

Industry-low rates starting at $0.15 batch fee + 0% Cash Discount Plans available

Show Summary

- The Best Credit Card Processing Companies Of 2024

- Forbes Advisor Ratings

- Other Credit Card Processors to Consider

- Methodology

- What Is a Credit Card Processing Company?

- How To Choose the Best Credit Card Processing Company

- How Much Does Credit Card Processing Cost?

- Credit Card Processing Company Pricing Structures

- How to Reduce Your Credit Card Processing Costs

- Credit Card Processing Equipment and Systems

- Frequently Asked Questions (FAQs)

The Best Credit Card Processing Companies Of 2024

Forbes Advisor Ratings

| Company | Forbes Advisor Rating | Free Plan | Monthly Fee | Processing Fees | LEARN MORE | ||||

|---|---|---|---|---|---|---|---|---|---|

| Stripe | 4.8 |  |

Yes | $0 | From 2.9% plus 30 cents per transaction | Learn More | On Stripe's Website | ||

| Stax |  |

4.7 |  |

No | Starting at $99 | From eight cents to 10-plus cents (per transaction, plus interchange rate) | Learn More | On Stax's Website | |

| Square | 4.7 | |

Yes | Free; Premium plans start at $29 per month plus processing fees | From 2.6% plus 10 cents per transaction | Learn More | Via partner site | ||

| PayPal | 4.5 | |

Yes | Free; Premium plans start at $5 | From 1.9% plus 10 cents per transaction | Learn More | Read Forbes' Review | ||

| Clover | 4.4 | |

No | Starting at $14.95 | From 2.3% plus 10 cents per transaction | Learn More | On Clover's Website | ||

| Payment Depot | 4.4 | |

No | Starting at $39 | From 7 cents to 15 cents per transaction, plus interchange rate | Learn More | On Payment Depot's Website | ||

| Helcim | 4.4 | |

Yes | Free | From 1.93% plus 8 cents per transaction | Learn More | On Helcim's Website | ||

| Gravity Payments | 4.3 | |

Yes | Free | From 2.5% plus 10 cents per transaction | Learn More | Read Forbes' Review | ||

| Merchant One | 4.2 |  |

No | Starting at $13.95 | 0.29% to 1.99% based on tier and transaction type | Learn More | On Merchant One's Website | ||

| Elavon | 4.1 | |

No | Custom-quoted | Starts at 1.10% + $0.12 cents per transaction | Learn More | Read Forbes' Review |

Other Credit Card Processors to Consider

- Intuit Payments: From the provider of QuickBooks, Intuit Payments is a high-quality credit card processor that stands out for its pricing transparency, ease of use and accounting connectivity. However, using it requires a QuickBooks online account, which is prohibitive for many users with their own accounting framework in place and its chargeback fee is higher than most at $25.

- National Processing: While National Processing offers competitively priced subscription-based plans with low transaction fees, it is not ideal for small businesses with low sales volume and its termination fee is expensive at up to $595.

- proMerchant: As a provider that stands out for its offering of services to high-risk businesses and top-rated support, it loses marks when it comes to features and usability as it is not as advanced or well-designed as many of its competitors.

