Report Overview

InterContinental Hotels Group (IHG) is establishing itself as a leader in hospitality tech innovation and developing itself into a nimbler, more diversified company. IHG Concerto is the first of its kind hotel tech solution, offering owners reservation, revenue, and property management solutions all in one platform, with the ability to roll out new functionalities easily over time. As IHG works to improve operations for hotel owners, the company has also been strengthening its own business. The company is now much more diversified geographically and in terms of brand offerings than it was before the previous economic recession. We don’t know precisely when the next recession will occur, but IHG’s key areas of focus are making it a smarter, better hotel company that is well-positioned no matter what the future looks like.

What You'll Learn From This Report

- An overview of IHG by the numbers: Sales, earnings, supply, and pipeline

- Geography and property types: IHG’s past, present, and future

- A description of IHG’s recent tech developments

- Owner views of IHG’s technology solutions and views of new IHG Concerto

- Then versus now: An assessment of IHG’s positioning ahead of the next recession

- Owner views on Holiday Inn and Holiday Inn Express brand renovations and expectations

- A description of other areas of strength for the company

- Skift Research forecasts for IHG’s 2019 RevPAR (revenue per available room), revenue, and earnings

- Company risks

Executive Summary

InterContinental Hotels Group (IHG) may not have been as loud as its peers, Marriott and Hilton when it comes to promoting its direct booking pushes or its own acquisitions. But, as Marriott and Hilton battle acquisition integrations and new asset-light identities, IHG is establishing itself as a leader in hospitality tech innovation and developing itself into a nimbler, more diversified company.

IHG has been known, historically, for developing its own tech solutions, but IHG Concerto is the first of its kind, offering owners reservation, revenue, and property management solutions all in one platform, with the ability to roll out new functionalities easily over time. Our survey of IHG-branded hotel owners suggests that all are optimistic about the potential financial benefits, the advantages for price optimization and greater insights, as well as better experiences for guests.

As IHG works to improve operations for hotel owners, the company has also been strengthening its own business. The company is now much more diversified geographically and in terms of brand offerings than it was before the previous economic recession. And, while some have viewed Holiday Inn and Holiday Inn Express as introducing brand concentration risk into the system, the brands are now stronger than ever in terms of RevPAR, and the company has rolled out renovation programs at both to better cater to guest needs and changing preferences.

We don’t know precisely when the next recession will occur. But, in the meantime, IHG is strengthening relations with hotel owners, investing in areas that elevate guest experiences and drive loyalty, and diversifying its own business. Its key areas of focus are making it a smarter, better hotel company that is well-positioned no matter what the future looks like.

Company Overview

As of year end 2018, IHG’s portfolio was made up of 15 different brands covering almost 837,000 rooms in more than 100 countries. In February 2019, IHG acquired luxury operator, Six Senses Hotels Resorts Spas, for $300 million, and the company has plans to launch a new, all suites, upper-midscale brand in 2019.

InterContinental by the Numbers

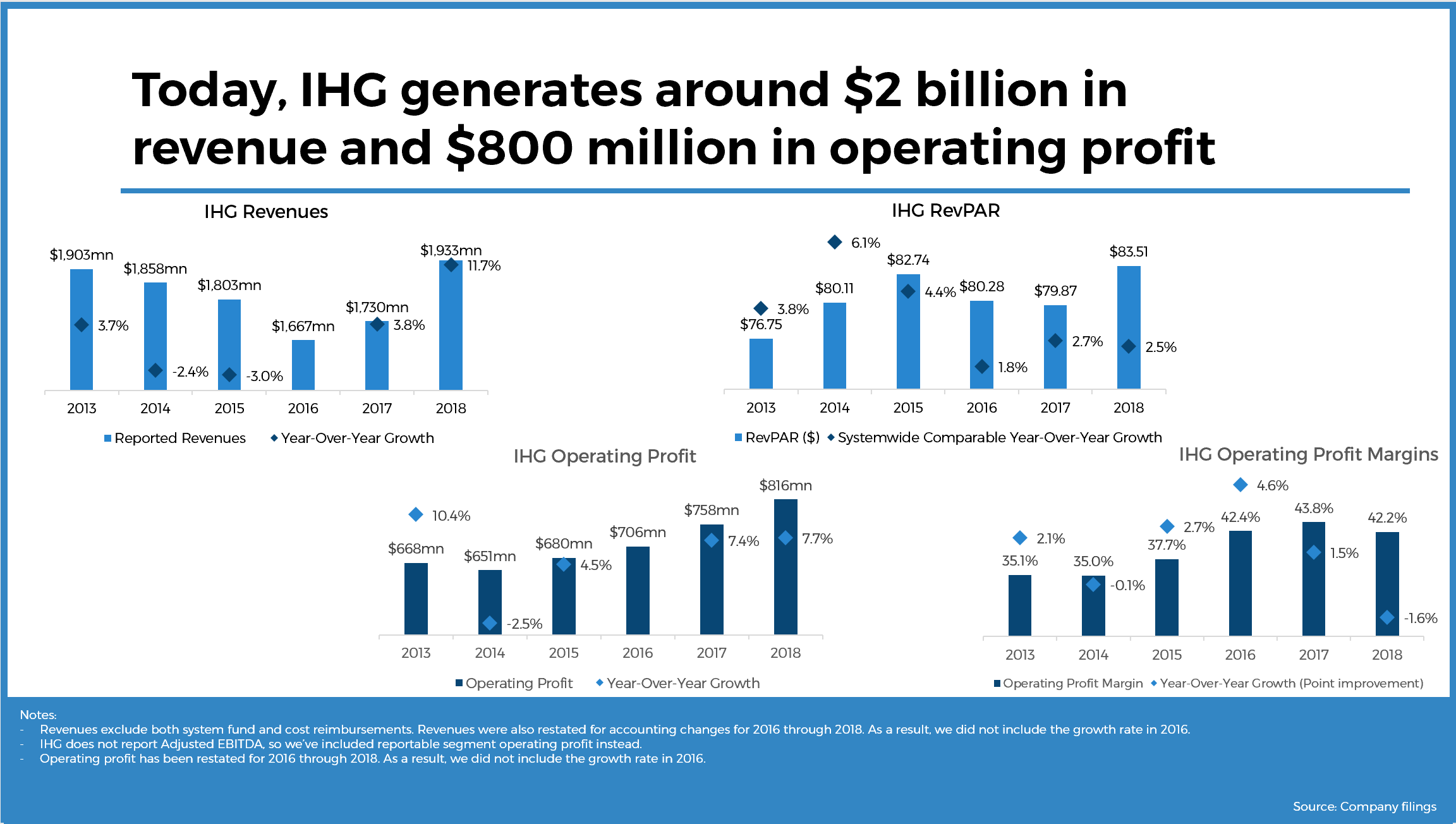

As of 2018, IHG has over $2 billion in annual revenues (excluding system fund and cost reimbursements), over $800 million in operating profit for its reportable segments, and revenue per available room (RevPAR) of $84.

