欧洲的高福利是否实质上是不可持续的的庞氏骗局?

64 个回答

虽然我也是欧洲福利制度的反对者,但是题主是典型的概念误用, 庞氏骗局一定不能有实业参与,换而言之,有公司实体参与的都不是庞氏骗局。不要把任何高期望,却入不敷出,兑付率不能完全的财政政策都解读为“庞氏骗局”,因为这是概念误用。。

对于欧洲高福利的批判,本质上是欧洲国家在黄金三十年的积累后,出现一个明显的上升期,大致两个状况,

1,社会刚开始进入中质化,财政状况良好。

2,左翼政府上台,开始给选民承诺各种福利政策的建立,占了财政支出的比较高的比例。

3,社会思潮进入多元主义时期,对于移民政策开始变得宽容。

故而,在经济周期上行的阶段,欧洲很多国家建立了比较庞大的福利体系,而当经济走入平缓,或者因为某些经济事件(诸如欧债危机)出现明显下行的经济状况。现有财政运营能力,无法用于运行如此庞大的福利系统,但是选民不是愿意政府大幅度消弱福利政策,且因为移民原因福利系统的负荷开始变大,故而出现入不敷出的情况。状况良好的,开始进行税收制度的大幅度调整,状况差的,就出现难以自行解决,并威胁到整个区域经济的债务问题。。。

其次,你建立的模型是槽点很多。首先,财政收入是经济活动中,政府本身所收到的分成,财政政策的目的之一是通过财政收入对社会资源进行再分配,而这个目的是通过财政支出的方式来进行的。

所以说财政收入包括个人所得税、企业所得税、消费税等一系列税种,支出也包括很多方面。故而你模型中单纯把个人所得税拿来支撑一个“你所谓的福利系统”是显然过于脑补的事情。

而养老金而言,理解也有一点误差。 法国现在的养老保险制度是二战之后才建立起来的,退休人员所领的退休金一部分来自于同一时间年轻人所交的老保险的钱(包括个人、企业部分等等),也就是所谓的“赡养比”,还有一部分是他们当年积累的钱。而在计算其养老金额度的时候,跟他们一生积累的数字有关。

而还有一类是诸如英国的养老金制度,来源三个:

(1)支柱是实行现收现付的国家基本养老保险,由两部分组成:

一部分是每个符合领取养老金条件的退休人员都可以得到相等数额的基础年金。它是一种强制性缴费制度,由国家财政、雇主和职工共同负担的。1997年全额基本养老金的水平为每周61.15英镑,相当于全职男性平均工资水平的15%。

另一部分是于1978年正式实施的政府收入关联养老金计划(SERPS),它根据个人的实际缴费年限和基数区别确定。基本养老保险的受益水平按照消费价格指数(CPI)进行指数化调整。

(2)职业年金计划和强制性的个人年金账户(APPs)构成,它是英国养老保险体系中最重要的组成部分。

(3)第三个支柱为个人自愿性的补充商业养老保险

所以,一个国家的养老金制度非常复杂,不要用这种过分简陋的模型来分析问题

最后,严格意义上而言,没有所谓的“高福利”的概念。因为福利政策的制定是与财政政策和经济状况,所做的有一定执行周期,但是有“时效性”的动态政策,所以说,社会福利支出占财政支出的多少,并不完全是衡量高福利的标准。而是福利政策是否和你的财政能力相匹配,从而避开“福利失衡”。而欧洲福利政策的问题,就是欧洲的经济下行,财政状况无法支撑福利系统,而目前的民众不愿意失去福利政策,导致欧洲现有的财政赤字和主权债务的把控能力非常拙计,也就是说,欧洲的福利政策与它本身的能力并不匹配,故而是“福利过高”。

而高福利的直接原因是“经济下行,总体低增长”等等。。但远不仅仅是如此。

福利政策本身也会影响到产业政策的状况,一个最简单的例子,如果一个国家的劳工福利给企业带来的负担高于企业能通过本地劳工市场所得到收益,那么本土企业自然集体细软出国。。故而,福利政策本身也会反馈到产业政策上,他的制定,决定着国内企业的生态,包括企业成本,产业的迭代率,中小企业的生存状态,进而对于产业经济产生影响,某种意义上,在社会流动性(social mobility)是一个比较重要的间接因素。。故而在福利政策在这些问题上也需要取得一个“平衡”。

而欧洲的问题,就是以上两条全部“失衡”了。。

As a German living in France, I wrote in English (included), but thank JY for the kind translation

坐标法国的德国人,用英文作答,翻译内容由热心知友JY huang提供

The very short answer to your question is: "YES"

很简短的回答:是。

But it's a little bit more complicated than that. It hasn't always been that way, politicians want us to believe it still isn't, and the degradation is incremental and not by design.