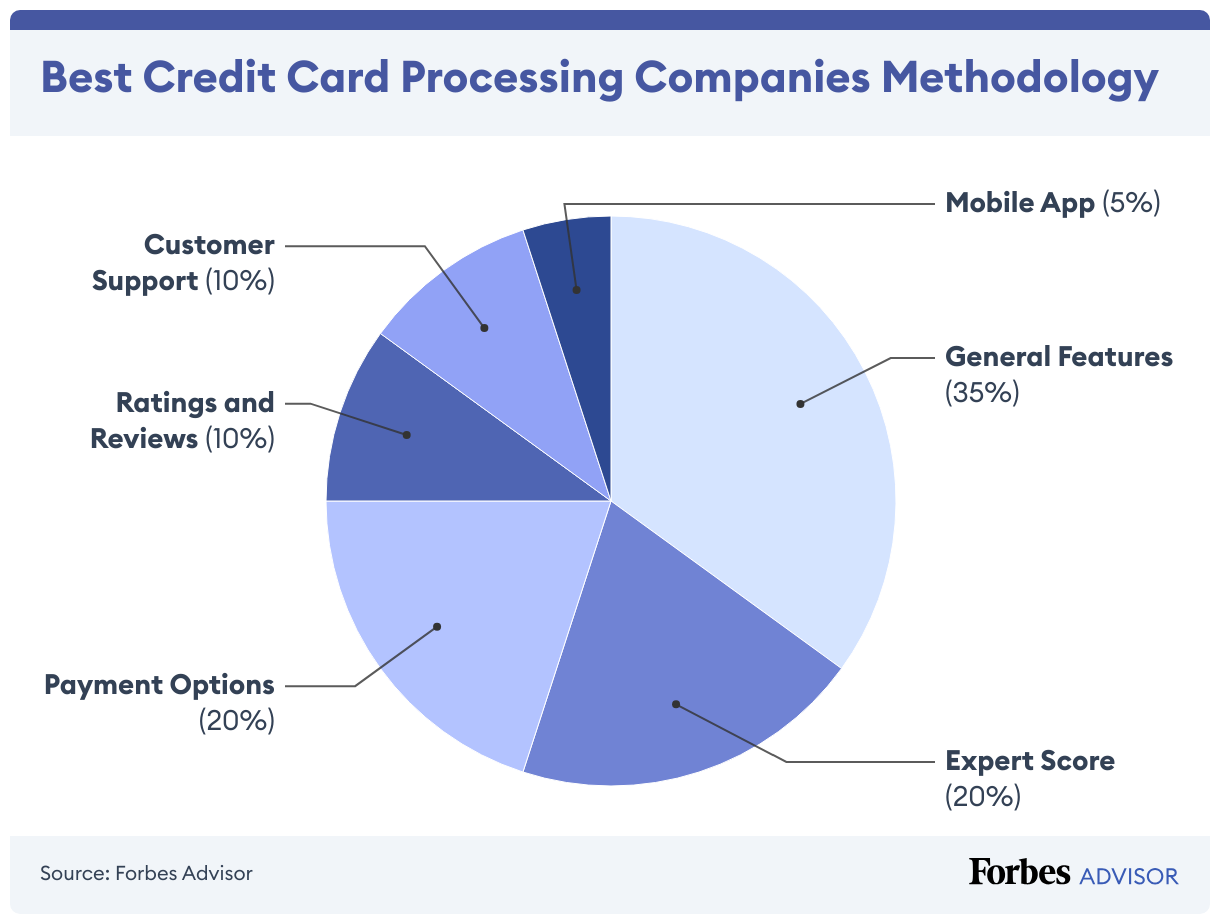

Methodology

| Decision Factor | Scoring Weight | Description |

|---|---|---|

|

Key Features

|

30%

|

Features are key to choosing the right credit card processor, so we analyzed providers based on the availability of key features, such as the inclusion of a reporting dashboard, invoicing, data exports, contactless payments, software integrations, PCI compliance and volume-based discounts.

|

|

Payment Gateways

|

20%

|

The best credit card processors offer a wide array of payment gateways, including: Visa, Mastercard, Discover, American Express, Apple Pay, Google Pay and POS integrations.

|

|

Customer Support

|

10%

|

When in need, support matters so we considered the availability of support, including hours and channels as well as support quality.

|

|

Mobile App

|

5%

|

Providers were analyzed based on whether or not mobile apps were available and their average scores on top app stores.

|

|

Ratings and Reviews

|

10%

|

To gain a deeper understanding of user experience, we analyzed third-party ratings in terms of average score and number of reviews.

|

|

Expert Analysis

|

20%

|

We incorporated our own firsthand experience with qualitative factors such as value for price, ease of use, features and popularity.

|

Read More: How We Test Credit Card Processors

What Is a Credit Card Processing Company?

Credit card processors make it possible for you to take credit card payments by connecting the various services involved in the process. These include credit card networks, issuing banks and your own payment processing account.

When a customer swipes their credit card at a store or pays online, a credit card processing company enables the secure transfer of customer data for payment approval, collects the funds from the issuing bank and deposits those funds to the merchant’s account within one to two business days.

