Abstract

Capitalism is often described as a “growth machine,” whose insatiable growth imperative(s) must either be halted to protect ecologies or repurposed by some kind of socialist or social democratic state. However, the continuation of robust growth rates in many countries seems unlikely under present conditions. As monopoly capital scholars have long theorized, late-stage capitalist economies are characterized by a “cancerous malaise” of secular stagnation. In accordance with this perspective, financialization emerged to overcome challenges associated with this cancerous malaise. Using the U.S. economy as a case study, low growth and accelerating accumulation are interlinked under the socio-historic conditions of monopoly finance capital. This interrelation is captured by the term “stagnation-accumulation treadmill,” which stresses that the expansion of finance ensures the systemic requirement to increase material throughputs despite rising obstacles to robust growth. I argue that this interrelationship can help explain the paradox of increased consumption in the Global North alongside increased economic immiseration of the non-propertied working class. This argument stresses the continued materiality of a growth-dependent capitalist economy, even—if not especially—one characterized by stagnation and the explosion of so-called “non-real” finance sectors.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

“Emissions reflect choices, not the level of GDP,” wrote New York Times Columnist and Nobel Prize–winning economist Paul Krugman in an August 2022 tweet. Krugman’s entrance into the “degrowth debate” signifies the decreasing hegemony of the once gospel-truth that growth is good. Significantly, in July 2022, the New York Times interviewed steady-state economist Herman Daly who declared that our “obsession with growth” must end if we are to meet environmental objectives. Beyond the pages of the Times, degrowth occupies the interests of numerous back-and-forth Substack columns and ongoing Twitter (“X”) debates. This discourse pairs well with increasingly mainstream concern about the capacity of contemporary capitalist economies to return to the high growth rates witnessed during the mid-twentieth century and its so-called “golden age” of capitalism (Probst 2019).

In this context, calls for “degrowth,” flourish. Degrowth is the notion that we must halt the capitalist growth imperative in favor of at least a steady-state-style economy that incorporates ecological limits into its operating logic. Advocates of degrowth usually stress the need for rich countries to reduce their net consumption of ecological resources, or material footprints, in a fashion that accords with ecological and social justice–oriented calls for equitable distribution of resources (Hickel 2021a, b; 2021a, Klitgaard and Krall 2012; Kallis et al. 2012; Kallis 2011). However, critics of degrowth assail it for what they see as a politics of austerity that shifts blame from the hidden abode of production to the Global North, working-classFootnote 1 consumer (Huber 2022a, b; Phillips 2015; 2019).

As environmental political economists debate the merits of degrowth, the articulation of a clear and consistent understanding of economic growth and its underlying imperatives prove elusive. In affluent countries, economic growth is anemic, insufficiently innovative, and underproductive. Further, economic growth in rich nations is no longer governed by antiquated mechanisms of “competitive capitalism,” that spur investment, bold risk-taking, and other qualities usually associated with capitalism’s supposed nature as a historical force of progress. These are a few of the general insights of modern capitalism made by thinkers informed by the monopoly capital school—a heterodox, Marxian political economic framework overlooked across most contours of the degrowth debate.

Later, I will provide an overview of the chief arguments made by the monopoly (finance) capital school,Footnote 2 and I will illustrate how they contribute to the debate on degrowth. Importantly, monopoly capital theorists describe secular stagnation as a historic, long-run tendency that plagues advanced capitalist economies. This perspective stresses the “maturation” of late capitalist economies, whereby massive productive capacity meets declining outlets for new investment and a growing class of indebted consumers who have trouble affording essential goods and services without exacerbating their debt (Warren 2007; Bellofiore and Halevi 2010; Foster and McChesney 2012a, b; Kalecki 1939). Keynes also remarked on this historical trouble, noting that a “euthanasia of the rentier” along with increasing “socialization of investment” was required to overcome what he called the “propensity to hoard” (Keynes 1937 quoted in Foster and McChesney 2012a, b, 58). For ecological economists and environmental political economy scholars more broadly, this characterization suggests that, in the monopoly capital stage, our economy does not contain adequate growth imperatives within its own operating logic. Rather, external stimuli such as government spending, advertising, financialization, military engagements, and war are required to support growth (Sweezy 1991).

To contextualize these trends, I provide a case study of monopoly finance capital. This study is necessarily interdisciplinary, drawing upon literature, perspectives, and data relevant to political economy, environmental economics, sociology, history, and social theory grounded in material conditions. The focus here will be the United States economy and its growing reliance on the real estate sub-sector to sustain capital accumulation in an era of secular stagnation. The U.S. is an important case in many respects, as it is the world’s superpower, the economic hub of finance capital, and a leading contributor to global ecological crises. This case will begin with an overview of the U.S. economy, which will illustrate the historical, long-standing nature of secular stagnation, and the trend toward dependency on the financial, insurance, and real estate (FIRE) sectors.

