Last Updated on –

Quick Take

What’s the best investment in the Philippines for both short and long-term goals?

The answer ultimately depends on your financial goals, resources, personal skills, risk tolerance, and preference.

That said, building a business and purchasing real estate are both amazing for short and long-term goals. Investing in the stock market is also one of the most stable investment vehicles for the last few decades.

Whatever investment you choose, the key is to research well. Remember that all investments still come with inherent risks and it is your duty to do your due diligence if you want to protect your hard-earned money.

Feeling like your wallet is always playing catch-up with the rising cost of living?

You’re not alone.

Financial security is a top concern among millions of Filipinos, and what better way to achieve this than investing?

If you’ve saved up Php100,000 through hard work and dedication, investing it can be nerve-wracking.

After all, you’re putting money, sweat, and sacrifices on the line. To make your hard-earned money work, you must make strategic choices.

So where do you start?

The world of investments can seem overwhelming, especially when you’re bombarded with jargon and complex concepts that seem designed to keep you out.

Here’s the thing: every successful investor started somewhere, and many faced the same fears and uncertainties you might be feeling right now.

Understanding that it’s normal to feel anxious about investing your money is the first step towards overcoming that fear.

The key is to begin with a step, no matter how small.

Whether you’re a seasoned investor or just starting, this article is for you. After you read this, you’ll have a solid understanding of the top investment opportunities available in the Philippines.

Remember, investing is not one-size-fits-all. What works for one person might not work for another. It’s about finding the right fit for your financial situation, your goals, and, importantly, your peace of mind.

Contents

What’s the Best Investment Vehicle in the Philippines [According to Data]

In an effort to understand the investment behavior of Filipinos better, Grit.PH recently conducted a study entitled “Best Investment Vehicles for Filipinos.” Over 867 small and non-institutional investors participated in the study.

Among the respondents were:

- 57.4%: female

- 38.5%: male

- 3.1%: LGBTQIA+

- 0.9%: Non-conforming

The study also spanned investors of all ages.

- 20.3%: 18-25 years old

- 14%: 26-30 years old

- 26.5%: 31-40 years old

- 17.2%: 41-50 years old

- 12.8%: 51-60 years old

- 9.2%: 61+ years old

The study asked respondents if they were to select one investment vehicle for their portfolio, which one would they choose.

Results showed that most people preferred starting a business (27%).

Followed closely by real estate (21.6%), stocks (11.4%), and Pag-IBIG MP2 (11.2%).

Here’s the full survey result for the investment vehicle that Filipinos preferred the most:

| Investment | Preferred by |

| Starting a Business | 27% |

| Real Estate | 21.6% |

| Stocks | 11.4% |

| Pag-IBIG MP2 | 11.2% |

| Mutual Funds | 6% |

| REITs | 5.2% |

| Bonds | 4.3% |

| High-Yield Savings Accounts | 3.5% |

| Cryptocurrencies (and NFTs) | 3.5% |

| Forex | 3.3% |

| Venture Capital (Private Equity & Angel Investing) | 2.3% |

| UITFs | 0.8% |

9 Best Investment Opportunities for Short & Long-Term Gains

Our team has carefully selected a diverse array of investment opportunities in the Philippines that we believe cater to a broad spectrum of investor profiles.

Whether you’re in search of secure, long-term growth or are on the lookout for more dynamic, high-yield prospects, our curated list aims to meet your varied investment needs.

1. Small Business

| Minimum Investment: | ₱5,000 |

| Risk Level | High |

| Average Returns | Varies widely depending on the type of business, the industry, market conditions, and the specific strategies and management skills of the investors |

Unfortunately, the reality of achieving ultra-millionaire status in the Philippines through employment alone is near impossible – and the pathways to become one are relatively limited.

It’s either you marry into a wealthy family, receive a hefty inheritance, win the lottery, or successfully launch your own business.

Although starting your own business comes with significant risks and usually demands specific skills, compared to other investment vehicles, it remains a favored choice for Filipinos because you have the option to start small.

With just ₱5,000, you can get into businesses like freelancing, street foods, karaoke rental, e-loading, and many more.

There are literally dozens of options for those who want to start a small business for under ₱100,000.

Starting or investing in a small business, including franchising, in the Philippines can be a good idea for several reasons:

| Growing Economy | The country has been experiencing steady economic growth, making it an attractive place for business investments (5.6% growth rate in 2023) |

| Large Consumer Market | With a population of over 110 million, the Philippines offers a large and diverse market. This vast consumer base can provide a steady demand for a wide range of products and services. |

| Strategic Location | The country’s strategic location in Southeast Asia makes it an ideal gateway for businesses aiming to tap into the larger ASEAN market. |

| Increasing Internet Penetration | With the increasing accessibility of the internet (73.1% internet penetration rate in 2023), businesses have more opportunities to reach their target market and expand their customer base through online platforms. |

| Flexible Workforce | The Philippines boasts a large, educated, and English-speaking workforce that is adaptable and capable of supporting various business needs. This can be a significant advantage for new businesses looking for efficient and cost-effective staffing solutions. |

Tips on Starting a Small Business in the Philippines:

Find your Passion.

A lot of people wonder what they should sell. Finding your passion can be important because it will help you push through with your business even if the going gets tough. For instance, if you have the passion for fashion, selling clothes would be ideal for you.

Conduct thorough Market Research.

The thing about most Filipinos is that, when they think about starting a business, all they think about are the basics, such as where to get capital and what product to sell. Those may be the main things, but market research is always important in any type of investment.

You have to understand the local market dynamics, consumer preferences, and competitive landscape. This will help you identify potential opportunities, challenges, and the viability of your business idea.

Secure Funding.

Your funding will cover two types: pre-operating fund to cover for equipment, stock, deposits, permits, etc., and working capital, which may cover salaries, rent, utilities, supplies, and other contingencies. It’s advisable to secure funding for at least six months of operation.

Comply with Legal Requirements.

Ensure you complete all necessary registrations and obtain the required permits. This includes registering with the Department of Trade and Industry (DTI) for sole proprietorships or the Securities and Exchange Commission (SEC) for corporations and partnerships, as well as the Bureau of Internal Revenue (BIR), and local government units for business permits.

Leverage Technology.

Leverage Technology. With increasing internet penetration in the Philippines, leveraging dogota; platforms for marketing, sales, and operations can provide a competitive edge. Consider establishing a strong online presence through a website and social media.

Develop a Robust Business Plan.

A comprehensive business plan should outline your business goals, strategies, market analysis, financial projections, and operational plans. This document is crucial for guiding your business decisions and securing financing.

Build a Reliable Team.

Hire skilled and motivated employees who share your business vision. The right team can drive your business towards success.

Focus on Customer Service.

Filipinos value excellent customer service. Providing a positive customer experience can lead to repeat business and word-of-mouth referrals.

2. Real Estate

| Minimum Investment: | Starts at ₱50,000 (Foreclosed Properties) |

| Risk Level | High |

| Average Returns | Rental Yields of 4% to 8% annually; 5% to 10% (or even higher depending on location) for property appreciation |

The real estate market in the Philippines offers a wide range of investment opportunities, from affordable residential properties to luxury developments, commercial spaces, and agricultural land, catering to different investment capacities and preferences.

If you’re thinking about owning a property but you’re wary about how much you want to spend, you may also consider buying foreclosed properties to get a cheaper deal. Or acquire a house or condominium unit through rent-to-own schemes, installment payments, or a monthly mortgage.

Real estate investing can offer a variety of ways to generate income and achieve substantial returns. Here are some strategies to earn from real estate investing:

- Rental Yields: Compared to many other countries, the Philippines offers attractive rental yields (for both residential and commercial properties as well as long-term or short-term rentals), making it an appealing option for investors looking to generate passive income from their properties.

- Property Appreciation: Real estate properties in the Philippines have historically appreciated over time (house prices grew by 12.9% YoY in Sep 2023), providing investors with significant capital gains.