How To Choose the Best Credit Card Processing Company

The best credit card processing for small business should strike the right balance of cost, functionality and support. Processing fees and monthly costs are the obvious starting points when comparing providers. However, considerations such as ease of use, support, integrated sales features and free software can help you spot the best value for your specific needs.

Here are a few questions to keep in mind when you shop for card processing services.

- What is your average sales volume per month? Higher transaction volumes equal lower processing fees. A good rule of thumb is once you reach $10,000 in monthly transactions, you can benefit from an interchange-plus or tiered processing service. Before then, a flat-rate service such as Square, Stripe or PayPal is very economical.

- Do you sell in-person, online, mobile or combined channels? Where you sell determines your processing hardware and system needs. If you sell in-store, you need checkout registers. If you sell on the go, you need mobile card readers and a mobile processing app or mobile POS. If you sell online, you need a secure payment gateway. If you combine sales methods, you need a payment processing service that seamlessly connects all of your sales within an integrated system.

- Do you need free equipment and POS systems? Free equipment and POS software add value to a service, even when paired with higher processing fees. When comparing services, consider what any free perks would cost if you went with a lower-fee processor that doesn’t provide them.

- Do you already have registers, terminals and POS software? A processing service that integrates with registers, terminals, POS systems or accounting software that you already use can save in upfront costs and minimize business interruptions.

- Is your business high-risk? High-risk merchants generally find the lowest fees with traditional merchant accounts with tiered pricing.

- Are you selling restricted items? Many popular card processing services limit what you can sell. If your business falls outside of their approved list, you’ll need a traditional merchant account provider.

- How fast do you need your funds? Virtually all card processing companies deposit funds within one to two business days, but charge an added fee for same-day deposits. If you need quick access to funds, look for a provider that offers this for free.

- Do you need 24/7 support? Most providers offer 24/7 service for network outages and other business-critical events, however, a few limit support at lower plan levels.

- Do you sell globally? You need a processing service that supports international cards and exchange rates.

- Do you use QR codes, payment links and online invoicing? You need a card processing service with an online portal feature that supports these cutting-edge payment methods.

- Do you want to accept e-checks and bank transfers? Look for card processing services that support ACH payments.

- Is your customer data going to be secure? It should go without saying that safely transmitting credit card information to your payment processor needs to be handled securely. Make sure that whatever company you choose adheres to payment card industry (PCI) compliance standards to keep these details safe.

How do I choose the best credit card processing company for my needs?

Jeff Luna

Small Business Expert

Kelly Main

Staff Reviewer

Amy Smith

Staff Reviewer

When selecting a payment processing company, transparency in fees and pricing structures is important. That being said, pricing should be the last thing you compare. More important and critical is the company’s ability to offer robust security measures to protect sensitive payment information to protect you and your customers, as well as support for the latest and emerging payment technologies to meet customer expectations. Shop based on features and needs, then beat them up on the pricing.

Jeff Luna

Small Business Expert

Ultimately, the best credit card processor for you will have the hardware and features you need at a competitive price–but not just price in terms of monthly subscription fees, but in terms of transaction fees. Consider your sales volume and payment type (e..g, online, swipe, keyed-in) and do the math to determine which plan is actually the most affordable as many offer attractive low-cost monthly plans, but these typically have higher transaction fees which can quickly add up.

Kelly Main

Staff Reviewer

There are so many variables that determine which credit card processing company you can choose (sales volume, industry, your credit score, etc.). High-risk industries such as vape shops, telemarketing and entertainment businesses typically don’t have much choice, so it’s best to focus on the features you need and payment types you want to accept. Sometimes an aggregate credit card processor is your best best, but they usually charge higher markups on transaction fees and a monthly fee.

Amy Smith

Staff Reviewer

Featured Partners

Advertisement

1

Stax

Free Trial

No

Offers

First Month Free

Pricing

$99 per month, 7 cents to 15 cents per transaction plus interchange rate

2

Finix

Free Trial

No

Offers

Save up to 40% on credit card processing

Pricing

Transparent subscription-based pricing with 0% markup on interchange fees

3

Payment Depot

Free Trial

No

Offers

$0 Setup & No Cancellation Fees

Pricing

Customized Interchange+ Pricing - Rates as low as 0.2% - 1.95%

4

Paysafe

Free Trial

No

Offers

SAVE or get a $200 gift card + FREE payment equipment*

Pricing

Industry-low rates starting at $0.15 batch fee + 0% Cash Discount Plans available

How Much Does Credit Card Processing Cost?