As elaborated upon in the discussion section, a monopoly capital analysis strengthens degrowth arguments. In sum, processes associated with monopoly finance capital enable increased, unsustainable consumption in the Global North despite anemic growth rates. As well, monopoly finance capital’s dependency on speculative real estate investment requires irrational allocation of energy and essential materials, particularly in the housing sector. Additionally, while monopoly finance capital enables increased consumption, it does so in a way that exacerbates inequality and fosters debt dependency. Citing recessions and periods of slow growth, critics assert that degrowth will require harsh austerity for the working class in the Global North (Phillips 2015; Phillips 2019; Huber 2021; Aukema 2023). However, from the lens of monopoly finance capital, secular stagnation is not a blip or a cycle but a systemic disease that financialization attempts to address in order to maintain growth in material throughputs while expropriating more and more wealth from the working class (Foster and Magdoff 2008). Thus, rising rates of housing precarity, debt, and other markers of economic destabilization across the Global North working class are not simply the result of a failure to grow but instead symptomatic of what monopoly capital theorists have long identified as a systemic ineptitude of late-stage capitalist societies to rationally utilize the economic surplus in such a way that meets genuine human need (Baran and Sweezy 1966; Saito 2023).

These dynamics constitute a stagnation-accumulation treadmill, where slow growth and accumulation are dialectically bound together to maintain material flows and accumulate capital in an era with diminishing opportunities for robust growth. This treadmill both entails and enables a paradoxical increase of consumption alongside increased social immiseration for a growing number of those in the Global North, particularly those who lack ownership of appreciating assets. In accordance with a great deal of recent degrowth scholarship, I will conclude with an argument that advocates for rational planning that promotes use-values, prioritizes human need, and eliminates (or de-grows) sectors that only exist to secure exchange value.

Debates on degrowth and growth imperatives

From a degrowth lens, ongoing growth constitutes a core imperative of capitalist development. For example, Hickel defines capitalism as a social-economic system “organized around the imperative of constant expansion, or growth,” that requires “ever-increasing levels of industrial extraction, production, and consumption, which we have come to measure in terms of Gross Domestic Product,” (Hickel 2020: 20). Frequently, degrowth scholars posit that such growth-oriented development is the ultimate purpose of capital accumulation, “as the surplus is accumulated and invested to produce more growth,” (Kallis 2017: 20). Often described as the core imperative of our economy, scholars refer to growth as the key architectural feature of modern capitalist economies and even modernity, generally (Jackson 2016). Put differently, “the global economy is structured around growth,” as Hickel et al. (2022) argue in a widely shared Nature article. Often, growth is synonymous with productivity; thus, modern capitalism is characterized as a hyper-productive, capacity-maximizing behemoth prone to ceaseless technological improvements and competitive behavior (Schmelzer et al. 2022; Alexander and Gleeson 2018; Smith 2010).

The material relationship between economic growth and environmental impact is well-established. Meta-analyses, large-scale literature reviews, and generalizable, large-N studies provide substantial evidence on the ongoing linkages (ranging from absolute to relative) between economic growth and various environmental impacts, carbon emissions, and material footprints (Haberl et al. 2020; Jorgenson and Clark 2012; Hubacek et al. 2021; Schandl et al. 2018). The positive relationship between GDP and material footprint load is especially strong, with little to no evidence to support decoupled development over time (Wiedmann et al. 2015; Sahoo et al. 2021).

Ecological economists debate the precise location of the growth imperative within a capitalist political economy—e.g., a debt-based monetary system or within the context of a political arena whose stability requires growth to avoid catastrophe (Cahen-Fourot and Lavoie 2016; Arnsperger et al. 2021; Stratford 2020). Those engaged in this arena of debate generally conceptualize growth-ism (or the ceaseless pursuit of growth) as ecologically unsustainable. Yet, some critics of degrowth stress that growth remains a positive, progressive feature of capitalist society. Degrowth critics reason that growth breeds innovation and harnesses the forces of development, which we need in order to rebalance global ecologies and lift billions out of deprivation. Notably, Chomsky and Pollin 2020; Chomsky 2022) spoke to this point, stating that, “all kinds of growth are required,” such as clean energy and public transportation infrastructure. Others reason that degrowth arguments work against the potential liberatory, labor-saving power of industrialization (Bastani 2019; Huber 2017; Phillips 2015). These theorists generally argue that a central, democratically accountable state could steer growth toward cleaner production techniques. Phillips (2019) gives the example of ozone recovery, which occurred as international organizations and nation-states issued regulations for CFCs in refrigerators and other household products.

Stressing historical materialism and the liberatory aspects of capitalist advancement, Huber also (2022b) defends growth as an effort to harness the liberatory powers of advanced, modern productive forces. This conception pairs well with Bastani’s (2019) argument that present-day capitalism contains the seeds for his conception of a futuristic, eco-utopia. Following Marx’s views of technological innovation and capitalism’s tendency to revolutionize the instruments of production, Bastani (2019) reasons that innovation in the productive forces will create new opportunities (such as off-world space-mining and nuclear fusion) for sustainable utopia—or what he calls fully automated luxury communism.

Bastani’s (2019) vision aligns well with environmentally minded calls for socialist modernism or the notion that we can harness capitalism’s innovative, revolutionary, and historically progressive tendencies for the good of humanity and the planet (Huber 2021). Without growth, Phillips (2015) reasons there is no incentive to invest surplus towards environment-saving innovations. “Thus we either invent nothing new…or we have to grow.” The challenge is, to Phillips (2015, 62), to “take over the [growth] machine, not turn it off!” Phillips’ argument thus suggests that the “machine” is a productive and innovative one, whose tendencies to innovate towards more efficient technologies can be rationally harnessed by socialist state planning (Phillips 2023). Jettisoning degrowth in favor of productivism, socialist modernism also argues in favor of industrial food technologies, atmospheric geoengineering, nuclear energy, and centralized state planning (Nordhaus and Smith 2021; Rosenberg and Wilson 2021; See Jacobin Magazine 2017 special issue on climate change as well as Angus 2017 for a response).