但其实这远没有那么简单。高福利并不从来就是一场旁氏骗局,但当今的政客们依然希望让人民相信它不是,希望人民认为福利的衰减是自然的结果,而不是故意为之。

I am a German citizen who lives partially in France, being married to a French wife. So I know both country's systems somewhat.

我是一个德国公民,部分时间生活在法国,并且娶了一位法国妻子。所以我对两国福利系统有或多或少的认识。

Personally, I am lucky that I am exempt from the normal pension system: Being the managing director of my own company (in Germany), I have the choice to stay in the system or not, and today, there is only one rational choice in that case: Get out, and look after your own pension plan through savings and investments to sustain yourself in old age.

个人来说,我很庆幸自己能不依赖这个养老福利系统。作为自己公司的董事总经理,我可以选在加入或离开这个系统。而实际上,现在只有一个合理的选择,就是离开并且好好管理自己的退休金,通过储蓄和投资来维持退休后的生活。

Our welfare states are not Ponzi-schemes by design. In a Ponzi scheme, you pay out unrealistically high dividends to investors by directly taking the money of new investors.

我们的养老福利系统在设计的时候并不是一个旁氏骗局。在旁氏骗局里,给予已有投资者不切实际的高额红利直接来源于新投资者。

The main reason why our system is out of balance is not so much the unemployment, as it is the demographic factor.

这套福利系统的失衡,其主要原因并不是高失业率,而是人口架构因素。

Going back a little bit in history:

In Germany, social welfare was introduced by the famous Prussian Chancellor Otto von Bismarck (Health insurance 1883, Accident insurance 1884, Old Age & Invalidity 1889).

This was pretty much a world's first. Bismarck being a very conservative politician, it seems counter-intuitive at first. But Bismarck was worried about the rise of socialism among the working class, and knew about the value of a stable society for the economy and the military. While it did not really stop the rise of Germany's oldest political party, the Social Democratic Party, it is considered till this day as a major achievement.

让我们先稍微回顾一下历史。德国的社会福利制度是由著名的普鲁士首相俾斯麦引入的。(医疗保险 1883年,人身意外保险 1884年,伤残养老保险 1889年)。基本可以说,这是世界首创的。作为一个非常保守的政治人物,俾斯麦引入一系列保险制度起初是让人难以理解的。但其实,俾斯麦一直担心社会主义在工人阶级中的崛起,他非常清楚社会稳定对于经济和军事发展的重要价值。虽然这些举措最终并没有阻止德国最老牌的政党,社民党的崛起,然而即使从现在看来,这依然是一个巨大的成就。

At first, it worked quite well. Maybe not all people benefited from it, e.g. with a retirement age of 71 and a life expectancy which was too short for many to ever benefit. But the system was in equilibrium.

起初,这套福利制度运行得非常好。虽然并不是每个人从此收益,例如规定了71岁的退休年龄,在当时国民预期寿命较短的情况下,很多人并没有机会获益。但这套系统是收支平衡的。

Why it worked, you can see easily on this stamp, issued to celebrate 100 years of the Old Age insurance in 1989, with evolved into the the pension insurance.

为什么系统能运行良好,从下面这张在1989年发行的,为庆祝老年保险(后成为养老保险)设立100周年的纪念邮票上,可见一斑。

The demographic tree in 1889 was almost a perfect pyramid or pine tree.

First the world wars, and then the declining birth rates have put things on its head since. The birth rate in Germany, without any regulation, is lower than in China, one or two child policy, at about 1.4 children.