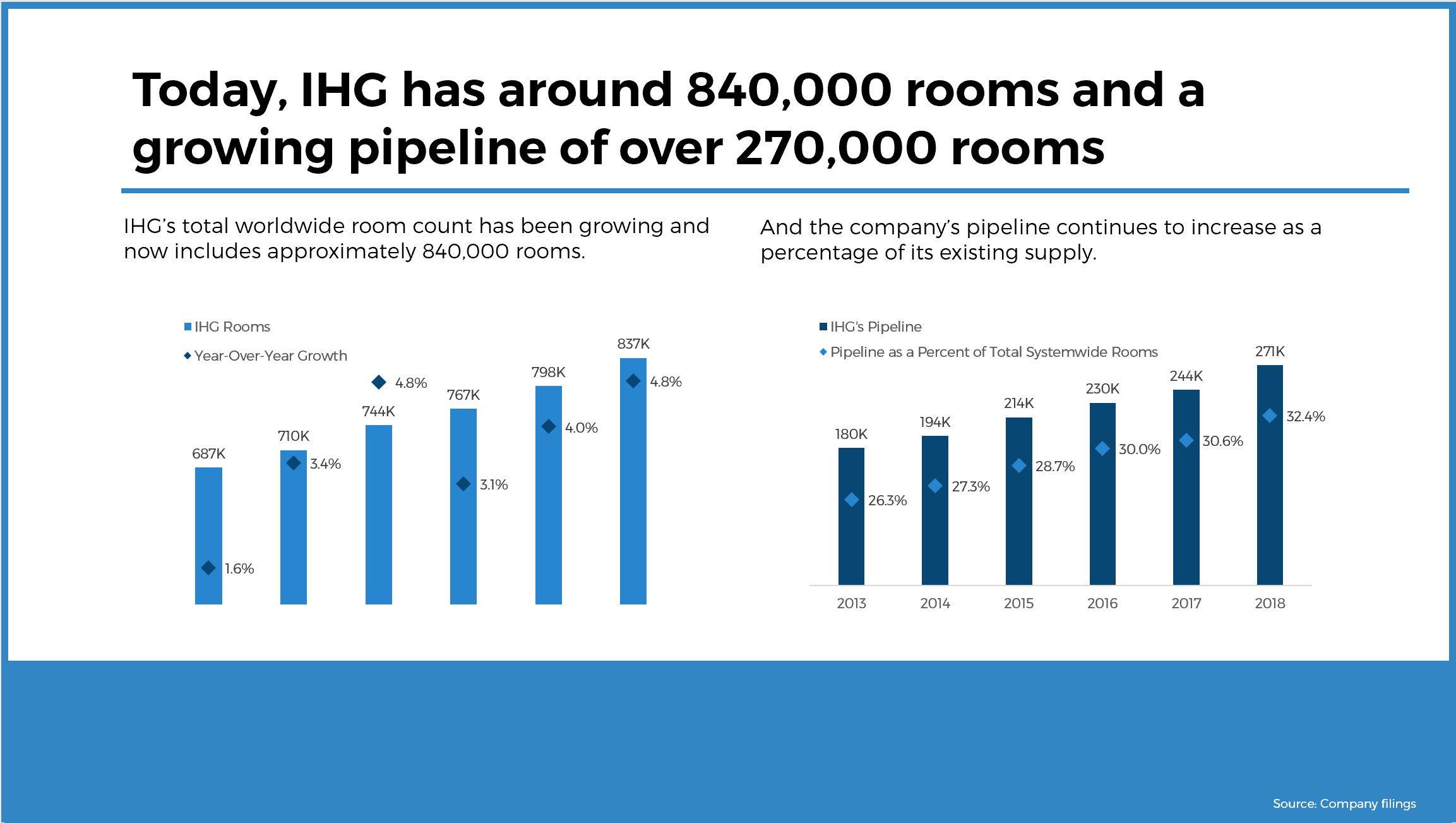

As of year-end 2018, IHG had 837,000 hotel rooms and a growing pipeline of 271,000 rooms. The company’s pipeline has increased significantly over the past couple years, as management has been focused on expanding internationally, particularly in China. The company’s pipeline as a percentage of its total rooms is now just under 33%, compared to 26% just six years ago.

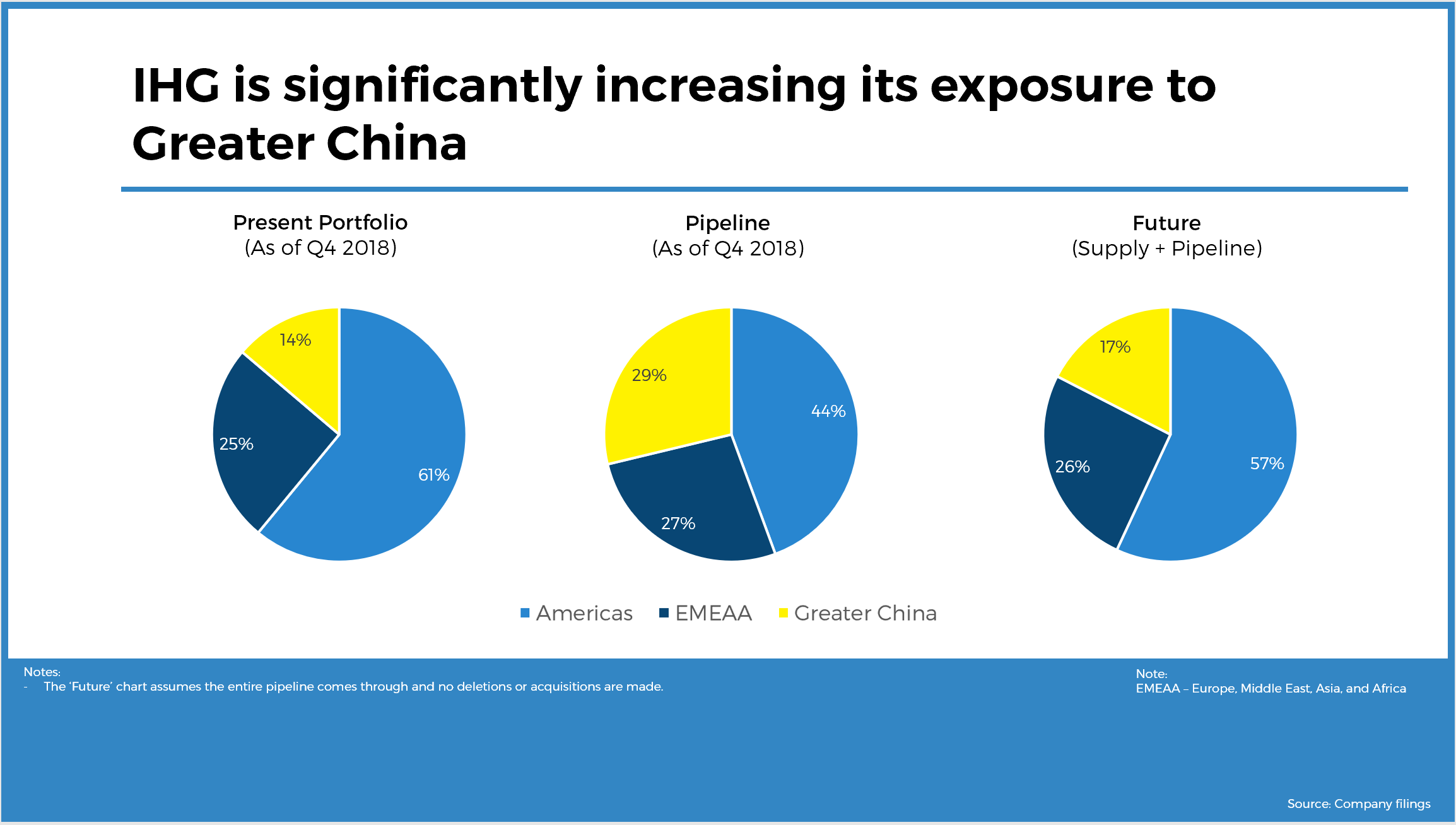

While the majority of IHG’s rooms currently reside in the Americas, with 61% of its total portfolio located in the region, the company is very much focused on expanding its international footprint, particularly in China. As of Q4 2018, almost 30% of its pipeline is located in greater China. In addition, 27% of its pipeline is located outside of the Americas in regions such as Europe, the Middle East, Africa, and Asia, whereas approximately one-quarter of its existing rooms are located in these regions.

IHG has been able to accelerate its growth in China due to its Franchise Plus model, which caters specifically to the Chinese market and offers additional benefits from IHG’s managed hotel model. The product was originally for Holiday Inn Express, but has now been rolled out to Crowne Plaza, Holiday Inn, and Holiday Inn Resort. As of year end 2018, 71 Holiday Inn Express hotels signed in 2018 under the Franchise Plus model, bringing the total signed since launch to 143. Seven hotels signed under Crowne Plaza and Holiday Inn brands in 2018.

“We have seen great potential in China since we opened our first hotel there in 1984. Since then, population growth, urbanization and … [an] emerging middle class have been driving solid demand for hotel rooms across the region. Significant investments in road, rails and their infrastructure and tourism being one of the strategic pillars of the Chinese economy means the long-term tailwinds for our industry are strong,” CFO Paul Edgecliffe-Johnson stated on the Q4 2018 earnings call. “Against this backdrop, our deliberate strategy to grow a sustainable domestic business as our second home market is delivering results. We were early to identify the potential to expand outside of Tier 1 cities and have been adding hotels in these areas whilst the demand drivers are being built. As demand outpaces supply, this will provide a long runway for faster RevPAR growth compared to the more mature market. With 3/4 of our open hotels and nearly 90% of our pipeline in Tier 2 to 4 locations, we are well positioned to capture future growth in these markets.”

We also note that HUALUXE is a brand that was introduced particularly for the Chinese market. However, the company only has eight properties in operation, and while there are 21 properties in the pipeline, HUALUXE rooms make up 11% of the total pipeline in Greater China. Crowne Plaza, Holiday Inn, and Holiday Inn Express make up 20%, 26%, and 20%, respectively.