The hyper-focus on “growth” across these debates can easily lead to misconceptions about the current trends of advanced capitalist economies and the challenges to sustainability that they pose. Modernist critics of degrowth appear to overlook current trends (described below) that point to the reality that capitalism, as it faces more limits to growth, has stagnated as a socio-historic force for progress. On the other hand, identifying growth as the central feature of capitalism possesses its own risks. For instance, the tendency toward secular stagnation in late capitalist societies can be confused as evidence to suggest that we are indeed already moving toward a more rational “degrowing” economy. In a hopeful fashion, Odum and Odum (2011) argued that such trends pointed toward a “prosperous way down,” or socioecological, rational downsizing, which they believed would occur as capital began to confront barriers to low-cost materials that enabled robust growth. Rather than a smooth transition to a prosperous way down, or a modernist vision of no-limits, “fully automated luxury communism,” capital appears capable of ongoing reproduction in a context of secular stagnation. Thus, there exists a need for additional critical theorizing of how capital is reproduced in the context of patterned low growth. As I will argue, what affluent and late-stage capitalist economies currently encounter is not just a “growth imperative,” but a stagnation-accumulation treadmill where robust growth, which is no longer secured easily, is less and less central to the underlying requirement of capital accumulation. This argument builds off the insights provided by the monopoly capital school, which I detail in the subsequent section.

Growth and monopoly capital

Monopoly capital stresses that secular stagnation is a normal condition of advanced capitalist economies. Stagnation—or patterned low growth—is sometimes described as a new problem, observed at a general level since the late 1970’s, and one whose causes include “international competition, declining productivity growth, and the financialization of the global economy,” (Schmelzer et al. 2022, 71). The monopoly capital school instead argues that secular stagnation is a normal tendency of capitalist economies that have developed past an early competitive stage and toward a monopolistic structure governed by giant corporations. As such, there is nothing “natural” or endogenous to capitalism that secures a robust long-term rate of growth (Foster 1987). Hansen 1938, 549) identified this lack of an internal imperative as a propensity to save in an era where relatively obvious stimuli for investment (the frontier, a rapidly growing population, epoch-changing technological innovations) were closing or extinguished (Hansen 1955; Foster 1987).

Writing in the 1950s and 1960s, during the supposed golden age of capitalism, Baran and Sweezy argued that the rise of the “giant corporation” meant less room for “competitive entrepreneurs,” who “do the vital pioneering work,” of innovation and risk-taking (Baran and Sweezy 1966, 49). In such conditions, monopolistic firms have little competitive incentive to take risks or invest in arenas outside of advertising—though they will gladly incorporate cost-cutting measures (like automation or outsourcing) to accelerate surplus accumulation. Baran and Sweezy (1966) judged this as a tendency for the economic surplus to rise despite shrinking growth rates. Unutilized productive potential or “excess capacity,” generated stagnation, or what they identified as the “normal state of the United States economy,” (Baran and Sweezy 1966, 76). Under such conditions, productive capacity can exceed effective demand by a widening margin, which “has the effect of shutting off potential net investment before it can actually be generated,” leading to a “vicious circle of stagnation” in mature capitalist economies (Foster 1987, 61; Kalecki 1939).

Baran, writing 10 years before he co-authored Monopoly Capital, argued that this “cancerous malaise of monopoly capital” led to a host of irrational consequences, including ever-increasing spending on advertising for shoddy and even harmful commodities or the tremendous amount of surplus invested in war and the military industrial complex (Baran 1957, xvii). A key argument that Baran and Sweezy articulated in Monopoly Capital concerned the ways in which the state and the capitalist class attempted to overcome the inherent tendency of slow growth that they identified as endemic to monopoly capital. “War spending,” first in World War II and later with the global Cold War, “accomplished what (New Deal Era) welfare spending had failed to accomplish,” as it—more than any other force—enabled the mirage-like era of capitalism’s golden age to blossom (Baran and Sweezy 1966, 160–161). Thus, monopoly capital theorists have long argued that political actors seek to overcome stagnation via various fiscal stimuli.

Yet every stimulus can only serve as a temporary fix to the deeper, structural problem of secular stagnation endemic to this historical period of monopoly capital. Thus, the outsourcing of competition to upstream, Global South suppliers (or the global labor arbitrage) and neoliberal market reforms are not causes of secular stagnation; rather, they are adaptations to this ever-present “cancerous malaise” identified by Baran almost 70 years ago, as of writing. Of course, these adaptations contain very real, material consequences that further skew power away from laborFootnote 3 and in favor of capital (Jackson 2019; Magdoff and Foster 2023). In Foster and McChesney’s (2012a, b) The Endless Crisis, they argue that the “underlying disease” of secular stagnation continues, but capital “has paradoxically even prospered within this impasse, through the explosive growth of finance” (Foster and McChesney 2012a, b).