人口架构在1889年的时候,是一个完美的金字塔形

然而,接下来的两次世界大战,及其后人口出生率下降,对整个人口架构产生了明显的影响。在没有计划生育的德国,人口出生率依然低于中国,达到了1.4的水平。

Before, we had what we called the "generational contract": The young generation's contributions would pay for the older generation.

But today, we are not far away from the point where 1 person of the active workforce has to support 2 retired people.

At the same time, You can't really win public elections if you hurt the senior citizens.

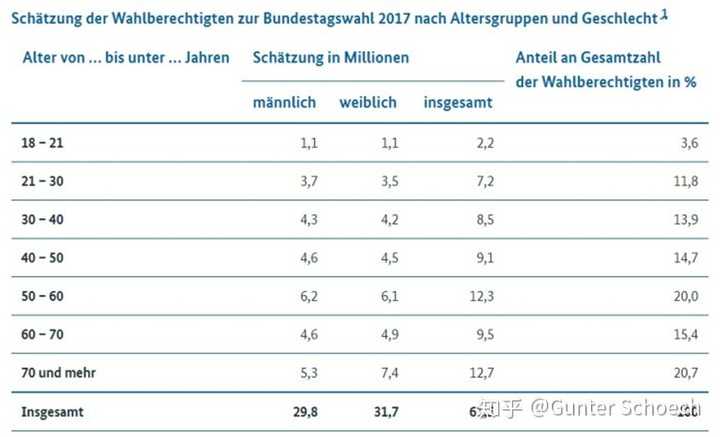

Our last general election had this age distribution: left the age groups, then the millions of eligible voters in millions in men, women and total, on the right the share of the population in %.

在这种情况出现之前,我们有所谓的“代间契约”,即年轻一代支付年老一代的养老金,但今天,我们实际离一个年轻人支付两个老年人的养老金不远了。

与此同时,如果你伤害了老一辈人民的感受,就根本不可能赢得选举。下表是我们上一次大选的选民年龄分布。左边的是年龄组,中间的是“男性、女性、总共”的人数(单位是百万人),右边则是其在人口中的百分比。

Official retirement age is now 67, but hardly anybody retires that late. So if you take all people > 60, you have 36.1% of the voters in that age group.

官方退休年龄是67岁,但实际上并没有多少人真到这么大的年纪才退休。如果以60岁就退休为界,你会发现有36.1%投票人口实际就是退休人口。

So if we can't keep up the generational contract, what can we do?

所以,如果你没有办法维持“代间契约”,该如何是好。

1. The government can use other funds to plug holes in the pension payments.

You can see that in the federal budget, "Work and Social" are by far the biggest expense, at 40.4%. This expense uses other taxes (e.g. VAT etc.) beyond the contributions of citizens to the social insurances.

1, 政府可以动用其它资金为养老金补缺口。从下图可发现,在联邦预算里,就业和社会福利占据了最大的部分,达到了40.4%。除了社保的收入外,这些支出还使用了例如增值税等的其它一些税款收入。

2. The government is reducing the benefits in various ways. It has already raised the retirement entry date from 64 to 67 years (if you retire earlier, you receive less benefits).

At the same time, the relative share of your last net income which you get as pension has declined to 48% and is forecasted to decline further.

2, 政府正在多方面减少福利的支出。退休年龄从64岁推迟到67岁。越晚退休,则你收到的福利越少。于此同时,与工作收入挂钩的养老金收入,其比例已经持续下降到48%,预期还会继续下降。

Finally, if you take these 48%, look at the distribution of German incomes, and compare that to the official definition of poverty in Germany, then 40% of current working people will qualify for the social help intended for the poorest (in particular including those who have never worked and paid into those social systems).

3, 最后,如只果你只能拿到48%的净收入作为养老金的话,现有的40%的德国工作人口将在退休时直接掉到贫困线以下(包括那些从未工作,没有为养老金支付过一分钱的人)

That is certainly not a sane system.

显然,这个系统是不健全的。

People are encouraged in many different ways to start their own capital based insurance.

So one where they will get back the very money they saved, plus (or minus in the worst case) the capital gains on that money. Instead of financing the current generation of retired people through their contributions and also through re-directed taxes of other kind, and later being left "in the rain" when the next generation is much smaller and unable to pay enough into the system.