- Fix and Flip: This involves purchasing properties below market value, renovating them to increase their value, and then selling them for a profit. This strategy requires a good understanding of the real estate market, renovation costs, and timing.

- Land Development: Buying land and developing it into residential subdivisions, commercial complexes, or industrial parks can yield high returns. Although this approach involves a higher risk and requires significant capital and expertise in real estate development.

- Lease Options: This involves leasing a property with the option to buy it at a later date. You can profit by renting out the property and potentially selling it for a higher price in the future.

- Owner Financing: In this scenario, you act as the bank for the buyer, providing them with a loan to purchase the property. You earn income through the interest on the loan in addition to the initial sale price of the property.

- Buy “Pre-selling” Properties: When you buy a pre-sale unit, it means you are purchasing a property in its pre-construction stage. A lot of investors make tons of money through this method because they buy it at a low introductory price, and then sell it at a higher price after its construction. This almost always guarantees high profits.

- Invest in a Hotel Unit: Hotel investing refers to buying a hotel unit and letting a company operate, manage, and maintain it on your behalf. Just like owning a condominium, you will also have a title for your unit.

Tips for Real Estate Investing

Due Diligence.

Understand the market trends, property values, and demand in various locations. Research helps identify promising areas for investment, whether for residential, commercial, or industrial properties.

Choose the Right Location.

Location is key in real estate. Look for properties in areas with strong growth potential, good infrastructure, and access to amenities. Consider emerging cities and neighborhoods, as well as established areas with steady demand.

Find Foreclosed Properties.

Go to banks, lending institutions, SPAV companies or companies formed under the Special Purpose Vehicle Act of 2002 to help banks shed their nonperforming assets, and government financial institutions like the Social Security System (SSS), Home Development Mutual Fund (Pag-IBIG Fund), and National Housing Authority (NHA).

Understand Legal Requirements.

Familiarize yourself with the legal aspects of buying and owning property in the Philippines, including titles, taxes, and ownership laws (particularly for foreign investors who face certain restrictions).

Get your Financing ready.

When you already have a housing loan approved by the bank, sellers will take you more seriously. And so, you’ll get more negotiating leverage compared to other buyers.

Consider your Investment Strategy.

Decide whether you’re investing for long-term appreciation, rental income, or a quick flip. Your strategy will influence the type of property you buy, the location, and how you manage the investment.

Calculate Expenses and Profits.

Be realistic about the costs involved, including purchase price, taxes, renovation, maintenance, and management fees. Calculate potential profits carefully to ensure a good return on investment.

Inspect the property.

You shouldn’t ever buy anything without properly inspecting it. You must see for yourself if it’s worth your money.

Plan for the Long Term.

Real estate investment often yields the best returns over the long term. Be patient and think strategically about how to grow your portfolio for future gains.

Diversify your Investments.

Don’t put all your money into a single property or location. Diversifying your investments can reduce risk and increase potential returns across different markets and property types.

3. Stocks

| Minimum Investment: | ₱5,000 (First Metro and COL Financial) |

| Risk Level | High |

| Average Returns | 9.06% per year (2021) |

Stock investing involves buying shares of ownership in public companies (listed in the Philippine Stock Exchange) with the expectation of earning a return.

This return can come from dividends, which are payments distributed by the company to its shareholders from its profits, or from capital gains, which is achieved by selling the stock at a higher price than the purchase price.

Investing in the Philippine stock market offers potential for high growth due to the country’s emerging economy, demographic advantages (with its young and growing population being a key driver for domestic consumption), and ongoing infrastructure developments.

It also provides investors with an opportunity for portfolio diversification, accessing unique sectors and companies that may be undervalued compared to those in more developed markets.

Tips for investing in Philippine Stock Market

Educate Yourself.

Before investing, understand the basics of the stock market, including how stocks are bought and sold, what affects stock prices, and the different strategies for stock investing.

Start Small.

If you’re a beginner, it’s wise to start with a small investment that you can afford to lose. This approach allows you to learn and gain experience without risking too much.

Know your Risk Profile.

Are you cautious or are you a risk taker? Your personality should reflect the stocks you buy. There are stocks that are volatile, with a great potential to go up but also a great potential to go down.

Some are just steady but when the market goes down, the impact to the company won’t be as bad. Consider what type of stock would fit your level of comfortability.

Diversify your Portfolio.

Don’t put all your money in one stock or one sector. Spreading your investments across different stocks and sectors can reduce risk and increase potential returns over time.

Invest for the Long Term.

The Philippine stock market can be volatile in the short term, but historically, it has provided positive returns over the long term.

Consider investing with a long-term perspective and avoid making decisions based on short-term market fluctuations.

Do your Research.

Before investing in any stock, research the company thoroughly. Look into its financial health, growth prospects, competitive position in the industry, and any news that might affect its stock price.

Buy Low, Sell High.

Buy stocks only when the price is below the “Buy Below Price”. The Buy Below Price is a level at which capital appreciation potential is already attractive relative to the fair value estimate. Any price below this is considered optimal to buy.

Set Clear Goals.

Understand why you’re investing and what you want to achieve with your investments. Setting clear, achievable goals can help guide your investment decisions and strategies.

4. Modified Pag-IBIG 2 (MP2) Savings

| Minimum Investment: | ₱500 |

| Risk Level | Low |

| Average Returns | 7.03% (2022) |

The Modified Pag-IBIG 2 (MP2) is a savings program available to existing and former Pag-IBIG Fund members with at least an equivalent of 24 monthly savings. They may leverage higher dividend earnings versus that of the regular Pag-IBIG Savings program.

For as little as ₱500, you can take part in a program that lets your money earn as much as 8.11% in dividends (their highest ever recorded dividend rate).

Their 3-year average is a solid 7.65% per annum1, way better than what you could get from bank savings accounts or other investment vehicles. You can withdraw your earnings annually or get the lump sum dividend when the fund matures (5 years).

How to Invest in Pag-IBIG MP2?

Enrolling under the Pag-IBIG MP2 program couldn’t be easier. Simply get a copy and complete the MP2 Savings Application form and submit it with copies of a valid ID and passbook or ATM card of your nominated bank.

You can get the MP2 Savings Application form from your nearest Pag-IBIG Fund branch or download it from here.

Or you can visit this page and complete the required fields.

5. Mutual funds & UITF

| Minimum Investment: | ₱1,000 (Mutual Funds); ₱10,000 (UITFs) |

| Risk Level | Medium |

| Average Returns | 5 – 10% per year |

A Philippine Mutual Fund is an investment company registered with the Securities and Exchange Commission (SEC), which pools money from many investors creating a massive fund under a common objective.

This fund is then invested in specific types of securities to achieve the stated objective.

The Unit Investment Trust Fund (UITF), on the other hand, has similar functions of a mutual fund. The main difference is that the fund is managed by a bank instead of a mutual fund company.

This type of investment is ideal for young and new investors because it allows them to access a diversified portfolio managed by professional fund managers, reducing the risk compared to investing directly in individual stocks or bonds.

These investment vehicles offer the potential for higher returns over time, especially for those who may not have the expertise or time to manage their investments actively.

There are four main types of mutual funds and UITFs offered:

| Money market funds | Short-term debt instruments (one year or less). |

| Bond funds | Long-term debt instruments offered by governments or corporations. |

| Balanced funds | A mix of shares of stock and bonds. |

| Stock or equity funds | Primarily shares of stock. |

Tips for Investing in Mutual Funds & UITFs

Determine Your Investment Goals.

Like with any other investment, you must know why you’re investing. Is this for your retirement, leisure, or capital for your future business endeavors?

Be clear on where you want this to go to make the best decisions. Newbies may become disheartened when they see losses even if they still haven’t reached the end of their time frame. Similar with stocks, you must be patient enough to see your investments grow.

Understand Different Types of Funds.

Familiarize yourself with the various types of mutual funds available, such as equity funds, bond funds, index funds, feeder funds, and balanced funds. Each type has its own risk and return profile.