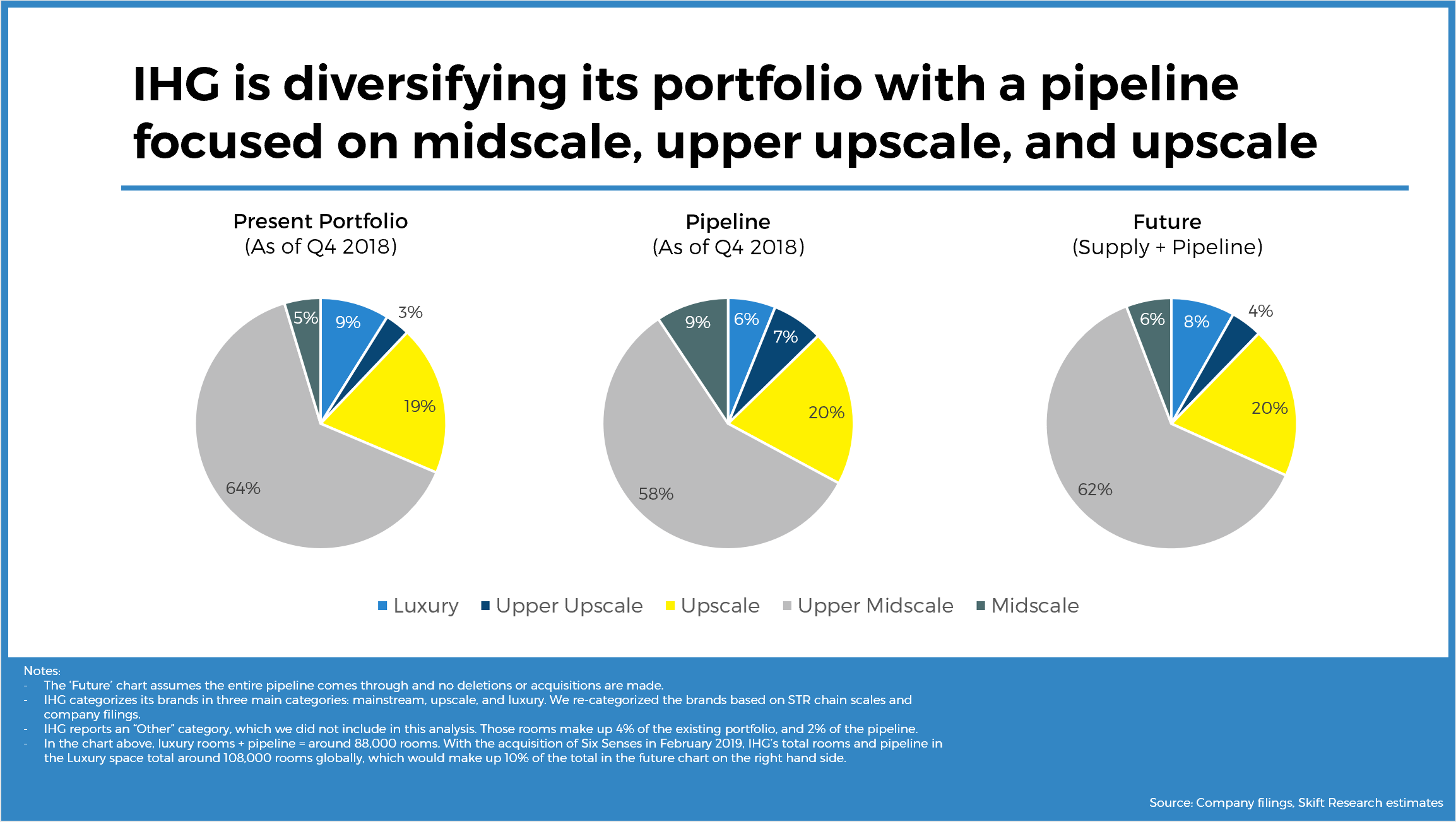

IHG primarily operates in the upper midscale chain scale given its large portfolio of Holiday Inn and Holiday Inn Express properties. However, the company’s pipeline has a stronger focus on midscale, upper upscale, and upscale relative to its existing portfolio, as the company focuses on diversifying its brands. “We’re constantly enhancing our established portfolio and we are moving quickly to add new brands in the underserved areas of the market where we see a clear opportunity to strengthen our offer to guests and owners,” CEO Keith Barr said on the Q4 2018 earnings call.

One of the major growth areas is in the midscale category with the company’s new avid hotels brand. While 87 rooms were in IHG’s existing portfolio as of year end 2018, the company has 15,800 avid rooms in its pipeline. The select service brand will be mostly new builds catering to guests at a lower price point than Holiday Inn Express. As CEO Keith Barr noted on the Q4 2018 earnings called, “Avid capitalizes on a $20 billion segment of the industry where guests are feeling underserved.”

The company also has large pipelines as a percentage of existing rooms in voco (upscale), Hualuxe (upscale), EVEN (upscale), and Hotel Indigo (upper upscale). Regarding the voco brand, CEO Keith Barr noted on the Q4 2018 earnings call that “the brand appeals to guests who are looking for more differentiated upscale experience,” and stated, “owner interest is very strong, and we remain confident of growing it to more than 200 hotels over the next decade.”

We also note that luxury is an increasing area of focus for IHG given the company’s recent acquisition of Six Senses in February 2019. The company also acquired a majority stake in Regent Hotels and Resorts in July 2018. When the company announced the Regent acquisition in March 2018, management noted plans to grow the brand from six hotels to over 40 hotels over the long term.

“In luxury, we have an outstanding and growing offer,” an IHG spokesperson told Skift Research. “Renowned for its expertise in sustainability and wellness, Six Senses secures a presence for IHG in some of the world’s most sought-after locations.”

IHG Performance Versus Peers

Most people may not realize that IHG has one of the largest portfolios of rooms relative to its brand peers. At approximately 837,000 rooms and 271,000 rooms in the pipeline as of year end 2018, IHG has the third largest portfolio out of 7 major peers.

It is worth noting that, together, Holiday Inn and Holiday Inn Express account for 61% of the company’s existing rooms and 57% of its pipeline. Those two brands makeup a large portion of IHG’s size.

The numbers included here and in the charts below do not include IHG’s recent acquisition of Six Senses Hotels. The company noted that, with the acquisition, IHG now has a portfolio of 108,000 open and pipeline luxury rooms globally.

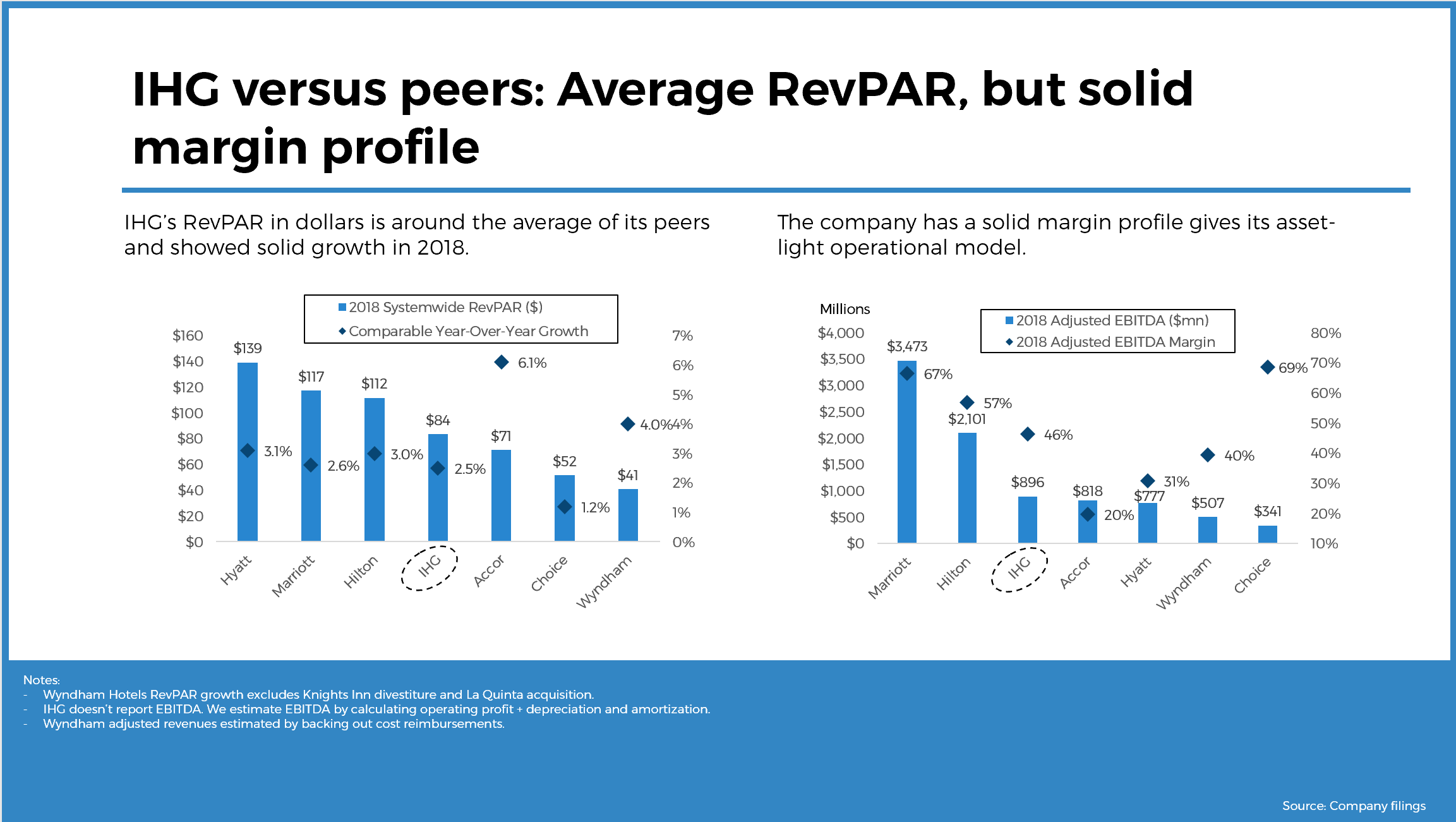

In terms of RevPAR numbers, IHG had average RevPAR relative to its peer group in terms of dollars in 2018, which makes sense given its exposure to upper midscale (IHG reported $84 in RevPAR in 2018 versus the average of $88). The company has also showed solid growth in RevPAR in 2018, though below the average of 3.2%.