政府正在以各种形式鼓励人民参与到自持资本的养老保险中。他们可以在日后取回他们存下的钱,以及这些钱投资所得的利润(当然,有可能投资失败导致拿回的钱变少)。政府希望通过这样,避免为支付现有退休者的退休金而进行融资,以及动用其它税款,避免将来因为人口架构改变,没有足够的新养老金收入去支付退休支出的被动局面。

But those who can build their own capital based old age insurance are those who have enough money left each month to pay for it. That will hardly be the 40% of the working population we just talked about.

但那些有足够能力参与到自持资本养老保险的人,即每个月还有余力参与投资的人,根本就没有多少在我们之前提到的那40%里。

In any case, in such a scenario, the risk of the investment is thus transferred to the retiree. While before, the government made some guarantees, which were also founded in the belief a certain capital appreciation could be achieved with the contributions, this risk now resides fully with the beneficiary. With risk free interest rates hovering barely above 0 in the Western world that's a big problem for life insurances and similar products which typically form part of any private retirement saving.

但无论如何,在这种情况下,投资的风险都直接转嫁到退休者身上。虽然此前,由政府主导的养老系统,也是经由投资获得收益,得到一定的保障,但现在这种投资的风险则完全转嫁到投资者身上。在西方国家里,保本投资的利率往往仅仅高于0,这对于人寿保险或者任何的私人退休储蓄来说都是一个很大的问题。

Germans are traditionally very unwilling to invest into shares instead, and prefer bonds, which have no yield today. Stocks have a better performance, in any case of the very long run as for a young person saving for retirement. But Germans feel that stocks are speculation rather than investment, and have not yet forgotten 2001 and 2007.

传统上,德国人非常不愿意投资股票,而是更喜欢债券,但现在的债券近乎没有收益。 长远来说,股票投资往往有更好的回报,实际是适合成为年轻人为退休作准备的一种储蓄。 但德国人往往认为股票是更多的是投机而不是投资,并且他们依然对2001年和2007年的金融风暴有深刻的记忆

As a result of all this, I see an inexorable decline of the system. No government can make really hard cuts, but economic realities continue to catch up with us.

In the past couple of years, Germany has made a budget surplus and even reduced debts. This is due to a large degree to the artificially low interest rates ever after 2007 financial crisis, and a decent world economy fueled by that cheap money which benefited Germany as export oriented nation. In the coming years, budgets will become more challenging, while the aging progresses further.

What happens when you have to cut really deep in the social welfare system, we have seen in Greece.

总结前面所说的,我看到了这套福利系统不可避免的衰落。 没有哪个政府可以做出真正的削减,而经济环境的现实问题却从没有放过我们。在过去的几年,德国实现了预算盈余,甚至减少了债务。 这在很大程度上是由2007年金融危机后人为的低利率,低息贷款使地全球经济上扬,使得以出口为主导的德国从中受益所带来的。在未来几年,老龄化将进一步发展,预算制定将变得更具挑战性。而我们已经在希腊身上看到过,当你必须在社会福利体系中进行大刀阔斧的改革时,会发生些什么。

The population feels that their standard of living is not only improving less fast than in other parts of the world, but that in many cases, it's difficult for the young generation even to keep up with their own parents, at least on a running basis. While they inherit huge wealth accumulated from ~1950-80, the perception of own development is often less bright.

They "Yellow Vest" protests in France are an expression of this diffuse feeling. Much is mixed into it, but "purchasing power" is at the heard of the people's demands. A government can redistribute wealth through taxes, subsidies and benefits. But if the economic and demographic trends leave less to distribute, economic well being can not come from thin air. Cutting back social welfare is a result.

人们认为他们的生活水平的增长不仅比世界其他地区慢,而且在许多情况下,年轻一代甚至跟不上自己的父母。虽然他们继承了从1950年至1980年积累的巨大社会财富,但对自身发展的视野却不甚明朗。 这群人在法国的“黄背心”抗议活动表达了这种晦涩的情绪。很多东西都混杂在一起,但对自身“购买力”的诉求是事件的核心。 政府可以通过税收,补贴和福利重新分配财富。 但是,如果经济形势和人口架构的改变减少了可分配的财富,经济福祉自然不可能无中生有。所以,削减社会福利是一种必然结果。