Research Fund Performance.

While past performance is not a guarantee of future results, understanding how a fund has performed in different market conditions can provide insight into its management and strategy.

Check the Fees.

Be aware of all the fees associated with mutual fund investments, including management fees, administrative fees, and sales charges. High fees can significantly eat into your returns over time.

Review the Fund Manager’s Track Record.

The fund manager’s experience and track record can impact the fund’s performance. Look for funds managed by individuals or teams with a proven history of success.

Consider Diversification.

Investing in a mix of mutual funds can help spread risk. Consider diversifying across different asset classes, sectors, and geographical regions.

Read the Prospectus.

Before investing, read the fund’s prospectus carefully. It contains important information about the fund’s objectives, strategies, risks, and fees.

Think Long-Term.

Mutual fund investing often works best as a long-term strategy. Be prepared to ride out short-term market fluctuations to achieve potential long-term gains.

Add Regularly.

Although you can start at a low price of ₱1,000 and there is no required regular addition, it is advisable to add regularly and use it as kind of your piggy bank for your long-term goals.

Assess Risks.

All investments have their risks, so it’s important to do risk assessments. Online brokers who offer mutual funds usually have their risk assessment questionnaire which will help you decide which type of mutual fund is best for you.

6. Bonds

| Minimum Investment: | ₱5,000 |

| Risk Level | Low |

| Average Returns | 2% to 5% annually (Government bonds); 4% to 8% (Corporate bonds) |

Investing in bonds in the Philippines offers a relatively stable and predictable income through regular interest payments, making them an attractive option for conservative investors seeking lower-risk investments.

Bonds work similarly to loans, except in terms of who borrows the money.

Say a company needs ₱1 million to expand its operations. They have two options: they can either borrow from banks (loans) or they can issue bonds.

With loans, banks will provide the company with a lump sum that they’ll have to pay based on the interest rate and other terms that the banks have set. In most cases, the company will be asked to pay in monthly terms, with the interest embedded in each payment.

With bonds, it’s like doing a reverse loan.

Instead of the company approaching the lender (bank), they will print a bond (contract) that might state, “In five years, our company will pay the owner of this bond ₱50,000”.

Since they need ₱1 million, they decide to print 20 pieces of these ₱50,000 bonds and issue them to institutional investors and the public. Aside from receiving the promised ₱50,000 face value back after five years, bondholders will also receive “coupon payments”.

For example, let’s say that the ₱50,000 bond in our example features a 5% annual interest rate.

Each year, the company will have to pay the bond owner ₱2,500 for five years. In total, the bondholder would get ₱12,500 in earnings after the bond matures (₱2,500 x five years).

But it doesn’t stop there. Since bonds are classified as IOUs (debt instruments) and can be circulated publicly, they can be traded—like stocks.

It’s possible that a bond can be sold at a higher price than its face value if the net present value of the principal and interest payments have increased.

But if the bond owner decides to hold on to it until it matures, he or she gets back the original investment (making it a good way of preserving capital) plus earnings from interest (passive income).

Related Guide: How to Invest in Fixed Income Securities in the Philippines

Different Types of Bonds in the Philippines

Bonds are generally classified into two: by maturity or by the issuer.

- Maturity-based bonds – Classified according to the length of time it will mature

- Treasury Bills (T-bills) – Mature in less than one year (short term). The most common tenors (length of maturity) for T-bills are 91 days, 181 days, and 364 days.

- Treasury Bonds (T-bonds) – Matures in more than one year. The most common maturity lengths for T-bonds are 2-year, 5-year, 7-year, 10-year, 20-year, and 30-year bonds.

- Issuer-based bonds – Classified according to who issued it

- Treasury Securities – Issued by the Bureau of Treasury

- Government Bonds – Released by various government agencies like Home Development Mutual Fund (HDMF or Pag-IBIG), Government National Mortgage Association (GNMA), Federal National Mortgage Association, and others.

- Municipal Bonds – Distributed by the local government units (LGUs)

- Corporate Bonds – Supplied by public and private companies

How to Invest in Bonds in the Philippines

For corporate bonds, some banks advise the general public through their official website or mailing list. Information and requirements for investing in bonds are typically posted on their website.

Some will have you complete a quick online questionnaire to get your details and contact info. Afterward, a representative from the bank will call/email you to discuss the details and next steps.

For Government bonds like T-bonds, you can visit the Bureau of Treasury website for updates and listings for any upcoming public offerings.

You can also reach out to banks and check if they have any government bond offerings.

Like with corporate bonds, they’ll provide you with details and instructions along with the paperwork to complete should you wish to proceed with the investment.

7. SSS WISP Plus

| Minimum Investment: | ₱500 (per payment); Amount varies for SSS WISP Plus, around 14% in excess of Php20,000 MSC (monthly salary credit) |

| Risk Level | Low |

| Average Returns | 6.39% (2022) |

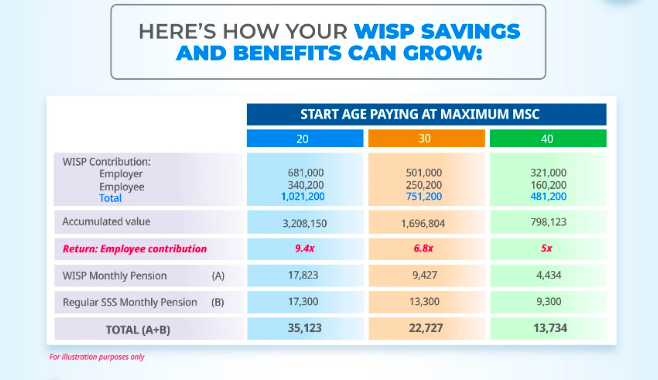

The Worker’s Investment and Savings Program or WISP was launched in 2021 under the SSS Law of 2021. It is a compulsory provident fund for SSS members with a monthly salary credit of more than Php20,000.

This investment offers market-based returns to ensure that your contributions increase over time. This is also tax-free and may be claimed as an annuity or lump sum. Considering this, it acts as an additional source of pension when you retire.

Designed specifically for those who have more funds to invest, specifically those with Php20,000 to Php30,000 (2023 and 2024), and up to Php35,000 (2025 onwards), employer-shared contributions are applicable for this investment vehicle.

Meanwhile, OFW, self-employed, and voluntary members must shoulder their contributions on their own.

Majority of the investments will be in blue chip corporations (25%), and risk-free government securities (minimum 75%).

The principal amount is also always protected. Moreover, 1% p.a. of the total fund will be deducted to members’ accounts to pay for operational expenses.

The SSS reported that WISP collections hit Php35.84 billion in 2023.

SSS WISP Features

- Open to all members of SSS: This is an easy and safe way to give you additional retirement savings with a competitive interest that compounds as you wait for your golden years. All your contributions are safe and will be tax-free in the future.

- Great boost for retirement: As you pay your WISP and SSS contributions, you can have a better nest egg when you retire due to its high interest. Your employer also contributes to this fund so you can truly see your retirement savings grow. The moment you retire, your WISP’s accumulated value may be up to nine times your personal share in contributions. This can help you become more financially secure.

- Options in receiving: SSS members can receive their benefits in an annuity or lump sum. This gives you more flexibility. If you receive it in an annuity, you’ll get a fixed monthly pension until your total value is fully settled. This may take up to 15 years.

SSS WISP Sample Computation

As stated above, MSC above Php20,000 will go to WISP. For instance, if you are paid Php30,000, then the extra amount is Php10,000. The employee’s provident fund is Php450 (Php10,000 x 4.5%). For the employer, it’s Php950 (Php10,000 x 9.5%).

Take a look at this table by SSS to learn more about your WISP contributions.

How to enroll for SSS WISP

If you’re already an SSS member with a monthly salary of over Php20,000 with no claim made in the regular SSS program, you will automatically be enrolled in the WISP.