We also included year-to-date EBITDA (earnings before interest, taxes, depreciation and amortization) and EBITDA margin numbers in the chart below. While IHG has room for growth in terms of the size of its EBITDA as measured in dollars, its margin is the fourth highest in its peer group, given its high exposure to management and franchise contracts which are much higher-margin businesses relative to ownership. Only 1% of its existing open rooms are owned.

IHG: Valuation and Investor Focus

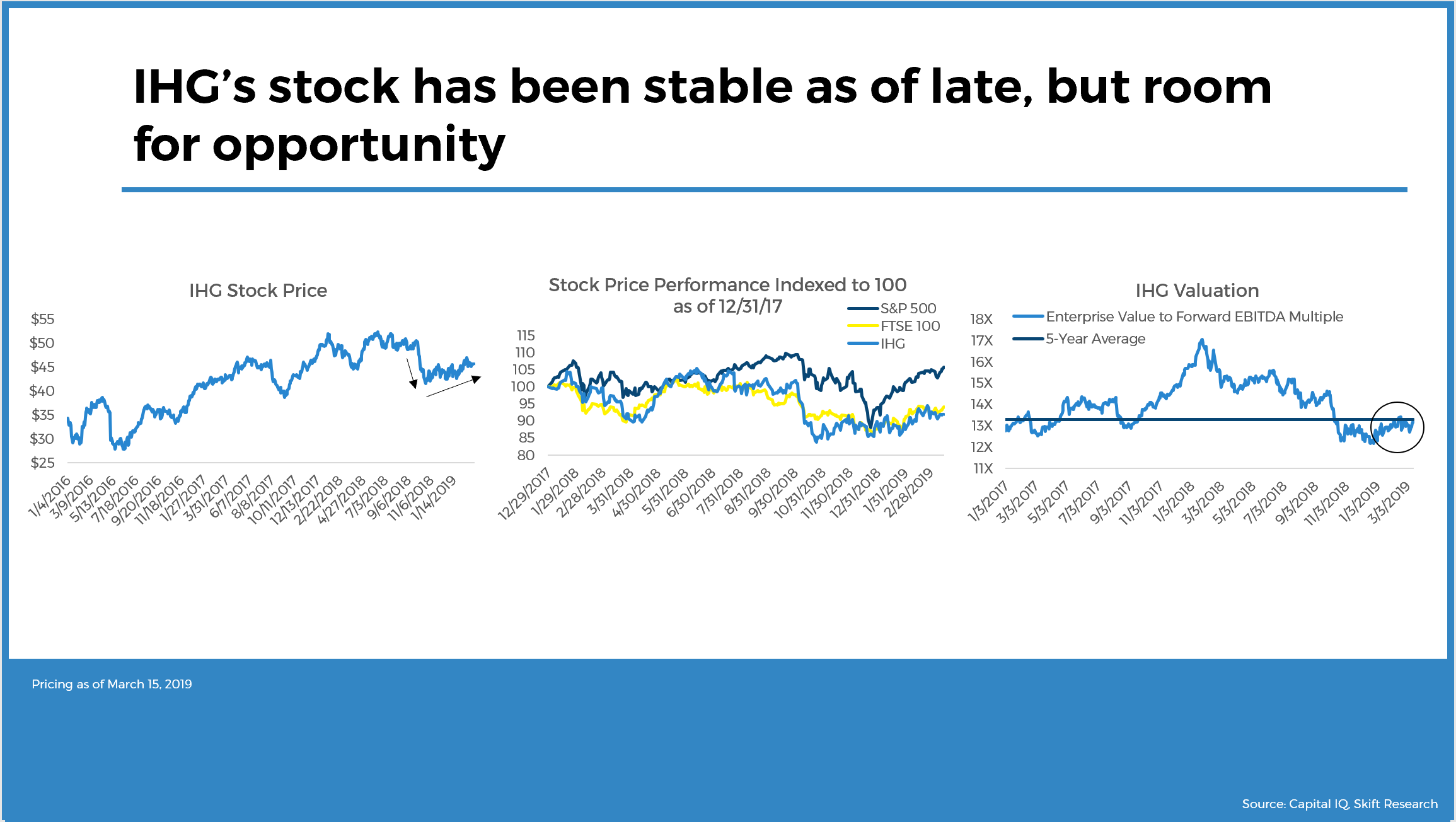

IHG’s stock fell in conjunction with the FTSE 100 and the S&P 500 in the fall of 2018 on concerns of trade wars, Brexit uncertainty, and China’s economy slowing. Then the company reported challenging third quarter results as the U.S. business faced tough comparisons versus the last year when the company saw high hurricane-related demand. Since then, IHG’s stock has essentially stayed in place, with the stock up 2% 2019 year-to-date, versus the S&P 500 up 13% and the FTSE 100 up 7%. Its current valuation has been hovering around the five-year average.

It’s worth noting that IHG’s stock appears to be heavily correlated with the FTSE 100, a share index of the top 100 companies listed on the London Stock Exchange in terms of market capitalisation (IHG is a component of the index). Despite the fact that over 60% of its current portfolio is located in the Americas, IHG has not enjoyed some of the recent upside the S&P 500 has seen, but appears to continue to be heavily influenced by U.K. and European factors.