The cost of credit card processing depends on various types of fees and individual companies’ pricing structures.

Credit Card Processing Fees

Understanding credit card processing fees is important for selecting the appropriate service. These fees typically include:

- Interchange Fees: Set by card brands such as Visa and Mastercard. These base costs of processing credit cards generally range from 1% to 2%. Factors influencing these rates include transaction type (higher for online sales), card type (lower for debit cards) and card brand (varying rates for different brands and card types).

- Processor Markup Fees: Charges by processing companies for their services. Varies based on fee structures such as interchange-plus, tiered rates or flat-rate fees.

- Monthly Fees: For additional services such as online gateways or PCI compliance. Some processors offer no monthly fees but incorporate higher flat-rate processing fees.

- Other Costs: Additional fees to consider include chargeback fees (vary among services), batch processing fees (charged by some providers), setup or termination fees (common in tiered rate plans), monthly minimum fees (if contracted volumes aren’t met) and same-day funding fees (for immediate access to funds).

Read more: Credit Card Processing Fees

Credit Card Processing Company Pricing Structures

Different pricing models cater to varying business needs. Key structures include:

- Flat-Rate Pricing: Offers a single rate for all transactions, typically ranging from 2.5% plus 10 cents to 3.5% plus 30 cents per transaction. Suitable for businesses with lower average transactions, it offers simplicity and often includes free tools such as POS software and card readers. In-person sales generally incur lower fees than online sales, with no variation based on card type or reward programs.

- Interchange-Plus Pricing: Adds a minimal fee to the base interchange rates. For instance, Helcim charges an added percentage and per-transaction fee, without monthly fees. Rates can be around 0.10% plus 5 cents to 0.50% plus 25 cents per transaction. Providers such as Payment Depot and Stax offer a monthly subscription with a minimal per-transaction fee. This model is transparent and often economical for businesses processing over $10,000 monthly.

- Tiered Pricing: Common in traditional merchant services, tiered plans categorize transactions into qualified, mid-qualified and non-qualified tiers based on various factors. Rates vary, with qualified transactions generally costing less. While detailed and complex, tiered pricing can be beneficial for high-volume businesses in specific industries.

How to Reduce Your Credit Card Processing Costs

Minimizing the impact of processing fees involves understanding and employing various strategies:

- Know Your Effective Rate: Calculate this by dividing total card processing fees by total card sales. Include all fees, such as monthly and statement fees. Understanding your effective rate helps assess if your current processing service is cost-effective.

- Negotiate Card Processing Rates: Regularly audit and negotiate your rates, especially if your processing volume has increased or you’ve expanded sales channels. Providers may offer better rates to retain high-volume merchants.

- Review Your Statement: Scrutinize each line item on your monthly statement. Understanding the specifics of interchange-plus and tiered statements ensures you’re aware of what you’re paying for, helping to identify any inconsistencies or areas for cost reduction.

- Reduce Fraudulent Charges: Implement security measures such as address verification for online sales and ID checks for in-person transactions. Enhanced security lowers the risk of fraud, thus reducing related fees.

- Consider Zero-Fee Processors: Some companies transfer processing fees to customers through a convenience fee. This model eliminates processing costs for the merchant and is effective in certain retail settings, particularly when combined with cash discount options.

Credit Card Processing Equipment and Systems

Terminals, POS systems, cash registers, online gateways and virtual terminals are a few of the many types of hardware and systems that enable card processing. Some credit card processing companies provide their own branded equipment. Others integrate with popular e-commerce platforms, payment gateways, card terminals and retail registers.

The right setup for your business depends on how and where you complete sales and collect payments—in-store, online, via mobile in-person sales or a combination of these.

Physical Card Processing Equipment

In-store and in-person sales settings use terminals and other processing hardware to physically swipe, dip or tap cards at checkout. Since the card is present, these types of sales are considered low-risk and carry the lowest processing fees:

- Point-of-sale (POS) systems: POS systems pair inventory, customer and sales management software with card readers, store registers and touchscreen terminals to complete a sale.