WISP vs. WISP Plus

WISP is mandatory for all SSS members who receive over Php20,000 per month. Meanwhile, WISP Plus is voluntary, and its focus is on capital preservation. Its investment mix includes:

- At least 15% in government securities. This can be increased up to 100%

- Up to 20% in corporate or multilateral institutions and equities

- Up to 25% in short- and medium-term loans to WISP Plus members (including calamity, salary, livelihood loans, and more)

- Up to 70% in loans to pensioners

- Up to 40% in money market and BSP-approved investment instruments

Just like the WISP, WISP Plus allows members to invest in their future tax-free. The latter also earns more compared to regular savings and time deposits.

Unlike the WISP which can be withdrawn, WISP Plus can only be withdrawn after one year (remaining balance should not be less than Php500).

For earlier withdrawal requests, it can only be done for extreme hardship conditions including repatriation from host country, involuntary separation from employer, critical illness, etc.

Keep in mind that WISP Plus can only be received through a lump sum.

8. High-Yield Savings Accounts

| Minimum Investment: | ₱1,000 |

| Risk Level | Low |

| Average Returns | 4% – 10 % per year |

Investing in high-yield savings accounts provides a safe and liquid option for earning interest on your cash reserves, typically offering higher returns than traditional savings accounts without significantly increasing risk.

These accounts (mostly offered by digital banks) also offer easy access to funds, making them a practical choice for maintaining an emergency fund or saving for short-term financial goals.

What are the Top High-Yield Savings Accounts In The Philippines

There are tons of choices when it comes to high-yield savings accounts in the Philippines. If you don’t have the time to look at each option one by one, this table below is for you:

| Bank | Type | Interest Rates |

| CIMB Bank (GSave) | Digital Bank | 2.6% |

| Tonik Bank | Digital Bank | 4% – 6% |

| Maya Bank | Digital Bank | 3.5% – 14% |

| SeaBank | Digital Bank | 3% – 4.5% |

| GoTyme | Digital Bank | 4% |

| UNOBank | Digital Bank | 4.5% |

| Union Digital Bank | Digital Bank | 3% – 4% |

| OwnBank | Digital Bank | 6% |

Tips to Maximize your Returns and Make the Most of High-Yield Savings Accounts

Shop Around.

Compare high-yield savings accounts across different banks and financial institutions to find the best interest rates and terms. Online banks often offer higher rates than traditional brick-and-mortar banks.

Understand the Terms.

Pay attention to the terms and conditions, including minimum balance requirements, fees, and how often the interest is compounded. These factors can affect the overall return on your investment.

Regularly Deposit Funds.

Make regular deposits into your high-yield savings account to benefit from compound interest over time. Even small, consistent contributions can add up.

Use for Emergency Funds.

High-yield savings accounts are ideal for holding your emergency fund due to their liquidity and safety, ensuring that your funds are accessible when needed.

Monitor Interest Rates.

Interest rates on savings accounts can change, so keep an eye on them and be ready to switch accounts if you find a better rate elsewhere to maximize your earnings.

Automate your Savings.

Set up automatic transfers from your regular savings or checking account to your high-yield savings account to ensure you’re consistently saving without having to think about it.

Stay Within Insurance Limits.

Ensure your deposits stay within the insurance limits of the Philippine Deposit Insurance Corporation (PDIC) to keep your money safe (₱500,000).

Read Reviews and Ratings.

Look at customer reviews and ratings of the bank or financial institution to assess their customer service and reliability.

Consider Using Multiple Accounts.

If you have different savings goals, consider using multiple high-yield savings accounts to segregate your funds and track your progress towards each goal more easily.

Stay Informed.

Keep abreast of economic trends that might affect interest rates, such as inflation rates and monetary policy decisions by the BSP, to understand how they could impact your savings.

9. Upskilling

| Minimum Investment: | time and effort |

| Risk Level | Low |

| Average Returns | High |

Investing in new skills enhances employability and opens up opportunities for higher income, as the country’s evolving economy demands a workforce adept in emerging technologies and industries.

Additionally, upskilling can pave the way for entrepreneurship opportunities, enabling you to expand your network and accumulate wealth over time.

You don’t have to go to a formal school to learn new skills. If you have the money, you can take courses or even get a post-grad degree.

For those who don’t have the money for expensive degrees, there are other alternatives you can consider below.

Tips for Investing in New Skills

Upskilling in the Philippines is essential for staying competitive in the job market and taking advantage of new opportunities. Here are some tips to effectively enhance your skill set:

Identify In-Demand Skills.

Research the skills that are in high demand within your industry or in fields you’re interested in entering. Focus on skills that are likely to remain relevant, such as digital literacy, data science, and specialized technical abilities.

Take Advantage of Online Courses.

Utilize online learning platforms like Coursera, Udemy, Skillshare, and LinkedIn Learning, which offer courses on a wide range of topics.

Many of these courses are created by reputable institutions and companies. Online courses are usually cheaper and may sometimes even be free.

Participate in Workshops and Seminars.

Attend workshops, seminars, and training sessions in your area or virtually. These can provide not only valuable learning experiences but also networking opportunities.

Find Free Resources on the Web (like Grit PH or YouTube).

You can learn any skill for free from watching thousands of videos on any given subject, may it be Bitcoin, Forex, or stocks. You name it, the site has it. The wealth of information you can access is just within your smartphone.

Read Books

Books are investments. If you want solid knowledge on any subject matter, then buying a book on it is always a wise decision.

The trick to reading a book if you’re busy is to look at the table of contents and to just pick chapters that would seem more applicable for you. This way you can focus on what’s essential.

Pursue Further Education.

Consider pursuing further education, such as a degree or certification program, in a field that interests you or is in high demand. Check if your current employer offers educational benefits or scholarships.

Learn from Industry Experts.

Follow industry leaders and experts on social media, read their blogs, and listen to their podcasts to gain insights into trends and valuable skills in your field.

Practice What You Learn.

Apply new skills in real-life projects or through volunteering. Hands-on experience is invaluable and can make your learning more concrete.

Join Professional Networks.

Engage with professional organizations or groups related to your field. Networking can provide insights into industry needs and opportunities for professional development.

Seek Mentorship.

Find a mentor who can guide your learning journey, provide advice, and help you navigate your career path effectively.

Stay Curious and Open-Minded.

Cultivate a mindset of continuous learning and be open to acquiring skills outside of your immediate professional needs. Diverse skills can open unexpected opportunities.

Honorable Mentions

Below are additional investment options previously featured in this list but were excluded from the top recommendations.

We’ve made this decision because some of the following options may be too volatile for beginner investors or may provide limited returns for the more experienced investors.

| Investment Vehicle | Risk Level | Pros & Cons |

| Cryptocurrencies | High | Investing in cryptocurrencies in the Philippines can be a good idea due to the potential for high returns and the growing acceptance of digital currencies as a form of investment and payment. However, it can also be risky due to the high volatility of the market, regulatory uncertainties, and the potential for loss due to hacking or fraud. |

| Forex Trading | High | Investing in forex trading offers the potential for significant profits due to the high liquidity and 24-hour trading environment of the forex market. However, it is risky and complex, requiring a deep understanding of market forces and the potential for substantial losses due to the market’s volatility and the use of leverage. |

| Social Trading | Medium | Social trading (through platforms like eToro) allows investors, especially beginners, to learn from and replicate the trades of experienced traders, potentially accelerating their learning curve and investment success. However, it also carries risks as it depends heavily on the performance and strategies of others, which may not always align with one’s own risk tolerance, values, or investment goals, leading to possible financial losses. |

| Exchange Traded Funds (ETFs) | Medium | Investing in ETFs offer diversification, lower costs, and the flexibility of trading like individual stocks, making them accessible and appealing for a wide range of investors. However, the market for ETFs in the Philippines might be limited compared to global markets, potentially offering fewer options and lower liquidity, which could impact investment strategies and returns. |