The economy therefore functions below its potential with a tremendous amount of unused productive capacity, needless un(der)employment, and worsening wealth inequalities (Magdoff 2006). Of note here is the tendency of advanced capitalist economies towards a falling rate of manufacturing capacity utilization, which has declined consistently over a five-decade period in the United States (Foster and McChesney 2012a, b). Consequently, growth in highly financialized, stagnant economies like the U.S. increasingly depends on the wealth effect, or luxury consumption by the rich, and debt-based consumption from the rest of the population, whose historical consumption rates increased in spite of the fact that median wage compensation stagnated or fell steadily for middle class and lower class earners (respectively) over multiple decades (Brenner 2003; Foster and McChesney 2012a, b; Mishel et al. 2015; Magdoff and Foster 2023). Increasingly, the flow of goods through the economy now depends on the financialization of housing, as mortgage lending comprises the largest activity for most banks in advanced economies (Ryan-Collins et al. 2017). Middle-class consumers may also take out loans against their house, say to buy a vehicle, but such activity cannot “solve” secular stagnation and likely exacerbates its crisis tendencies (Ryan-Collins et al. 2017). These efforts allow advanced capitalist economies to churn through materials and secure valorization for capital, despite declines in the material bases that more effectively support both the “real economy” and a relatively stable working class.

In sum, monopoly capital theorists stress that advanced capitalist economies are inherently prone to stagnation. Without sufficient oppositional force from government or organized labor, capital appears content to prioritize shorter-term, asset-driven booms over productive investments. The pressure to maintain a somewhat stable economic system that can distribute wealth through the population is thus a matter of politics. Indeed, growth is still required to prevent bubble-driven crises, mitigate Piketty’s r > g problem that capital return outpaces economic growth, create jobs, and stave off the disastrous consequences of recession (Stratford 2020). However, under monopoly capital, there exists insufficient internal logic or mechanisms necessary to avoid such consequences—Après moi, le deluge,Footnote 4 as Marx remarked in Capital. Today, risk is curtailed not by robust growth but rather by central banking institutions, notably the U.S. Federal Reserve, which can prop up insecure creditors both at home and abroad (Tooze 2018). Stagnation therefore breeds speculation, which generates more stagnation and creates conditions for an “endless crisis,” whereby an ever-increasing amount of financialization is required to keep the economy afloat.

The conditions and effects of monopoly capital are evident in the United States. The following section analyzes trends in secular stagnation and the growth of the FIRE sector within the United States. This case will provide a descriptive analysis of conditions associated with monopoly capital. Then, the subsequent section will parse out the implications of these trends as they relate to social inequality and environmental impacts. The data presented illustrates descriptive trends that earlier studies of monopoly finance capital emphasize as evidence of stagnation and financialization in an affluent economy (Foster and McChesney 2012a, b). When relevant, I also provide visualizations to illustrate important patterns in U.S. housing, material footprints, and built land footprints. Data presented in subsequent sections were gathered from the World Bank, Saint Louis Fed, Bureau of Economic Analysis, the U.S. Census, the Global Footprint Network, and the Global Material Flows Database. Data collection occurred during the research process for this analysis, which primarily took place in the fall of 2022. Because the case relies on descriptive data, it is largely an exploratory study. Comments on how to advance this case and the theory built by it appear in the conclusion.

Secular stagnation and FIRE in the United States

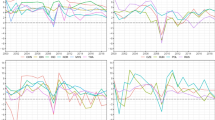

In the United States, annual GDP growth rates (measured as a percent increase from the previous year) have trended downward since 1960—the first year available as tracked by the World Bank. Figure 1 illustrates this trend. As alluded to, this decline implies that secular stagnation predates its usual periodization.

Annual GDP growth rate (% growth from previous year), United States

Figure 2 suggests that not only is new growth in decline, but the productive potential of the U.S. economy is as well. According to Fig. 2, the U.S. industry appears less and less confident that productivity growth will lead to the kinds of profits that justify investment. This trend has only continued during the notably unimpressive, post-Great Recession recovery. As Foster and McChesney (2012b) point out, net private nonresidential fixed investment dropped every decade between the 1970s and 2010s—a trend that continued after the Great Recession (Fig. 3). Confronted with limited demand and a dearth of investment opportunities in productive arenas, the U.S. economy has become increasingly dependent on finance capital to keep accumulation afloat during prolonged periods of slow growth (Foster and Magdoff 2008). Hence, U.S. productive sectors are reaching all-time lows in capacity utilization. This trend suggests an ominous rise in inefficiency and underdevelopment. Put differently, U.S. capital lacks the incentive to fully realize its productive potential—a trend that has been worsening over time. The failure to fully realize already existing capacity generates disinterest in new industrial investments, as indicated by Fig. 3.

US capacity utilization, annual rate

Real private fixed investment in manufacturing % growth rate

Indeed, the FIRE sector sustains the U.S.’ increasingly unimpressive growth rates. Figure 4 illustrates how, in a decade of recovery since the Great Recession, FIRE’s share of annual U.S. growth has increased, as the relevance of manufacturing for U.S. growth continues its historic decline.

Value added by industry, percent GDP

Recent estimates (Fig. 5) demonstrate that real estate’s quarterly contributions to the U.S. GDP total more than $2700 billion—a number that has increased annually over the course of the pandemic and outweighs the contributions of all other FIRE subsectors combined.

FIRE sector disaggreated, contributions to GDP (billions of dollars)

U.S. economic growth is therefore increasingly dependent upon real estate-oriented development. From the lens of the degrowth debate, the next section details some of the irrational socioecological consequences of this trend.

The real estate economy

While real estate development can generate growth in manufacturing via construction demand, a problem stems from land’s tendency to appreciate its value without investment (Ryan-Collins et al. 2017). Banks see real estate as a source of cheap funding and excellent returns, meaning that credit is less tied to the so-called real economy and more prone to asset price booms (Tooze 2018). This form of growth produces historically specific, irrational socioecological consequences, chiefly, housing insecurity, acceleration of uneven wealth, and capital accumulation as well as wasteful allocation of material resources that correspond with debt-based, ecologically intensive consumption.