- Smart terminals: Compact all-in-one card processing terminals can be used in-store and in mobile settings via Wi-Fi and cellular connections.

- Basic registers and terminals: No-frills cash registers with card processing terminals work well for basic in-store retail and countertop services.

- Self-serve kiosk checkouts: Customer-facing touchscreen checkouts with built-in card readers are ideal for quick-serve cafes and other self-serve settings.

- Mobile card readers: Paired with a mobile app on a tablet or cell phone, mobile card readers physically process cards for all types of in-person mobile settings, such as fairs and markets, food trucks and mobile service calls.

Virtual and Online Credit Card Processing Systems

Online payments and virtual credit card sales require cloud-based systems called online portals or payment gateways to securely collect and transmit customers’ payment information. Since the card isn’t physically present and staff can’t verify identification, these types of sales are considered higher-risk and carry the highest card processing fees:

- E-commerce payment gateways: Payment gateways are secure online checkout systems that connect your online store to your card processing service to verify and complete online transactions.

- Online payment portals: Some processors have secure online portals that enable a range of modern online payment options including online invoice payments, automated recurring and subscription payments, QR code payments and payment links sent via text or email.

- Virtual terminals: Nearly all card processing services support keyed-in payments through a cloud-based online dashboard, typically called a virtual terminal.

- Mobile terminal or POS app: Many card processing services provide a mobile payment app that enables virtual keyed-in payments using tablets and smartphones. Some providers include this in a POS app that supports both keyed-in and card reader payments.

Frequently Asked Questions (FAQs)

Are credit card processing fees subject to sales tax?

Credit card processing fees are applied to transactions based on the total sale amount, including sales tax. Merchants do pay processing fees on the sales tax portion of the sale. How much that is depends on the state’s sales tax rates.

Do credit cards process on weekends?

Credit card processing is a 24/7/365 activity, and credit cards are processed on all weekends and holidays. However, merchant deposits typically occur on business days, so credit cards processed on a Friday might not be deposited until the following Monday or Tuesday, depending on the payment processing service’s funding schedule.

What is a virtual terminal for processing credit cards?

A virtual terminal is an online dashboard that lets you securely key in credit card information and process payments without a card being present. Virtual terminals are helpful for phone sales or as a backup if a terminal or card reader isn’t working properly. Most payment processing companies provide a virtual terminal and some support card readers for physically swiping cards as well.

Can I write off credit card processing fees?

Credit card processing fees are a business expense, and you can write them off as a cost of sale or under another business accounting expense per your financial advisor.

Why does my business need credit card processing?

According to a study by the American Bankers Association in May 2022, there were over 360 million credit card accounts active in the United States in 2021. This means that the vast majority of American adults hold at least one account, if not more. With credit cards being so common, not being able to accept credit cards means a huge potential for missed sales opportunities.

How do I process credit card payments online?

If you primarily operate an e-commerce business, you’ll need to make sure that you select a credit card processor that is compatible with your website. Some website builders include their own payment gateways, while others allow you to connect with third-party providers. Several of the companies listed above, such as Square, double as website builders so that you can keep everything under one umbrella.

Is credit card processing secure?

Because so much sensitive information is being transferred across these networks, credit card processors are PCI-compliant and use advanced encryption methods to secure transactions.

Which credit card processor is cheapest for small businesses?

The answer to this question varies depending on your sales volume. If you process a low number of transactions on a monthly basis, you may want to choose a processor that charges a low transaction fee such as Stripe or PayPal. If you have a higher volume, a subscription-based model such as Payment Depot where you pay a monthly fee in exchange for lower transaction rates may be a better fit.

How long does a credit card payment take to process?

It generally takes one to two business days to process a credit card payment. On the consumer side, a credit card payment is verified and approved immediately, and funds are held under temporary authorization until the merchant sends the batch at the close of the business day. Next, the merchant’s card processing service and the consumer’s issuing bank initiate the transfer of funds. Typically, the consumer’s statement shows a cleared charge within one to two business days and the merchant receives the funds within one to two business days.