| Variable Universal Life Insurance (VUL) | Low | Investing in Variable Universal Life (VUL) insurance in the Philippines can be advantageous as it combines life insurance with investment options, providing both financial protection and the potential for wealth accumulation. However, it may not be suitable for everyone due to its higher costs compared to term insurance and direct investments (BTID), and the investment component’s performance can vary, impacting the policy’s cash value and benefits. |

| Peer-to-Peer Lending | High | Investing in P2P lending offers the potential for higher returns (10 – 15%) compared to traditional savings and investment products, and it allows investors to directly fund borrowers, supporting small businesses and individuals. However, it also carries risks such as the possibility of borrower default, which can lead to the loss of invested capital, and the lack of a regulatory framework may add to the uncertainty and risk profile of these investments. |

| Real Estate Investment Trust (REIT) | Medium | Investing in REITs offers a way to gain exposure to the real estate market with less capital, providing investors with regular dividend payments (6% – 8% dividend yield) and potential for capital appreciation. However, like any investment, REITs come with risks, including market volatility and potential impacts from economic downturns on property values and rental incomes, which could affect returns. |

| Digital Assets | High | Investing in digital assets, like buying websites, taps into the growing digital economy and offers high potential returns through advertising, e-commerce, subscription models, or acquisition. However, it requires technical know-how, constant content updating, and effective monetization strategies, with the risk of rapid obsolescence or declining traffic affecting profitability. |

| Angel Investing & Private Equity | High | Angel investing offers the opportunity to support innovative startups with high growth potential, allowing investors to potentially reap substantial returns if these companies succeed. However, it carries a high level of risk, including the possibility of losing the entire investment if the business fails, and requires a deep understanding of the market and the ability to perform thorough due diligence. |

| Personal Equity and Retirement Account (PERA) | Low | Investing in the PERA provides tax incentives and a structured way to save for retirement, potentially leading to a more secure financial future. However, it may not suit everyone due to its annual contribution limits and the fact that early withdrawal penalties and specific conditions for tax benefits could restrict access to funds for those who may need liquidity before retirement age. |

Investing in the Philippines FAQs

Still got questions about investing in the Philippines? We’ll answer them below.

What is an Investment?

Buyers identify an investment as a purchased item or asset that would grow its value in the future and can be sold at a higher price. It can also be viewed as a property that enables its owners to generate passive income and create wealth over time.

Learn More: How to Invest your Money

What are the different types of investments?

Stocks, bonds, annuities, commodities, real estate—I bet we all scratched our heads the first time we tried to know more about these financial terms. If you’re anything like me, you also probably got overwhelmed with all the technical jargon and got buried with a ton of information that didn’t make sense.

This guide aims to shed light on the different types of investments available out there to help you achieve your financial goals. Learning about them will open ways and ideas for multiplying your money quickly.

Here’s our quick rundown of the different types of investments:

1. Bank Products

Perhaps the most popular and common of all investments, bank products come in different options.

The money you deposited are federally insured to up to a certain limit and can be easily withdrawn. Some examples are savings accounts, certificates of deposit (CDs), money market, and federal insurance.

2. Bonds

Bonds are loans offered by an investor to governments and corporations. In exchange, the borrower must pay the interest on the borrowed money at a predetermined schedule (annual or semiannual) and will need to return the principal on an agreed upon maturity date.

3. Stocks

Put simply, stocks pertain to units of ownership in a corporation. This means that if you own or invest in stocks of a company, you become one of its “owners”.

4. Investment funds

Investment funds come or are sourced from different investors. A mutual fund is one of the most common types of investment fund.

5. Annuity

Annuities promise to pay you a regular or fixed-interval income either immediately or in the future. You must first pay for the annuity in one lump-sum or through a series of payments also known as premiums.

6. College fund

College fees are notoriously expensive, and many people opt to invest in college funds to save money for the future. Depending on the location, earnings from this fund are not subjected to Federal and State taxes, as long as the funds are strictly used for college expenses.

7. Business capital

Simply put, business capital is money that you put into a business to gain active or passive earnings or income.

8. Retirement fund

Retirement funds come in handy as a way to have continuous cash flow. While still able, workers can save money and receive pension upon retirement.

9. Commodity Futures

This agreement or contract allows a person to buy or sell a specified amount of a commodity at a fixed price and future date. This helps protect buyers by negating risks caused by fluctuations in price of the commodity in the future.

10. Security Futures

Similar to commodity futures, security futures lets you purchase and sell a fixed amount of shares of a particular stock at a specified price and future date.

11. Insurance

Insurance protects you against potential financial loss, damage or harm. The insured or policyholder pays premiums to buy a policy that states the terms and conditions in which the insurer is required to pay.

12. Real estate

Real estate investment generates income or profit through purchasing, leasing, managing or selling a piece of realty property for a higher price than it was acquired when the property’s value appreciates over time.

13. Alternative and Complex Products

Alternative and Complex products offer optional investment vehicles outside of traditional stock and bond investments. Some examples of this include notes with principal protection and risky high-yield bonds that have low credit ratings. Most are risky but provide high rates of return.

Related: 8 Best Online Investment Sites & Platforms in the Philippines

How to choose the best investments in the Philippines

But are there really low-risk, high-return investments in the Philippines?

This may sound impossible, but you can find them if you know where to look.

The key is to check low-risk investments such as money market funds and bond funds (through mutual funds or UITFs) with the highest returns.

Money market funds and bond funds are both invested in low-risk, fixed-income securities. Time deposits and government T-bills comprise money market funds, while corporate and government bonds comprise bond funds.

To view and follow the best-performing investments in the Philippines, visit the following sources:

- Investing.com’s Philippines Stocks tracker for daily stocks performance

- Philippine Investment Funds Association (PIFA) website for mutual funds

- Unit Investment Trust Fund Philippines website for UITFs

How much money is needed to start investing in the Philippines?

The short answer: Not much.

If you’re just starting out as an investor, you don’t need five or six-digit figures from the get-go. Anyone, even college students and fresh graduates, can start investing with as little as ₱25 to ₱5,000.

The actual initial investment depends on where you’re putting money in, and the bank or investment company that will handle your funds.

Here are the required initial funds for the common investment options in the Philippines:

| Investment Vehicle | Minimum Initial Investment | Minimum Additional Placement |

| Mutual funds | ₱100 to ₱5,000 | ₱100 to ₱1,000 |

| Stocks | ₱5,000 to ₱1 million | ₱1,000 |

| Time deposit | ₱1,000 to ₱100,000 | N/A |

| Unit Investment Trust Fund (UITF) | ₱25 to ₱10 million | ₱50 to ₱1 million |

How to start investing with little money

The advantage of growing your money through investments is that you can start small.

There’s no excuse from getting started even if you’re a breadwinner with a lot of bills to pay, as you can increase the amount you invest later on when you’re more financially capable.

But it’s important to note that you should never begin an investment journey without a solid strategy.

Take these initial steps to invest even with a small amount of money.

1. Determine how much you can afford to invest.

This step is crucial if you plan to invest regularly in the long term.

You don’t want to invest a certain amount initially and then stop it altogether after a few months because you could no longer afford the monthly, quarterly or yearly investments.

Before you start off, set a realistic and reasonable amount to invest, considering your income, expenses and savings.

2. Save up for your emergency fund.

A common mistake many first-time investors make is jumping right into investing without having an emergency fund.

When a financial emergency happens (like the hospitalization of a family member or the need for home repairs after a typhoon) without emergency funds stashed away, you’ll have no choice but to withdraw your funds or sell stocks prematurely.

Ideally, you need to build an emergency fund equal to six to 12 months’ worth of living expenses, before starting to invest.

Make the process easier by putting away a small amount every week or payday.

The Philippine Stock Exchange (PSE) recommends putting the emergency fund in short-term, liquid investments such as savings accounts and time deposits.

You can invest the rest of your savings in medium-term or long-term instruments, depending on your financial goals.