Diving In: Taking a Leadership Role in Hospitality Tech

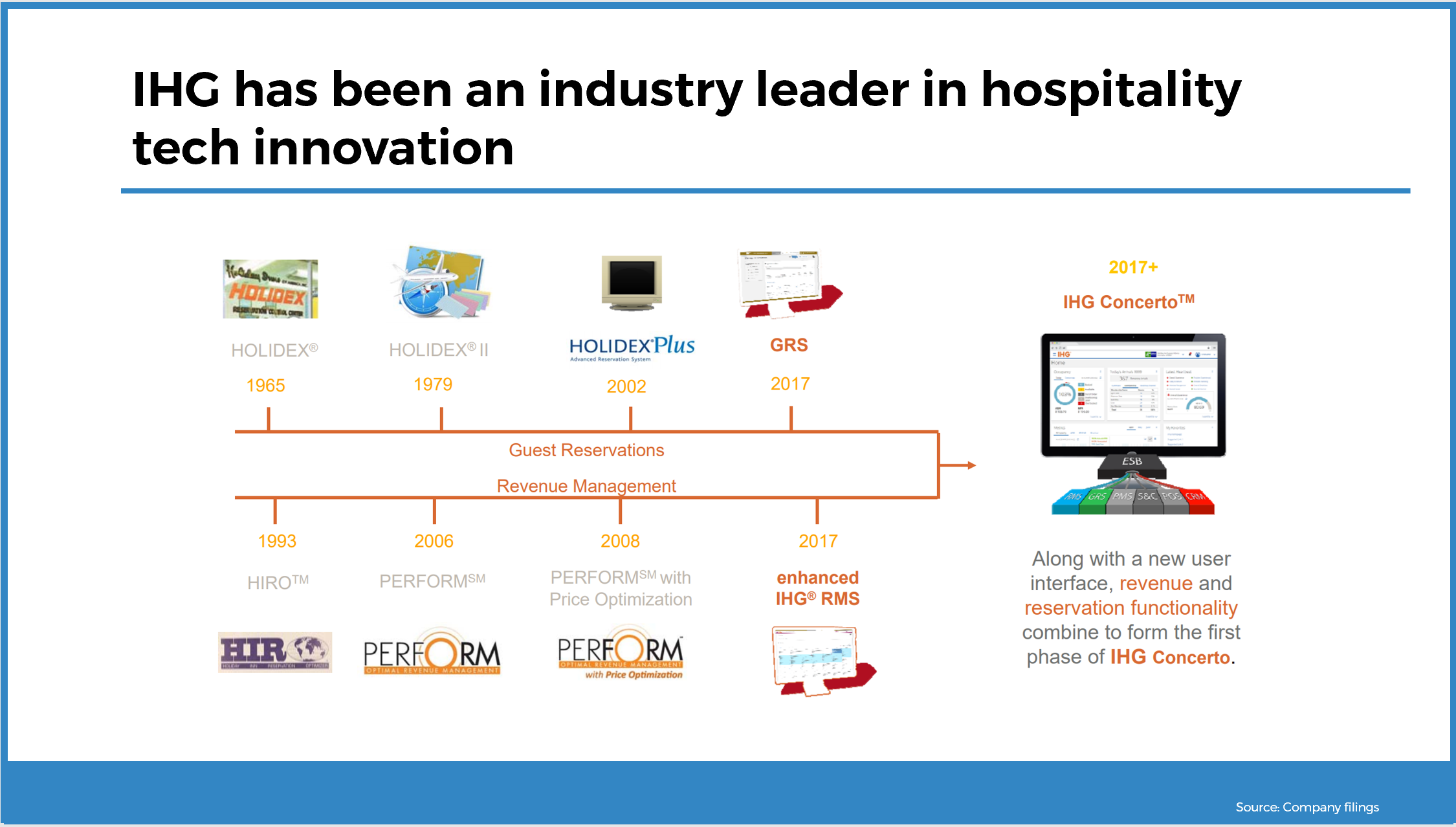

IHG has a history of developing tech innovations in the hospitality arena. The company’s proprietary Holidex platform was an industry first in terms of a computer-based reservations system launched in the 1960s. Even today, the company is ahead of the curve with its leadership in investments in revenue, reservation, and property management capabilities.

“IHG is moving fast in this area [of technology] and making sound decisions. I like the fact they are not only implementing technology solutions, they are becoming leaders in and owing this area of the business,” one IHG-branded hotel owner told Skift Research. “The IHG mobile app is so functional for the guest, and, as it evolves, the possibilities are endless … The guests are demanding innovative technology, and IHG is responding to their needs in real time with great solutions.”

Overview of IHG’s Recent Tech Developments

In 2015, IHG announced a partnership with Amadeus to develop a new Guest Reservation System (GRS) that would replace Holidex. The plan was to roll out the new GRS in 2017 and Amadeus bore the majority of investment cost.

The hopes for the new system included providing owners more flexibility around rate management and access to more data to personalize experiences. CFO Paul Edgecliffe-Johnson noted on the Q3 2017 earnings call, “There’s a few different advantages from it. One is, there will be a revenue uplift on it over time, and as we are able to do more with the system as we bring out new functionality … Interestingly, though, what we found and didn’t expect was a number of owners have said, ‘Well, we like the new functionality.’ And the functionality existed in the old system. It was just quite hard to find some of it. It was … still a DOS-based system. So this is now … in a Windows environment with a much more accessible interface. So more of the tools are going to be used, which should have some benefit to RevPAR. And then we’re able to add in more functionality, which will allow us to do things like revenue manage the overall attributes of the hotel inventory better.”

Then, during Q4 2017 earnings, the company discussed IHG Concerto, a new cloud-based technology system that would house the company’s new GRS as well as its proprietary revenue management system. The all-in-one hotel management platform provides the opportunity for IHG to roll out additional functionality over time – from property management tools to sales and catering to point-of-sale systems.

“IHG has a long track record of innovating through smart technology to ensure we meet the needs of current and future guests,” an IHG spokesperson explained to Skift Research. “As part of our strategic model and value proposition for owners and guests, we have strengthened revenue delivery with the rollout of IHG Concerto, which gives us the most sophisticated cloud-based platform in the industry and a real competitive edge.”

As of today, initial functionality, which includes reservations, rate, and inventory management, yield and price optimization, and a user-friendly dashboard and insights, is live across all 5,600+ properties.

In addition to these current functions, what’s exciting about the platform are the future opportunities. “It lays the foundation for the next stage of technology investment,” CEO Keith Barr noted during Q4 2018 earnings. “The flexible infrastructure is designed to future-proof our technology platform, creating efficiencies when we want to upgrade or add new systems and provide scalability to grow in line with our business. When coupled with the ability to optimize pricing and drive greater levels of guest satisfaction, IHG Concerto enhances our owner offer and delivers a clear competitive advantage for IHG.”

The flexibility of the platform is already evident. In the fall of 2018, Sabre Hospitality Solutions announced a Business Travel Services suite of services including insights on corporate contracts and performance, a lead-generation tool for corporate travel management, and consortia services. InterContinental Hotels Group was able to be one of its first adopters because IHG Concerto makes it easy to partner with other solutions providers.

What’s next for IHG Concerto? The company is piloting attribute pricing, which will allow guests to choose rooms based on different attributes (high or low floor, type of view, close to the lobby/noise or not, type of bed, etc). The successful development of this service will not only enhance guest experiences, driving increased loyalty, but also provide IHG-branded hotel owners greater flexibility in how they fill rooms and better optimize price. The service should also encourage booking direct as this feature will only be available to IHG Rewards Club members.

“It will be 2 to 4 times a year [that] we’re rolling out some new functionality,” CEO Keith Barr noted on the Q4 2018 earnings call. “But we’re doing it because, fundamentally, we believe it’s going to do a few things. One is, [it] will increase overall pricing ability at the hotels … We also think [the tech] can help us on the conversion side, too, by us being able to package up and serve content and pricing and products differently across our brands to be much more relevant, too. So clearly, we’re making the investment in there, because we believe it will drive incremental revenues to our hotels.”

“This cloud technology positions us ahead of major peers, and allows for faster, more agile and more efficient technology updates in the future,” an IHG spokesperson stated. “This is more than simply a technology platform shift to cloud. IHG Concerto is a fundamental shift in the way IHG delivers hotel solutions to users.”

Owner Views on IHG Concerto and IHG Technology More Broadly

We asked hotel owners of IHG-branded properties what were their views on and expectations for IHG Concerto, and the responses were overwhelmingly positive. Details on the owners we interviewed are provided in the Appendix of this report, but responses are kept anonymous.

“This [technology change] has long been overdue … I expect that as Concerto evolves that the hotels will be better positioned to meet the guest ever evolving booking needs,” one owner noted to Skift Research. “I see nothing but advantages for our business. The guests will be able to pick the room they want by location in the hotel, add services or remove services from that room, and this will drive greater profits for the hotels. This is a first class system and IHG responded in a big way with its implementation.”

The owner went on to point that the transition was seamless and smooth. “The change over to Concerto at the hotels was a non event. It took place without any issues.”

Another owner pointed out how simple and easy to use the platform is, called it “a useful tool which is easier to learn and manipulate than its predecessors.” One other rattled off a list of advantages of the solution: “Live dashboard, good metrics, easier tracking, machine learning.”

While it is certainly too soon to tell what the ultimate impact IHG Concerto will have on financial performance, all hotel owners seemed optimistic in terms of their expectations for the solution.

Other Thoughts from Owners on IHG Technology

Owners also had positive things to say on IHG Connect, the company’s seamless, Wi-Fi solution for guests, stating “The IHG connect program is great for delivering a consistent guest experience when they initially log on,” and “The seamless Wi-Fi experience works so well, and the guests love it.”

“IHG Connect provides a platform for the future introduction of greater connectivity across the guest stay such as the ability to stream content in room smart TVs or to order room service through the IHG app,” CEO Keith Barr highlighted on the Q4 2018 earnings call.

However, we note that not all views on IHG technology were positive. One owner highlighted a wide variety of issues including “Too many vendors, too much overlap, Cannot understand the … services provided versus what we are charged, too complicated.”

“The experience can vary from hotel to hotel,” another owner noted. “There is also a lack of guidance on the F&B (food and beverage) side when it comes to PoS (point of sale) systems and guidelines and recommendations for operators.”

“I don’t like the mandatory PMS (property management system) refreshes [the company sometimes requires] as it makes no sense to me to throw out perfectly good working equipment and software on a predefined schedule,” one owner highlighted. “It should be rather on a condition or as requirements change.”

The comments here speak to how IHG is continuing to evolve and develop its offerings (i.e. IHG Concerto will eventually offer catering and point-of-sale services). But, more importantly, they speak to the need for IHG to continue to develop strong owner relations – strong communication of the benefits and advantages of working with IHG are needed in order for owners to continue to stay on board with IHG into the future.

Diving In: Prepping for the Next Recession

One major risk to IHG’s business that equity analysts and other stakeholders often cite is that the company is more heavily exposed to North America and the U.S. versus peers which could prove challenging should the region experience another economic recession.

InterContinental’s American hotels represent 61% of total rooms. The most recent recession led to revenue declining 19% in 2009.

While we do not currently expect an economic downturn in the next year, uncertainty has been increasing globally with concerns of global trade wars, uncertainty around Brexit implications, slowing growth in advanced economies, and decelerating growth in emerging economies.

Nevertheless, IHG’s business is a vastly different business than it was during the last recession. Thus, in this section, we detail the changes IHG has made and the strategic initiatives the company has implemented to better position itself for the future. In our view, IHG is a much stronger and more formidable company and will likely be better able to weather the storm whenever the next recession occurs.