Housing insecurity

To remark that the real estate sector is “doing well” belies the reality that affordable, decent housing is increasingly difficult for working-class people in the United States to secure. According to a recent real estate consulting report, it now costs $839 more per month to own a home than it does to rent one in the United States (Nguyen 2022). As such, homeownership rates are projected to decline in the coming decades, with especially significant declines for marginalized groups (Goodman and Zhu 2021). However, the real estate sector regards unaffordable housing as an opportunity for further investment and accumulation. As the report (ibid) states:

“With demand now shifting toward renting, home builders who were once reluctant to sell to rental home investors are now soliciting offers from investors. Strong demand from investors will provide additional support to today’s home prices.”

Figure 6 illustrates how the rising precarity of U.S. tenants further buoys these enticing trends for real estate capital. In 2021, rental vacancy rates fell to their lowest point in over three decades in the United States.

Rental vacancy rates US

Thus, vacant rental units get snatched up quickly. This dynamic cedes further political economic power to an emergent class of land and property owners who can confidently charge higher rents in extremely competitive markets. Relatedly, tenant eviction across major U.S. cities is now commonplace. As Desmond (2016) documents, roughly one in eight tenants in major U.S. cities suffer eviction. The service of eviction—once a taboo and rare practice just generations ago—is now a routine procedure for U.S. police and landlords (Desmond 2016). Princeton’s Eviction Lab documents nearly 1.1 million home evictions across 34 U.S. cities over a 12-month period, with nearly 70,000 evictions occurring just last month, in those cities, as of writing (Eviction Lab 2022). In total, these dynamics are common across housing markets in the United States, including in cities with relatively lower rent costs and surplus availabilities of rental units (Schwartz and McClure 2021). Suggesting the commonplace reality of this crisis, many of the nation’s “top evicting cities,” are not stereotypical hubs of outlandish housing costs. The number one ranked “evicting city” is North Charleston, South Carolina, where 16.5% of all renter-homes are evicted each year (Eviction Lab 2022). In an absurd example of irrational allocation of resources, such trends correspond with net increases in the country’s total housing stock (Saint Louis Fed 2023a).

Wealth accumulation and inequality

The cost of renting a home in the United States is increasingly burdensome for working-class and poor individuals and families. Over the last several years in the U.S., income failed to keep up with the cost of rent, and now, close to 50% of all American renters spend over 30% of their monthly income on rent alone (Schaeffer 2022). On the other side of the market, the recent uptick in home buying in the United States is overwhelmingly fueled by the affluent. According to the Home Buyers and Sellers Generational Trends Report, the median household income for new home buyers was roughly $102,000—a mark that exceeds the national median by $35,000 per year (Trapasso 2022). New homebuyers are also overwhelmingly white, a social fact that will exacerbate the already staggering racial wealth disparities within the U.S. (Trapasso 2022). The evidence that such inequalities can be solved by a more libertarian housing policy is not compelling. As extensively documented by Taylor (2019), efforts to liberalize housing finance and increase homeownership for Black and brown people have been tremendously marred by racial capitalism, characterized by predatory lending and racist attitudes against Black and brown homeowners. Today, the hyper-competitive sellers’ market that currently exists favors the wealthy and puts Black and brown people at a further disadvantage as realtors rely upon arbitrary judgements of “trustworthiness” that are vulnerable to racial bias and prejudice (Korver 2022; Korver-GE 2021).

New housing construction also overwhelmingly benefits the wealthy, as additions to the overall housing stock have failed to ameliorate housing costs for most Americans (Harvard 2023). Many markets are also increasingly vulnerable to large-scale property investors, who see property as a capital investment rather than a place to live. The percentage of homes purchased by investors has skyrocketed over the last decade (Henderson 2022). “All told,” writes Amanda Mull, “nearly a third of American house sales last year went to people who had no intention of living in them,” (Mull 2022). A Wall Street Journal expose cited a real estate consultant on the matter, who plainly stated that because of these trends, “you now have permanent capital competing with a young couple trying to buy a house,” (Dezember 2021). While analysts have generally criticized the notion that large-scale investors like Blackrock are buying every home on the block, it is accurate to suggest that such companies are buying properties that working- to middle-class families might have a chance to obtain in many key markets (Botella 2021). Moreover, in a country rife with homelessness and housing insecurity, luxurious units often remain unoccupied for years. In New York, one out of four luxury housing units constructed over the last decade remained vacant for prolonged periods of time, sometimes years (Chen 2019). Of these units that had been sold, 40% were purchased by investors with no intention of living in them (Chen 2019). Housing insecurity also benefits landlords and owners who can generate higher rates of returns off expensive rents in poor neighborhoods with low property taxes, low maintenance costs, and (in the case of mobile homes) sell the land out from under the resident (Desmond and Wilmers 2019; Sullivan 2018).

Beyond single-family housing, commercial property—warehouses, hotels, multi-family properties, retail, offices, etc.—comprises a massive portion of the sector. Commercial property companies control billions of square feet of space and constantly seek to expand in scale. As the Wall Street Journal documents:

“Prologis, the world’s largest owner of warehouse space, said Monday it is acquiring Duke Realty Corp., in a $26 billion deal that will add 160 million square feet of industrial capacity to Prologis’s world-wide portfolio of 1 billion square feet.” (Young 2022).