3. Put your money in low initial investment vehicles.

Look for investment opportunities that allow you to begin investing with a minimal amount.

The best financial instruments for this purpose are mutual funds and UITFs. When you put your money in these instruments, you can invest in a diversified portfolio of bonds and stocks with just a single transaction. Here are your options in the Philippines with initial investments ranging from ₱25 to ₱1,000.

| Mutual Funds | ||

| Fund Name | Minimum Initial Investment | Minimum Additional Placement |

| Sun Life Prosperity Money Market Fund | ₱100 | ₱100 |

| Philam Managed Income Fund | ₱1,000 | ₱500 |

| Philam Bond Fund | ₱1,000 | ₱500 |

| Sun Life Prosperity Bond Fund | ₱1,000 | ₱1,000 |

| Sun Life Prosperity GS Fund | ₱1,000 | ₱1,000 |

| ATRAM Philippine Balanced Fund | ₱1,000 | ₱600 |

| Philam Fund | ₱1,000 | ₱500 |

| Sun Life Prosperity Balanced Fund | ₱1,000 | ₱1,000 |

| ATRAM Alpha Opportunity Fund | ₱1,000 | ₱ 600 |

| ATRAM Philippine Equity Opportunity Fund | ₱1,000 | ₱600 |

| Sun Life Prosperity Equity Fund | ₱1,000 | ₱1,000 |

| PAMI Equity Index Fund | ₱1,000 | ₱500 |

| Sun Life Prosperity Philippine Stock Index Fund | ₱1,000 | ₱1,000 |

| UITFs | ||

| Fund Name | Minimum Initial Investment | Minimum Additional Placement |

| Unlad Kawani Money Market Fund | ₱25 | ₱25 |

| ATRAM Peso Money Market Fund | ₱50 | ₱50 |

| ATRAM Total Return Peso Bond Fund | ₱50 | ₱50 |

| ATRAM Philippine Equity Smart Index Fund | ₱1,000 | ₱1,000 |

| ATRAM Global Dividend Feeder Fund | ₱1,000 | ₱1,000 |

| ATRAM Asia Equity Opportunity Feeder Fund | ₱1,000 | ₱1,000 |

| ATRAM Global Technology Feeder Fund | ₱1,000 | ₱1,000 |

| BDO PERA Short Term Fund | ₱1,000 | ₱1,000 |

| BDO Merit Fund | ₱1,000 | ₱1,000 |

| BDO PERA Bond Index Fund | ₱1,000 | ₱1,000 |

| BDO Institutional Equity Fund | ₱1,000 | ₱1,000 |

| BDO PERA Equity Index Fund | ₱1,000 | ₱1,000 |

What are the different types of Investment Strategies?

Investment strategies can vary widely depending on the goals, risk tolerance, and time horizon of the investor. Here are some of the most common types of investment strategies:

- Growth Investing

- Value Investing

- Passive Investing

- Active Investing

- Momentum Investing

- Dividend Investing

- Income Investing

- Indexing

- Contrarian Investing

- Diversification

- Dollar-cost Averaging

How to determine your Investment Risk Appetite

Your risk appetite as an investor refers to the amount of risk you can take in pursuit of your investment goals. After all, “no pain, no gain,” right?

An individual’s investment appetite can vary wildly depending on different factors so there’s no clear standard for what a good risk appetite looks like. If you want to determine your risk appetite, take a look at the factors below.

Investment goal

Your investment goal will largely influence your risk appetite. Think of why and when you want to use your investment money for. A person who is investing to pay for a house down payment will have a different risk tolerance from someone who is investing to pay for a week-long holiday.

If you are an aggressive investor who is okay with taking on more risk for more potential reward, then you can afford to invest in higher-risk assets. Meanwhile, a conservative investor with a low-risk appetite will favor investments that lessens the risk of losing money.

Investment timeframe

Different people have different time horizons. Investors that have a longer time horizon can afford to take more risks.

Current income and savings

Your current income and savings are other major factors in determining your risk appetite.

Those who earn more money and have huge savings can have a greater risk appetite since they have a better financial cushion to catch their fall. On the flip side, if you don’t have enough disposable income, you can’t afford to lose much money on investments.

Keep in mind that there is no right or wrong risk appetite. The answer largely depends on your unique situation.

Learn More: Investment Risk Management Strategies

What’s the best investment for beginners?

Beginner investors in the Philippines can benefit from very low barriers to entry.

Some of the best investments beginners should take advantage of include Pag-IBIG MP2 and SSS, which are two of the most common investments in the country.

You can start for as low as Php1,000 for the SSS PESO Fund, and Php500 for Pag-IBIG MP2. These investments are also guaranteed by the Philippine government, and most of all, they are tax-free.

Other investments for beginners include stocks and mutual funds, UITFs, and VULs.

Always keep in mind that before you start investing, you should first have your emergency fund. This is ideally 6 times your monthly salary. You may store this in a high-yield savings account that pays you interest based on your cash balance.

Related: How to Build Wealth in your 20s

What are the top 5 investments for building a portfolio?

There is no such thing as a perfect investment portfolio for everyone.

When you’re building your investment portfolio, there are key things you should account for such as your time horizon, investment strategy, goals, and risk appetite.

That said, five of the most popular investments today include emerging market stocks, blue-chip stocks, fixed-income securities, real estate, and certificates of deposit.

What are the best alternative investments in the Philippines?

If you’re ready to diversify your portfolio, investing in alternative assets is an amazing idea. These investments cover assets that are not stocks, bonds, or cash. The best alternative investments today include:

- Real estate crowdfunding platforms

- P2P lending

- Cryptocurrencies

- Private equity and venture capital

- Arts, collectibles, and antiques

- Commodities

- NFTs

Want to learn more about these alternative investments? Check out our in-depth guide here.

How are investments taxed in the Philippines?

In life, there are two things you can’t avoid: death and taxes. Here’s how investments are taxed in the Philippines.

| Passive income | Tax rates |

| Interest from currency deposits, trust funds, and deposit substitutes | 20% |

| Cash and/or property dividends received by an individual from a domestic corporation/joint stock company/insurance or mutual fund companies/ Regional Operating Headquarter of multinational companies | 10% |

| Capital gains from sale, exchange, or other disposition of real property located in the Philippines, classified as capital asset | 6% |

| Net Capital gains from sale of shares of stock not traded in the stock exchange | 15% |

| Interest income from long-term deposit or investment in the form of savings, common or individual trust funds, deposit substitutes, investment management accounts and other investments evidenced by certificates in such form prescribed by the BSP. Upon pre-termination before the 5th year, there should be imposed on the entire income from the proceeds of the long-term deposit based on the remaining maturity thereof: Holding period: 4 years to less than 5 years 3 years to less than 4 years Less than 3 years | Exempt 5% 12% 20% |

Disclaimer: All information listed in this article is for information purposes only. Although utmost effort was made to ensure accuracy of information on this website, readers must not solely rely on it in making any investment or financial decision since it does not take into consideration the risk tolerance, financial situation, investment goals, and experience of readers. It is best to consult a professional financial planner or your bank before investing to make a more informed choice and limit your risk exposure.

Read Next:

Passive Income Ideas: 12 Ways to Make Money While You Sleep

Passive Income Ideas: 12 Ways to Make Money While You Sleep- How to Invest in Real Estate in the Philippines [Ultimate Guide]

- How to Invest in Bonds in the Philippines

- How to Invest in UITFs in the Philippines

- How to Invest in Mutual Funds in the Philippines

- How to Invest in Peer-to-Peer Lending: Top 4 P2P Lending Sites in the Philippines

- Value Investing: Tools, Techniques, and Strategies

- How to Invest in Forex in the Philippines

![How to Invest in Real Estate in the Philippines [Ultimate Guide]](https://grit.ph/wp-content/uploads/2023/07/real-estate-investing-150x150.png)

I WILL FOLLOW IT ALL THANKS

Hello Chora! I am a financial adviser of manulife philippines. I can help you realize ur investment dreams.