IHG Intelligently and Mindfully Shifted Asset-Light

IHG shifted into an asset-light business model more thoughtfully than some of its peers, which have more recently made the switch. Over the course of almost 10 years, IHG sold almost 200 hotels for total proceeds of $8 billion, culminating with the sale of the InterContinental Hong Kong in 2015 for $938 million.

The Skift Research team has talked extensively about why asset-light business models in hotels are less volatile, more stable, and more profitable than owning hotels outright. n our report, “A Deep Dive Into Operating & Branding Strategies for Hotel Owners,” our analysis demonstrated that while revenue growth and adjusted EBITDA growth of asset-heavy hotels significantly outperformed the asset-light hotels in 2007, asset-heavy hotels saw much more severe declines during the 2009 financial crisis, with revenues declining 8% more and adjusted EBITDA declining 16% more than asset-light hotel companies. This asset-light advantage is largely due to the stability of management and franchise contracts. In the report, we also show hypothetical income statements for hotel owners, managers, and franchisers to demonstrate how managers and franchisers are much more profitable versus owners in general.

Then vs. Now: IHG is a more nimble, more formidable company

IHG has become a nimbler, more diverse, more formidable company since the last economic recession. Almost 40% of its rooms are now located internationally outside of the Americas, versus 30% in 2007. The company has also diversified into other brands and outside upper midscale, increasing the most in upper upscale, upscale, and midscale. The Six Senses acquisition also adds scale to the luxury category.

While IHG has decreased its portfolio of owned and leased rooms since 2007, it has increased its management segment category more so than its franchise category. We view this is in light of the company expanding internationally, where it may make more sense to manage the property so as to have slightly more control over the future operations of the hotel versus simply licensing via franchise. Regardless, the changes the company has made since the last recession are significant, creating a more diverse, more stable, more profitable company.

A Deeper Look at Holiday Inn and Holiday Inn Express

The Holiday Inn brand completely revolutionized the hospitality industry in the 1950s by offering affordable, consistent accommodation for travelers and was the first hotel brand to franchise. The brand has grown and expanded tremendously over the years (Holiday Inn Express opened its first property in 1991) and is now one of the largest brands in the world.

However, the crux of the issue regarding IHG’s “over”exposure in the Americas today arguably is centered on the famous brands – Holiday Inn and Holiday Inn Express. These two brands combined make up 61% of the company’s total portfolio and 67% of its portfolio in the Americas, as well as 67% of the company’s pipeline. Brand concentration is often viewed as a risk. If a brand is overly penetrated in markets or performs poorly, the ramifications could be large.

Thus, we take a look here about how Holiday Inn and Holiday Inn Express are doing since the recession. We look at RevPAR improvement, renovations IHG has implemented, and owner views on the brands. We note that IHG has also invested a lot in renovations for Crowne Plaza in U.S. over the past years, and now in Europe, but, given the broad geographic exposure of Holiday Inn and Holiday Inn Express, we focus on these two brands here.

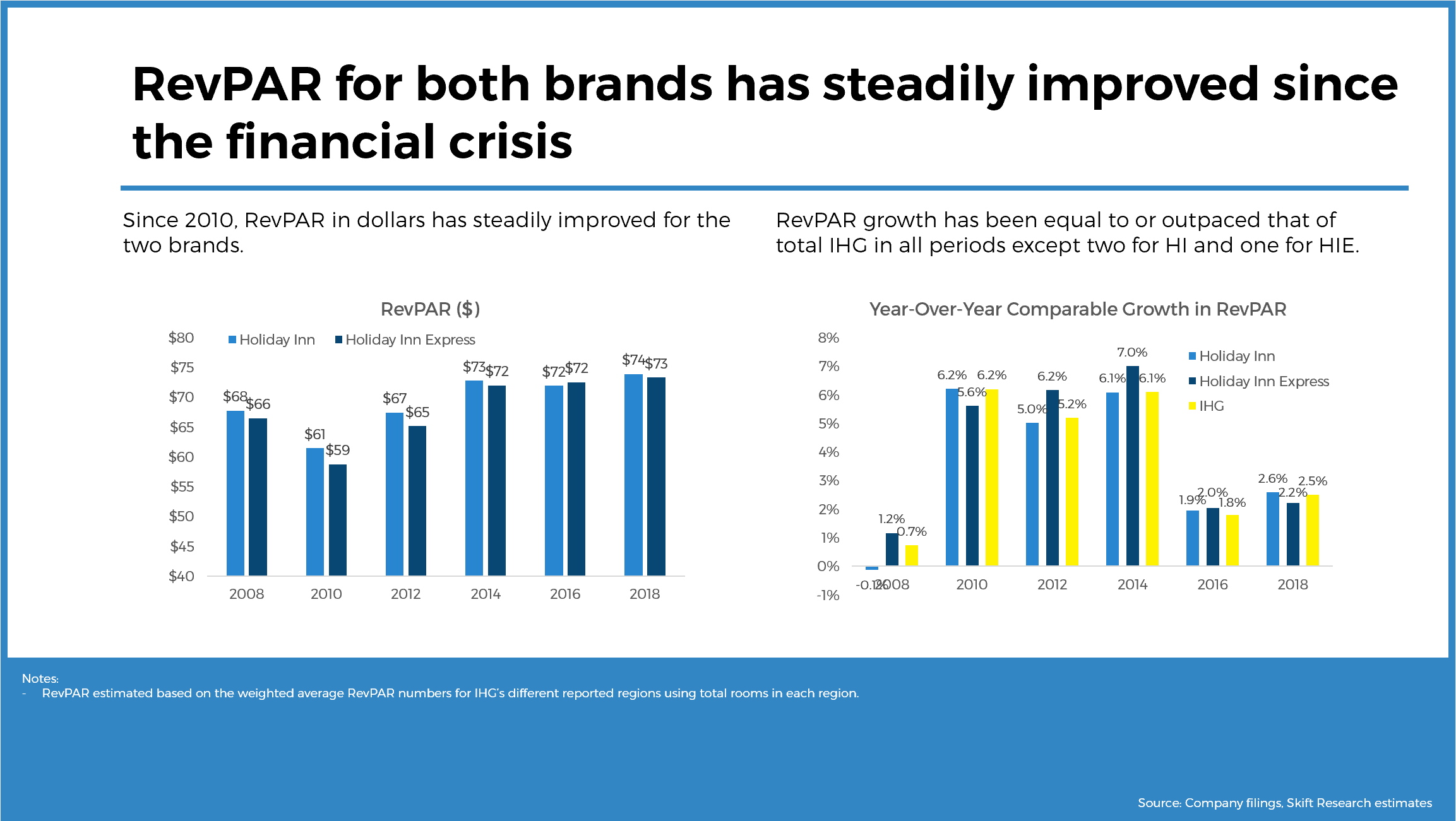

IHG has done a lot to help Holiday Inn’s and Holiday Inn Express’ RevPAR numbers in terms of dollars steadily improving post the financial crisis. Growth rates were in the mid-single digit range from 2010 to 2014 and have regularly outpaced that of the entire company.