Over $600 billion is currently invested in the U.S. commercial real estate market, with “equity capital targeting U.S. real estate near all-time highs,” buoyed by a “robust investor appetite,” that real estate capitalists believe will keep prices trending upward (Coldwell Banker Richard Ellis (CBRE), 2021). A great deal of enthusiasm in this sector also exists for the construction of massive warehouses for the storage and mining of cryptocurrency, blockchain, and digital tokenization (Newmark 2022).

The ecology of built property and real estate speculation

One might reasonably wonder—what is the net ecological footprint of vacant apartments, empty warehouses, perpetually flipped homes, bitcoin mining centers, a halfway empty commercial office space, or a new luxury hotel averaging an industry-standard 50% occupancy rate? Or, what might be the footprint of the built space within these properties that is strictly unused, going to waste, and really only in existence to drive up investors’ portfolios? The precise numbers here are difficult to discern, but the reality that one might even have to ask such questions points to the ecological irrationality of monopoly finance capital. Currently, a substantial portion of the U.S. carbon budget and material footprint goes to waste in order to fuel the real estate market upon which U.S. GDP growth depends.

Presently, the rise of monopoly finance capital’s real estate economy contains both direct and hidden environmental impacts. In terms of direct impacts, emissions from the building sector make up 14% of all U.S. greenhouse gas emissions—a number that increased 8% since 2005 (Chong 2022). Emissions from the building sector can include embodied and operational carbon—at most points in a building’s life cycle, emissions stem from embodied carbon, i.e., the emissions involved in the production, manufacturing, construction, repair, and disposal of building materials like concrete and glass (CLF 2020). When including embodied and operational carbon—offsite electricity, for example—the building sector accounts for 30% of all U.S. greenhouse gas emissions (Center for Climate and Energy Solutions 2018). A heavy portion of embodied building emissions include concrete production which, as Huber (2022a, b) points out, constitutes a large portion of manufacturing sector emissions as well. If “business as usual” approaches to development continue, the building sector projects to emit 62 gigatons of CO2 from roughly now until mid-century (Logan 2021). When thinking of climate change, it is common to imagine a dirty smokestack or clear-cut forest. We should add speculative real estate development, especially that which does nothing (or worse) to address social problems like housing affordability, to this imagination.

More broadly, as Alexander and Gleeson (2018) argue in their work Degrowth in the Suburbs, capital has favored an irrational form of human settlement that requires privatization of mass tracts of land and extremely wasteful consumption of resources (e.g., fuel for driving longer distances, inefficient energy for heating/cooling) that more rational urban planning could easily avoid. Globally, waste from construction projects constitutes upwards of 30% of all landfill waste worldwide and 40% of total energy and resource consumption (Tafesse et al. 2022; Polat et al. 2017; Asif and Muneer 2007). In the U.S., over the last five decades, the size of houses increased by 21%, occupants decreased by 14%, and the amount of developed land increased by 61% (University of Michigan Center for Sustainable Systems 2023). The term “sprawl” thus comes easily to mind when imagining the developmental pattern of U.S. urban planning. As tracked by the Ecological Footprint Network, the footprint of built land in the United States has increased consistently over the last 50 years as well (Fig. 7). In simple terms, the built-up land footprint represents the amount of land covered by human infrastructure (Global Footprint Network 2024). In addition to the effects discussed above, such increases exacerbate pressure on watershed sustainability and biodiversity. As discussed, these increased ecological impacts correspond with continued and exacerbated trends related to inequality and housing precarity.

US-built land footprint, thousands of global hectares

In terms of hidden or indirect effects, it is critical to understand the rise of real estate and the FIRE sector as essential for the continued, increasing flow of matter and energy through the world economy. As widely noted, material footprints are strongly correlated with GDP growth across affluent, OECD economies (Hickel 2021a). This correlation holds in the United States as well, with the most substantial declines in material footprint indicators occurring after the housing crisis that fueled the Great Recession (Fig. 8). In a context where the “real economy” appears less capable of stimulating GDP growth, the rise of the FIRE sector under monopoly capital, therefore, enables the circulation of money, credit, and, ultimately, material. Indeed, the maintenance of consumption in the U.S. appears increasingly dependent on “wealth effect” consumption, whereby households borrow against their home or consume more as the value of their assets rise to enable and expand present levels of consumption—especially when faced with credit difficulties (Cooper and Dynan 2016; Brenner 2003).

GDP vs material footprints, United States

It is essential to place this sort of wealth-effect consumption in a broader context. As a core nation within the structurally unequal capitalist world system, the U.S.’ middle and upper classes serve as a consumer base for ecologically intensive, heavily exploited labor abroad (Jorgenson 2016; Dorninger et al. 2021; Givens et al. 2019; Hornborg 2009; Smith 2016; Suwandi 2019b, a; Hickel et al. 2022). The dependence on the FIRE sector to maintain consumption in countries like the U.S. thus creates a kind of Faustian bargain whereby the valorization of globalized capitalist production requires the acceleration of financialization, which is needed to maintain demand in affluent, high-consuming nations. These dynamics harken to what Foster and Suwandi (2020) refer to as “catastrophe capitalism,” whereby capital accumulation requires highly unsustainable, increasingly interlinked circuits of exploitation, ecological plunder, and financialization across multiple levels of the world system.