I made a comparison matrix of popular VUL policies in the market (Sunlife, Axa, Manulife, Insular Life, Bpi-Philam/Philam Life, Prulife). But first…..

Among VUL, mutual funds, UITF, and direct stock trading, only VUL offers simultaneous life protection, growth of money thru investing, and the many supplementary benefits (cash assistance when hospitalized, or upon diagnosis of critical illness, etc.)

With regards to investment, it would also be prudent for starting investors to enter pooled funds instead of direct stock trading unless he has large capital to invest in blue chip stocks, and has the time and diligence to track market movement from time to time, since one can really maximize earnings by trading.

With regards fund performance among pooled funds (VUL, mutual funds, and UITF), best fund managers in the country are employed in Life Insurance Companies, which offer VUL products, hence annualized returns are higher in VUL by historical performance. And among several VUL products, there are actually few funds that really stand-out. And these funds are available only in select few Insurance Companies.

If you are interested in availing VUL policy, I suggest you get as many proposals from different Insurance Companies as possible. DO NOT compare the products by the illustrated projected fund values through the years. As stated, these are PROJECTIONS, and all are mandated by Insurance Commission to show projected earning rates at Low (4%), Medium (8%), and High (10%). Different companies also offer different protection coverage periods. Some guarantees up to 99 or 100 years old, some are only up to 80 to 88 years old, so one may be swayed to get a “less expensive” policy, but this is not actually case and when you do the math, he/she is actually paying more for relatively shorter coverage, and this is not only for the life coverage but includes also for supplementary benefits (critical illness, accidental death benefits, etc.)

Lastly, keep in mind that when Financial Planners present to you a VUL policy which would require limited-term pay (5-yr/7-yr/10-yr), it is NOT guaranteed that you will only pay up to this period. VUL is investment-linked, and all will depend on the actual fund performance. Same goes with regular pay- it is NOT true also that you will pay continuously, so look for a premium holiday feature (with no premium holiday charges).

If you are interested to learn more, I was able to make a comparison matrix of all VUL products, and these cover 2-groups – Investment-Oriented and Protection-Oriented Products. I had 19 criterias as basis of for my evaluation when choosing which company gives more value to the premium (investment) that I pay, as one will be suprised that some companies charge more than other companies (and this does not include yet the hidden charges- you will only realize that it is hidden when you understand complex terminologies in the VUL policy).

Example of my criterias are: fund performance (annualized ROI/assets), market capitalization, pricing policy (single or dual), protection coverages, premium and monthly deduction charges, rules on policy lapsation, effect on short-term non-payments, etc… I also made an analysis about the pros and cons of regular pay and limited-term pay. Actually, a lot of Insurance Agents offer limited-term pay since it requires higher minimum, and with higher premium the more commission.

If you want to umderstand more, you can contact me. This is my email: emg12316@gmail.com and my number 0917-5662845

hi Kiel

can u send me more details about this insurance plan.

thank you so much for the tips i will advise my kids

Thanks big help 😊

#BUYBITCOIN

Thank you..It helps me a lot

thank you

Thank you..

You did not include cooperative..

SmartCash is the best investment in the world of cryptocurrency. Believe me i’m in there!

good job

A lot of young professional’s money will get slaughtered in the first 9 of the 10 tips mentioned. Due your due diligence before making an article like this. To the yappies, follow the advice at your own peril.

Very good read! Thank you for sharing these valuable information. God bless

Now is the best time to invest in stocks. Taking advantage of the market crashing from the corona virus! Stocks are at all time low hat will obviously bounce back. It’s a no brainer!

I’m an OFW and this article is very helpful.

I made a comparison matrix of popular VUL policies in the market (Sunlife, Axa, Manulife, Insular Life, Bpi-Philam/Philam Life, Prulife). But first…..

Among VUL, mutual funds, UITF, and direct stock trading, only VUL offers simultaneous life protection, growth of money thru investing, and the many supplementary benefits (cash assistance when hospitalized, or upon diagnosis of critical illness, etc.)

With regards to investment, it would also be prudent for starting investors to enter pooled funds instead of direct stock trading unless he has large capital to invest in blue chip stocks, and has the time and diligence to track market movement from time to time, since one can really maximize earnings by trading.

With regards fund performance among pooled funds (VUL, mutual funds, and UITF), best fund managers in the country are employed in Life Insurance Companies, which offer VUL products, hence annualized returns are higher in VUL by historical performance. And among several VUL products, there are actually few funds that really stand-out. And these funds are available only in select few Insurance Companies.

If you are interested in availing VUL policy, I suggest you get as many proposals from different Insurance Companies as possible. DO NOT compare the products by the illustrated projected fund values through the years. As stated, these are PROJECTIONS, and all are mandated by Insurance Commission to show projected earning rates at Low (4%), Medium (8%), and High (10%). Different companies also offer different protection coverage periods. Some guarantees up to 99 or 100 years old, some are only up to 80 to 88 years old, so one may be swayed to get a “less expensive” policy, but this is not actually case and when you do the math, he/she is actually paying more for relatively shorter coverage, and this is not only for the life coverage but includes also for supplementary benefits (critical illness, accidental death benefits, etc.)

Lastly, keep in mind that when Financial Planners present to you a VUL policy which would require limited-term pay (5-yr/7-yr/10-yr), it is NOT guaranteed that you will only pay up to this period. VUL is investment-linked, and all will depend on the actual fund performance. Same goes with regular pay- it is NOT true also that you will pay continuously, so look for a premium holiday feature (with no premium holiday charges).

If you are interested to learn more, I was able to make a comparison matrix of all VUL products, and these cover 2-groups – Investment-Oriented and Protection-Oriented Products. I had 19 criterias as basis of for my evaluation when choosing which company gives more value to the premium (investment) that I pay, as one will be suprised that some companies charge more than other companies (and this does not include yet the hidden charges- you will only realize that it is hidden when you understand complex terminologies in the VUL policy).

Example of my criterias are: fund performance (annualized ROI/assets), market capitalization, pricing policy (single or dual), protection coverages, premium and monthly deduction charges, rules on policy lapsation, effect on short-term non-payments, etc… I also made an analysis about the pros and cons of regular pay and limited-term pay. Actually, a lot of Insurance Agents offer limited-term pay since it requires higher minimum, and with higher premium the more commission.

If you want to umderstand more, you can contact me. This is my email: emg12316@gmail.com and my number 0917-5662845

thanks for this info it helps a lot specially when looking for various VUL offered by different companies around. If you permit can I see your comparison matrix? Thanks a lot

Hi Aldrin,

Yes, you can contact me in my email: emg12316@gmail.com or thru my number 09175662845

very nice read.. thank you

thanks for the information .i like small business with small capital

I can recommend one Mr. Drigo contact me at 0920-922-4027

I like small business with small capital too.

Any idea pls? thank you.

Check out our massive list of business ideas here: https://grit.ph/business-ideas/

Thanks for reading, Yhan.

Hello

I just to inquire what are the investment that high in interest rate?

NICE ARTICLE FOR US OFW’S

Good day! I am Marjorie Anne Mena, licensed Property Specialist from Avida Land Corp., A subsidiary of Ayala Land Inc., known to be the best in Business District Development.

We have lots of great condominium projects within Metro Manila, exclusive, secure, and organized residential and office community respectively, with residential, retail, medical, business, and lifestyle options or what we called “mmixed-used community”.

If you are interested to invest in Real Estate business, I am willing to help you get your own, now!

You may reach me thru these:

Globe 0936-444-8514

Smart 0921-393-1923

Email: menamarjorie11@gmail.com

For reference to fund performance of different investment vehicles (VUL, Mutual Funds, and UITF), you may refer to this link:

https://www.entrepreneur.com.ph/news-and-events/entrepreneur-ph-guide-to-investment-funds-2017-a36-20170217-lfrm

One needs to understand the difference of Annualized and Absolute Return. It would be straightforward to make a comparison of different funds and distinguish which funds are superior or perform better if the inception dates and time duration of subject funds are the same.