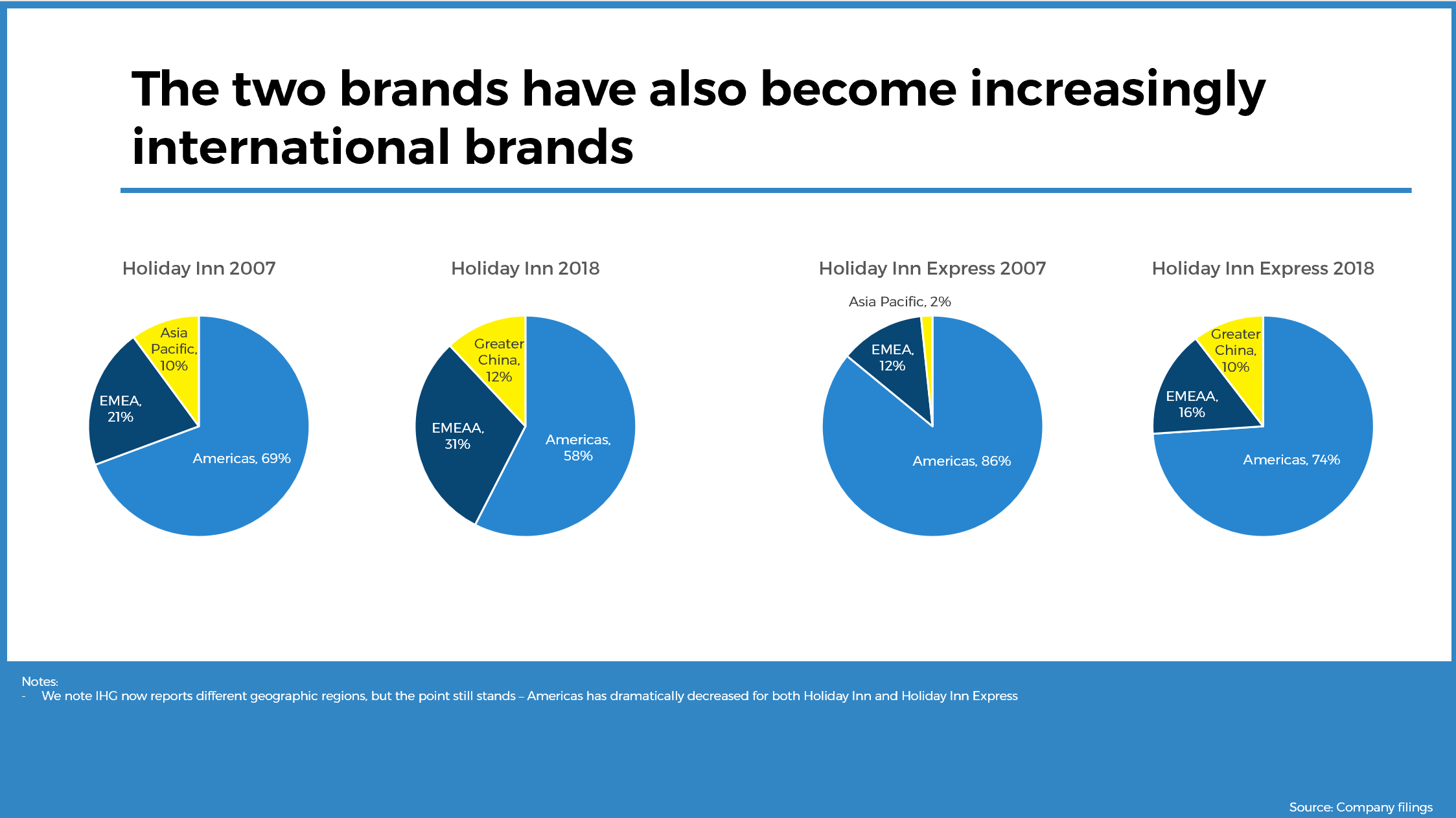

As a result, RevPAR in terms of dollars has surpassed that of its pre-recession highs in 2007. In addition, the two brands make up a smaller portion of the overall portfolio, going from 68% of rooms in 2008 to 61% of rooms today.

The two brands are now much more geographically diversified due to IHG’s Franchise Plus model, as discussed earlier. In 2007, Holiday Inn and Holiday Inn Express had 69% and 86% of their portfolios in the Americas, respectively. Today, those numbers are 58% and 74%, respectively.

These incredible results would not have occurred without the hard work of and dollars invested by hotel owners. In 2007, IHG announced a global relaunch of the Holiday Inn brand family, whereby owners and franchisees were required to invest up $1 billion over the course of three years as part of the brand redesign. Thus, during one of the worst economic recessions, thousands of franchisees had to pay $150,000 to $200,000 to revamp their hotels’ rooms and properties.

There have also been a number of brand specific renovation plans implemented such as Holiday Inn’s Open Lobby concept and H4 and Holiday Inn Express’ Formula Blue and Next Generation rooms.

“Over the years, the Holiday Inn brand continued to innovate and evolve to meet the needs of guests and is currently further enhancing the guest experience by focusing on the H4 guest room concept in the Americas and the Open Lobby design in the EMEAA region,” an IHG spokesperson told Skift Research. “The Holiday Inn brand’s H4 guest room design is a flexible solution that adapts to each guest’s individual needs as they change throughout their stay, allowing them to work or relax wherever and however they want and truly make the space their own.” The H4 redesign features a new rooms prototype catering to both business travelers and families, making everyone feel at home.

Holiday Inn Express targets “the Smart Traveler [who] has a ‘rest and go’ mentality and wants a hotel experience that delivers exactly what they need while traveling for leisure or business, and part of that is a flexible place to work and relax beyond their guestroom,” according to an IHG spokesperson. The Formula Blue design solution, therefore, features multi-functional room elements and a dynamic public space to allow guests to remain productive on the road.

The Holiday Inn Express brand has also rolled out a new Express Start breakfast solution. “To date, 1,500 hotels in the U.S. have implemented this new solution during 2018, with the rest committed to implementing in the near future,” noted an IHG spokesperson. “This new offering is driving a 3-point increase in guest breakfast satisfaction and a higher quality guest experience.”

Owner Views on Holiday Inn and Holiday Inn Express

We asked hotel owners of Holiday Inn and Holiday Inn Express properties their views on the renovations they’ve had to implement at their properties and if they’ve seen a material impact to their financial performance, and views were very mixed. We also asked how they feel about the positioning of the two brands ahead of the next recession. Details on the owners we interviewed are provided in the Appendix of this report, but responses are kept anonymous.

“In the long run, I believe they will be very beneficial. We have completed a Formula Blue [for Holiday Inn Express], and the results, while still early, are positive for both ADR (average daily rate) and guest scores. The guest comments have all been very positive. As more hotels in both brands renovate, I believe the guests will seek out these hotels. This is the first time I can remember that IHG has developed a full blown renovation program that will add true consistency to the brands that will drive market share and brand loyalty, which in turn will be beneficial to owners and guests.”

“We very rarely ever see an immediate bump in performance after renovations. This is coming from someone that did one of the very first Formula Blue renovations and has done multiple others. What I believe the renovations do is keep pace with the other brands … and maintain the position IHG currently has. I would argue we could do 30% less and still keep that same benefit.”

“I would say the renovation changes have helped the brands as a whole, lifting up properties that were dragging down all the others … However, it can be debated if everything IHG has us do is impactful to the guest or just an extra cost. Overall, for the market segment we are in, guests expect a modern hotel with up to date amenities. IHG has done their best to capture those needs when recommending or mandating improvements to owners.”

“[Renovations are] more of an expense. We have not been able to raise our ADR, [and] we get a lot of resistance if we raise rates. IHG said we can recover the $2 million invested in renovations by raising our ADR. But it is more of a hit owners have to bite.”

“[For Holiday Inn Express,] renovation changes are better for the brand. [For Holiday Inn,] renovation changes are not that great. It’s not a great prototype and is very expensive. Most owners do not want to do it or are doing it cheaply, as they are not a big fan of it.”

However, views on how well-positioned the two brands are ahead of the next recession were much more favorable, particularly when it comes to Holiday Inn Express.

“Express is in a good position to continue to be a successful brand. The product and consistency have helped elevate the entire estate to meet and exceed guest expectations in most cases.”

“[Holiday Inn Express] is better positioned, because a lot of the product is renovated, and it’s a leading brand.”

“Both brands are better positioned for the next economic recession … [IHG has] implemented standard changes that have made and will continue to make the hotels deliver a more consistent experience across all of their brand for both product and service. Through procurement, they continue to improve on their ability to deliver better products and prices to their franchisees. They have become more nimble in their approach when it comes to executing their strategies. They respond faster and to changing guest needs and business conditions.”

“Most of the upper mid scaled brands are positioned pretty equally for the next recession. Marriott, Hilton, IHG and Hyatt all have strong customer bases and loyal followers as well as pretty uniform asset quality.”

Other Company Areas of Strength

- Tapping into new market opportunities to diversify and grow: We’ve talked extensively in this report about IHG’s work to diversify. Another area of diversification worth mentioning is IHG’s focus on making sure it’s paying attention to current trends. A perfect example of this is the company’s acquisition of Six Senses. The acquisition represents not only an opportunity for IHG to expand its luxury offerings, but also for it to gain expertise in the wellness and sustainability arenas to better enhance guest experiences across its portfolio. The company also announced during Q4 2018 earnings plans to launch an all-suites brand catering to the upper midscale chain scale later this year in 2019. The company noted that the all-suites category of the upper midscale market has grown by around 70% over the past four years and believes there’s a $18 billion market opportunity. The product will work well for new builds as well as conversions. These are two additional examples of how IHG is staying nimble and taking advantage of market opportunities and where it sees demand heading to better position itself for the future.

- Enhancing guest loyalty proving effective: IHG has been doing a lot to strengthen the value of its loyalty program, IHG Rewards Club, including launching members only pricing and strategic partnerships with companies such as Amazon, OpenTable, and Grubhub. IHG has implemented IHG Connect, a guest log-in platform that offers considerable opportunities for improving guest experiences via streaming TV content and ordering room service, to more than 4,000 properties. The company also has agreements with Alipay and WeChat pay, making it easier to serve Chinese consumers. And the initiatives are certainly paying off. Twelve months after launching Your Rate by IHG Rewards Club (exclusive member pricing), the company showed 3.4% growth in direct channels, and its retail segment grew 2%. The company’s loyalty contribution percentage has grown from 39% in 2014 to 43% as of 2018. IHG Rewards Club hotel direct accounted for 15% of channel revenue in 2018 (IHG Digital [web and mobile] accounted for 23%.).