Discussion: monopoly capital and the stagnation-accumulation treadmill

Stagnant growth and financialization are dialectically intertwined. This intertwinement can be described as a stagnation-accumulation treadmill in late capitalist economies. The stagnation-accumulation treadmill stems from ongoing slow growth combined with rapid capital accumulation, both of which condition and mutually reciprocate one another. As monopoly capital theorists have long argued, modern financialization is a consequence of monopoly capital’s failure to secure adequate investment outlets needed for robust growth in productive areas. However, as Foster and McChesney’s (2012a, b) phrase “endless crisis” suggests, financialization only exacerbates problems of over-accumulation because it fails to stimulate robust growth. Financialization fuels credit booms and wealth-effect consumption, which serve as life-support for stagnant levels of GDP growth. This anemic growth serves to maintain a precarious bubble economy for as long as it can. Akin to a political growth imperative, policymakers at all levels will therefore pursue growth-oriented policies, even with diminishing returns, to keep the treadmill going (Stratford 2020). For finance, the politics of growth also emerge in the form of a “de-risking state,” whose role is to minimize barriers to accumulation through regulatory reform and guarantee financial returns through direct grants, preferential credit, loan guarantees, and a slew of other instruments (Gabor 2021). When crisis does occur, threats of prolonged recession quickly lead to bailouts followed by ongoing “quantitative easing” that props up a “too big to fail” financial system where an increasingly small number of gigantic, international finance firms hold undue weight over the stability of the global system (Tooze 2018).

To extend upon monopoly capital arguments, these conditions emerge precisely because growth-ism cannot serve as a long-run, historically progressive force. Without rational planning to assess and cater to human needs, a system predicated on limitless expansion will, invariably, run into objective limits associated with reduced demand and stressed ecological systems. In other words, aggregate demand and ecological fecundity are not infinite and cannot be expected to increase at paces required to fuel robust growth ad infinitum. Thus, paradoxically, the rise of the “non-real” FIRE sectors underscores the materiality of the global economy. Financialization may appear ethereal and limitless, but its emergence as a defining feature of our times provides further evidence that there are indeed limits to growth. This reality poses a challenge to socialist modernist theorists, who still maintain that a system whose stability requires limitless growth can be effectively managed in a sustainable fashion. This sentiment is reinforced by long-standing theories of economic and environmental “de-coupling,” where affluent economies supposedly move towards cleaner forms of development decoupled from environmentally intensive industrialization (Mol and Spaargaren 2000; Mol 2002; Buttel 2000). This logic is still prominent today, especially in relation to carbon emissions, the impact of growth in rich nations, or the continued allure of green capitalism (Rathi 2024; Wang and Su 2020; Krugman 2023).

However, the stagnation-accumulation treadmill points to the reality that financialization does not produce a dematerialized or decoupling economy. Likely enabled by debt-based, wealth-effect consumption, as well as luxury consumption by the very affluent, the United States’ material footprint consumption and built-land footprints continue to rise despite low growth. From a world-system level, the growing dominance of finance capital also corresponds with the closing of colonial markets on tap that once served as captive consumer bases and new sources of labor exploitation and ecological expropriation (Patnaik and Patnaik 2021). Thus, through the lens of the stagnation-accumulation treadmill, financialization maintains the expropriation of ecological wealth from the Global South despite anemic growth rates in the North. These circumstances allow for a short-sighted, crisis-oriented prolongation, where Global North consumption and unequal ecological exchange can increase despite austere conditions for much of the Global North working class.

Thus, finance allows for the acceleration of the “ecological rift” between society and non-human ecologies (Foster 2011). Under capitalism, the metabolic requirements of non-human ecologies (e.g., nutrient cycle, species reproduction, the carbon cycle) become subjected to the social demands of a capitalist mode of production. Under the “social metabolic order” of capital, it is argued that the cyclical, regenerative requirements of finite non-human natures are subjected to the uncontrolled and limitless logic of exchange value and capital accumulation (Foster 2023; Foster 2023; Longo et al. 2015). This means that human and nature interactions must intensify, with larger quantities of non-human nature (e.g., raw materials) extracted from nature across local, regional, and global scales to satisfy ongoing capital accumulation (Foster 2023). Because it can maintain the flow of credit and consumption, FIRE enables these intensified interactions to continue despite barriers to the robust growth of the “real economy.” However, due to the nature of financialization under capitalism, this intensification of extraction and consumption occurs in a context whereby much of the Global North working class is vulnerable to increased socioeconomic precarity. In Burkett’s (2005) terms, such trends indicate that capital continues to favor the “growth of material wealth in a general sense” over “Marx’s vision of free and well-rounded human development,” (Burkett 2005: 18).

Mistaking the logic of monopoly finance capital for “degrowth,” critics have argued that degrowth downplays the material realities—such as food or energy insecurity—of the Global North working class, promotes austerity, and ignores the primacy of capital accumulation (Phillips 2015; Huber 2022a, b; Aukema 2023). Aukema (2023) goes so far as to argue that capital embraces degrowth as a method for dealing with excess accumulation, essentially arguing that degrowth is synonymous with austerity and, thus, already occurring. To say that capital embraces degrowth, though, disregards the decades of extraordinary measures that capital has taken to reproduce itself against the objective limits associated with stagnating demand, a shrinking “resource base,” and a closing “global frontier.” Thus, I argue that the rise of FIRE coupled with austerity measures arises precisely because of a structural resistance against a more rationally planned economy that operates within limits. In addition to the inequities and social problems discussed in the preceding section, the rise of the FIRE sector has captured local politics and fueled environmental injustices associated with gentrification (Stein 2019; Ariza 2020).