Unfortunately in reality, investment funds have different inception dates. You can actually verify inception dates from Fund Fact Sheets. In the example given from this article, all three (3) funds have the same inception dates, and the author used the equity fund of one insurance company. But you will identify in the link I posted earlier that there are actually VUL Funds that perform better than their counterparts, and these VUL Funds are even superior than Mutual and UITF fund counterparts

Without knowledge of how investments perform, an investor could be committed to an inferior investment and never even know it. An Annualized Return figures the investment’s average annual return or how much the investment has grown on a yearly basis for a specified period of time, while the Absolute Return measures the overall return for the entire period you’ve held the investment since inception date.

For example, a 5-Year Annualized Return at Year 2018 will tell you how much return your investment has generated on a yearly basis from Year 2013 up to Year 2018 (5-year duration). On the other hand, an Annualized Return Since Inception will tell you the average annual return of your investment since the inception date, hence if the fund’s inception date is Year 2009, that would be average annual return for nine (9) years. Therefore, Annualized Returns are very useful when you want to compare two different funds or investment vehicles (of the same category) where time duration and/or inception dates are different.

Each Insurance and Investment Company will show you numbers in the way they look attractive to them to sell it to you. But in my experience, annualized returns (with consideration of Assets Under Management) are the most effective way to calculate the returns and compare fund performance of different Variable Life (VUL)-investment linked products.

If you want to understand more, you can contact me. This is my email: emg12316@gmail.com and my number 0917-5662845

Thanks

Reply

Im very much interested in your inputs sir. Can you kindly send me an email regarding more of this. I want to know more. Thanks and God bless. Here’s my email: pvpenillanm11087@yahoo.com

If you have any questions, you may email me at: emg12316@gmail.com or you may text/call me at: 0917-5662845. Just to share a little background of myself, I currently have one (1) Investment-Oriented VUL Product, one (1) Protection-Oriented VUL Product, and two (2) Certificate of Participation for UITF.

I wrote in my previous post that there are VUL Funds offered by select few Insurance Companies that have shown superior fund performance over their Mutual Fund and UITF counterparts. At this point, I would like to explain another important benefit of VUL Product- The Total Disability Waiver.

1. Note that Variable Life Policies are investment-linked products, which means that so long as the Fund Value/Account Value/Full Withdrawal Value is not zero (0) and is sufficient to cover the monthly deductions, the plan will not terminate, and the insured person is covered with minimum guaranteed benefits. The minimum guaranteed benefits in most VUL Policies are presented in Item Nos. 2/3/4 below. Is it possible to have a Fund Value less than zero (0) or negative during the early years into the policy? The answer is YES and No. If a VUL Product has no Contract Debt Feature, it is possible that Fund Value will become negative in the early years of the policy, and Policy Owner will then be required to make a top-up payment. However, some VUL Products provide Contract Debt Feature, and this will prevent the Fund Value to be negative during the early years of the policy. Therefore, always look for the Contract/Policy Debt Feature in a VUL Product.

2. What is the 1st minimum guaranteed benefit per Item No.1? This would be the death benefit of the policy. This represents the “Face Amount” or “Benefit Amount” of the policy that will be paid out on a tax-free basis to whoever the Owner and/or Irrevocable Beneficiary of the policy is. This is equal to 500% of the basic monthly premium or the Policy Face Amount whichever is higher.

3. What is the 2nd minimum guaranteed benefit per Item No. 1? This would be the accidental death benefits. In most VUL Policies, this is a built-in feature in the product already. However, there is one Protection-Oriented VUL Product that I know that offers accidental death benefits as an optional rider only, which means the rider can be detached, and therefore savings on the overall Rider Premium. The Additional Death Benefit provides additional coverage of up to 100% of the Face Amount or Benefit Amount if death is due to accident.

4. What is the 3rd minimum guaranteed benefit per Item No. 1? This would be the Total Disability Waiver. This is a built-in feature in VUL Policies without charge. This waiver of premium rider pays all Basic (Life insurance and Investment Allocation) and Rider (Supplementary Benefits) Premiums due if the insured person becomes disabled and unable to perform work.

5. The waiver of premium benefits the less well-off policy owners the most, because they would least be able to cope with paying for all future premiums if they become completely disabled, and this include the premium that is allocated to investment (cash value). This can provide the insured person with potential passive source of income (thru partial withdrawals in the policy) if the insured person becomes injured and/or disabled, hence unable to work or perform the key income producing duties. Passive income comes from earnings that one receives with little or no work required. For this case, passive income would refer to investment earnings.

6. A Term Life Insurance Policy (referred to as TERM in BTID or “Buy TERM and Invest the Difference”) is a type of insurance plan that offers financial security to the family of the insured upon Insured’s death. When the insured person dies within the period covered, his beneficiaries get paid. If nothing happens to the insured person within the term, he/she does not get anything. While optional riders can be attached to a Term Life Insurance Policy for more comprehensive coverage (similar to VUL riders), it would not still be able to level the coverage of Total Disability Waiver Benefit for VUL Product as premiums do not earn cash value. Note that in a VUL Policy, the waiver of premium includes the amount that is allocated for investment, which cannot be applied in a Term Insurance Policy.

7. In relation to Item No. 6, this is one of the reasons why VUL Products continus to be more appealing and valuable to people. A total disability or being unable to work due to injury (i.e. when a classical musician permanently injures his arm) will inevitably decrease a person’s income. When insured person becomes disabled, it makes much more difficult for him/her to save money and will impact the retirement plans. With less savings, and less ability to add money to savings, a total disability will have a significant and negative impact on a person’s net worth, which is the amount that he/she is able to save for retirement, and the amount that he/she will be able to pass along to his/her beneficiaries.

Thank you.

In continuation on the previous post..

If you have any questions, you may email me at: emg12316@gmail.com or you may text/call me at: 0917-5662845. Just to share a little background of myself, I currently have one (1) Investment-Oriented VUL Product, one (1) Protection-Oriented VUL Product, and two (2) Certificate of Participation for UITF.

At this point, I would like to address a popular misconception that a VUL Policy is more expensive, and yet offers inferior benefits on the life insurance and investments of the insured person compared to BTID (Buy Term and Invest the Difference).

8. In a VUL Policy, every time one pays a premium, a certain percentage of the premium goes toward premium expense charges and the balance goes towards the Cost of Insurance and Cash Value (investment portion). Premium expense charges include administrative fees, commissions, and the life insurance company’s overhead.

9. In my own opinion, I see nothing wrong with giving sales commissions to Financial Advisers or Insurance Agents, especially if they are really providing holistic and personalized service to their clients. This include regular updates on the fund performance and giving recommendations when to make fund switches or apply changes to the fund allocations in the policy. Note that same with Mutual Funds and UITF, one can really maximize the returns of his/her investments by making strategic fund switches and changes in fund allocations. Oftentimes, the facilities offering Mutual Fund and UITF Products provide only transactional service, which means that after an investor gives his/her investment, Mutual Fund and UITF Brokers/Agents may not bother to do periodic monitoring and reporting of fund performance to the investor.

10. In relation to No. 9, Financial Advisers or Insurance Agents, at their own expense, had to pass two (2) rigorous licensing exams and register with an official regulating body- in the Philippines it would be the Insurance Commission. Afterwards, they had to do several prospecting, and if successful, set meeting with their prospect Clients. Note that the Insurance Company does not pay its Financial Advisers and Insurance Agents with a daily or monthly allowance. Financial Advisers or Insurance Agents will have to spend their own money for business-related expenses (phone bills when calling the client, transportation expenses when meeting the client, internet usage when drafting and sending product proposals online, miscellaneous expenses such us purchase of coupon bonds and printing of product proposals, etc.), not to mention the challenges they face when chasing tough potential clients.