- CEO Keith Barr is a strong asset to IHG: We would argue that many of the current strengths of the company have developed in recent years under the leadership of CEO Keith Barr. Since becoming CEO in 2017, Keith Barr has been dedicated to supporting IHG’s strengths, improving the technological capabilities of the company, and diversifying the business. He has handled some difficult situations smoothly, including $125 million in cost-cutting measures, the majority of which came in the form of layoffs, and continues to be dedicated to making IHG a nimbler company via investments in tech.“My aspiration is to have a full robust brand portfolio from the upper end of luxury into mainstream, and we still have some gaps there,” he told Skift during the 2019 Americas Lodging Investment Summit (ALIS). “I want us to continue to innovate and lead in digital data technology.”

“Regardless of what brand our owners choose to invest in, everyone at IHG is focused on delivering the things we know will make the difference for them and our guests every day,” an IHG spokesperson told Skift Research. “That means the right technology, systems and hotel solutions that remove friction and drive revenue. It means developing our attractive brands and creating sharp marketing designed to maximize consumer demand. It means delivering an IHG Rewards Club loyalty program that keeps valued guests coming back through IHG hotel doors more often.”

Company Model and Estimates

We built a model for IHG to forecast 2019 results based on various ongoing initiatives at the company. We provide our expectations versus consensus expectations and management guidance below.

We note the company does not provide explicit guidance, but CEO Keith Barr did note on the Q4 2018 earnings call, “The fundamentals of our business remain strong. And while there are macroeconomic and geopolitical uncertainties in some markets, we are confident for the year ahead.”

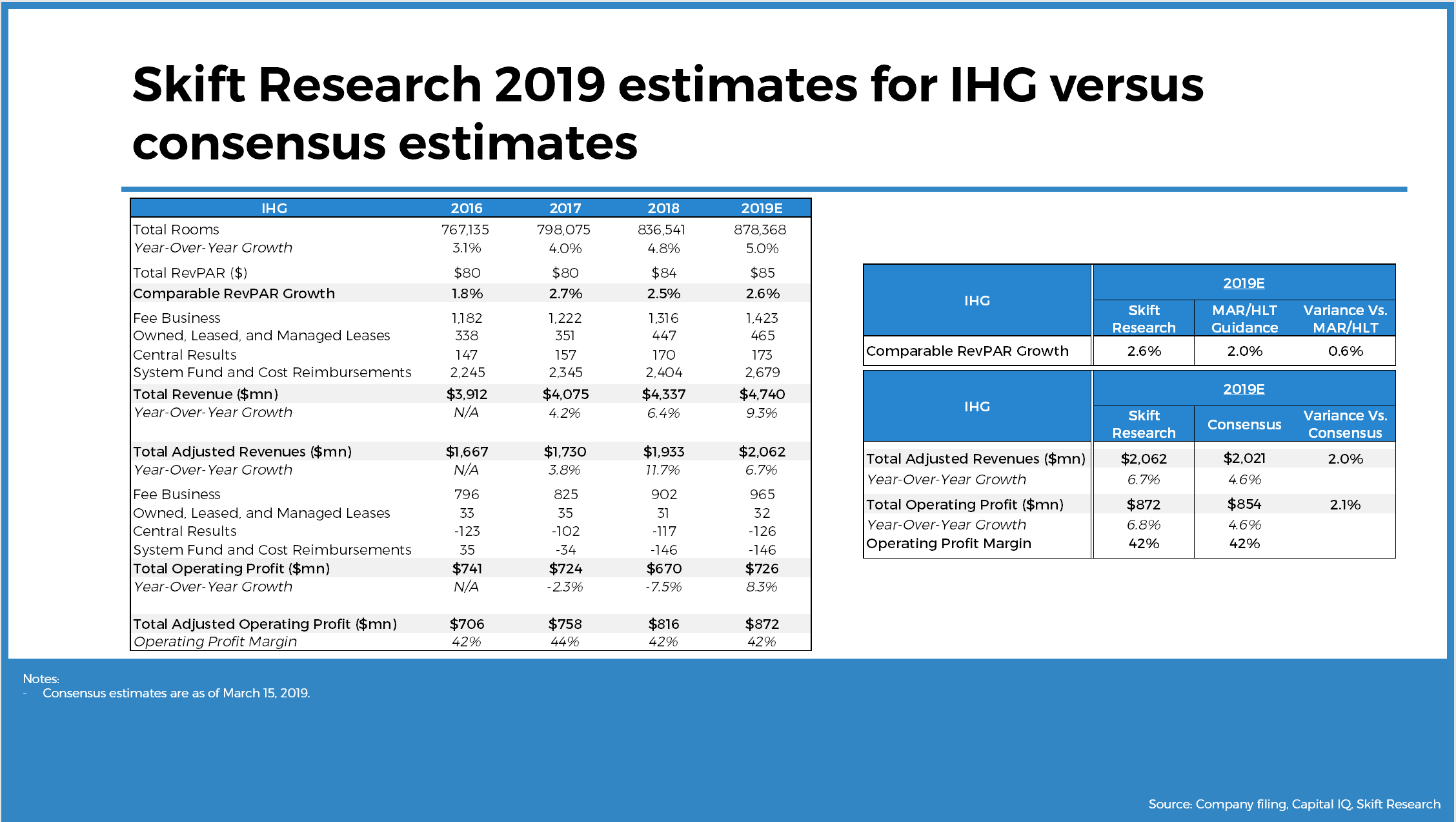

- Room Growth: We forecast 5% net rooms growth in 2019, as we expect ongoing strategic initiatives to play out in the form of industry-leading net rooms growth and an acceleration vs. 2018.

- RevPAR: We forecast 2.6% comparable RevPAR growth in 2019. While IHG does not give guidance for RevPAR growth, both Marriott and Hilton have guided to a range of 1% to 3% in 2019 system-wide. 2.6% is slightly above 2.5% which IHG reported for 2018, as we expected softening results in North America to be offset by strong growth internationally (though easing, IHG’s pipeline is more heavily weighted towards international) and ongoing initiatives to improve RevPAR.

- Revenue: As a result, we forecast over $2 billion in adjusted revenues in 2019 (which excludes system fund and cost reimbursements). Our forecast is 2% higher than consensus estimates and is driven by 7% growth in fee business and 4% growth in the owned, leased, and managed leases segment.

- Operating Profit: We forecast $872 million in operating profit, which is 2% above consensus estimates, driven by our higher estimate for revenue. We expect margins to remain essentially in line with 2018.

- We do not assume any company acquisitions or asset dispositions in 2019.

Company Risks

We would be remiss not to include any risks to IHG’s current strategies and financial performance.

Our current expectations are for steady, stable growth in the U.S., and solid growth internationally for the hospitality industry, albeit at an easing pace compared to what we have seen in the past couple years. Because IHG operates under a primarily asset-light business model, especially relative to the prior recession, the company has mitigated some risks associated with downturns.

While the lack of diversification currently remains a risk, we believe IHG is working diligently to expand its brand offerings and geographical representation which will reduce risk over time. We also note that IHG has properties in over 100 countries around the world, and a brand range of brands covering numerous chain scales from midscale to luxury.

IHG has been focused on growing tremendously in China. However, the country is currently facing decelerating economic growth. Should we see any sustained declines in economic growth or heightened tensions or trade wars with the U.S., it could prove detrimental to financial results for IHG.

Any slowdown in operations as a result of integrating new technology solutions could negatively impact financial performance. However, we currently do not foresee this being an issue, especially given several IHG-branded hotel owners noted the integration process has been seamless thus far.

Appendix

We interviewed five hotel owners and/or operators who currently have IHG-branded properties in their portfolio.

- IHG-branded properties made up 24% to 100% of their portfolios.

- Respondents own 1 to 25 hotels.

- IHG brands included in their portfolios include Holiday Inn, Holiday Inn Express, Holiday Inn Resort, Holiday Inn and Suites, Staybridge, and Candlewood.

- Owners noted also working with Marriott, Hilton, Hyatt, and Choice brands.

- Respondents were based in the U.S. (East, Southeast, Midwest, and West) and Canada

Further Reading

- IHG Press Releases

- IHG History

- IHG Overview

- IHG Global Presence

- Skift Research, “A Deep Dive Into Operating & Branding Strategies for Hotel Owners.” February 2018

- Skift Research, “Skift Global Travel Economy Outlook 2019.” December 2018

- Skift, “IHG CEO Sees More Nimble Hotel Group From What He Inherited.” February 2019

- Skift, “IHG to Replicate Its Light-Touch Kimpton Approach With Six Senses.” February 2019

- Skift, “IHG Confirms Plans to Add Dynamic Pricing to Hotel Award Bookings.” February 2019

- Skift, “InterContinental Lands Another Luxury Brand.” February 2019

- Skift, “InterContinental Launching an All-Suite Brand.” February 2019

- Skift, “InterContinental Hotels Makes Asia Luxury Push With Six Senses Acquisition.” February 2019