These injustices and socioecological irrationalities do not represent a “degrowth” vision for two major, conceptual reasons. One, the stagnation-accumulation treadmill allows for an expansion of material throughput despite anemic GDP growth in the capitalist core. Capital’s rejection of a “degrowth vision” is obvious in the reality that the United Nations expects that raw material extraction will increase by 60% between now and 2060, globally, largely to satisfy rising demand from Global North nations (Nelsen 2024). Two, the transition to the FIRE sector occurs because it maintains, to use Harvey’s phrase, “value in motion,” a process akin to a cycle that resembles a “constantly expanding spiral,” (Harvey 2007; Clarno 2019: 370). Taken together, these reasons suggest that the rise of FIRE, and more broadly, the expansion of credit, serve as fraught mechanisms to increase the flow of material throughput and, thus, accelerate the accumulation of capital despite the underlying obstacles to economic growth.

Conclusion: the value of degrowth alternatives

Halting the stagnation-accumulation treadmill will require planned degrowth that promotes rational utilization of economic surplus alongside dis-accumulation and redistribution of wealth. This approach differs from Klitgaard’s (2023) definition of a recession, which he calls “unplanned degrowth.” Planned degrowth would instead involve the intentional shrinking of damaging sectors, such as speculative, unaffordable, and low-quality housing developments, and towards needed infrastructure such as sustainable, de-commodified housing and retrofitting abandoned, unused structures to increase affordable housing stock. This approach mirrors what Foster (2023), drawing from Odum and Odum (2011), refers to as a prosperous way down. On the one hand, a prosperous way down implies that, when done with intention, degrowth can result in improved living conditions for the world majority—including most people in global North nations. On the other hand, a “prosperous way down” also points to the necessity for greater economic planning that aligns production with the human need to eliminate wasteful usage of materials that exacerbate inequities—e.g., construction of luxury condos that will remain largely unfilled in a city with rising homelessness (Foster 2023).

Theoretically, degrowth requires that we organize production in a cooperative, planned fashion to meet human needs. This will involve what Marx called “real anticipation…in relation to the work and to the land” to avoid the “premature over-exertion and exhaustion” of both (Marx 1971, 309; quoted in Foster 2023). This approach challenges conceptions of wealth endemic to a capitalist mode of production, which generally emphasizes an abundance of commodities and an ever-increasing flow of matter and energy through the economy. Under such conditions, human need is perceived as insatiable with no discernible limits; in other words, “human need” becomes a reification of the capitalist growth imperative (Saito 2023). In the U.S., especially, this reification corresponds to increasing levels of personal consumption that occur alongside rising indebtedness, continued poverty, worsening health outcomes, shorter vacations, and more time at work (Schor 2010). Thus, calls for degrowth now center on the importance of increasing public wealth in the form of job guarantees, the decommodification of public goods/services, investments in green technologies, as well as an optimistic vision of what constitutes the “good life” (Odum and Odum 2011; Soper 2020; Hickel 2023).

Realizing such goals will require challenging the interests of monopoly finance capital. Challenges can range from radical to reform-based, especially if reforms create opportunities for greater transformation in the future. Programs that institute communal, public ownership of land, where property is a public good as well as tax reform—such as a land value tax—are worth exploring and advocating for whenever possible. As well, financial reforms that limit the capacity of finance capital to create and use credit are necessary (Ryan-Collins et al. 2017). These calls to reform and re-imagine land relations could pair well with more radical calls to reimagine property relations entirely and to restore land rights and sovereignty to Indigenous groups and victims of contemporary land-grabbing (Estes 2019; Ajl 2021). Moreover, the very system of private sector finance, where investment is mostly if not strictly determined by the potential for returns, must be radically challenged. Stein (2019) also offers a review of policies, principles, and political actions currently undertaken, or being advocated for, that could sway power away from finance capital. These include more public funding for government-sponsored housing, stronger taxes on landlords, regulations, and limits on rent increases, democratically controlled city planning, as well as mass rent strikes and eviction blockades that emanate from organized tenant-rights movements and unions. Overall, connecting degrowth to struggles against financial profiteering could prove politically appealing, as fewer and fewer people materially benefit from the turmoil and inequality associated with such processes.

Achieving these aims will require transcending the logic of capital, a system that Mészáros (1995) referred to as an “uncontrollable mode of social metabolic control.” As Mészáros reasoned, capital alienates individuals from control over the production process. Thus, at a broad level, society appears to have little command over what gets produced, how, where, why, and by whom. Rather, the determinations accord to capital’s “immanent necessities” of growth and expansion and thus appear “radically incompatible” with comprehensive social planning (Mészáros 1995, 881 & 886). As Mau (2023) has similarly argued, capital’s “mute compulsion” bleeds into daily life and social reproduction, making it difficult to determine which parts of our lives are truly “free” from the demands of capital accumulation. Here, the value of planned degrowth becomes clear, as it simultaneously challenges the logic of capital accumulation while also advocating for a reassertion of non-alienated control over economic life.

Directions for additional research

Future scholarly work in degrowth should investigate the extent to which the stagnation-accumulation treadmill—as indicated by low rates of economic growth and increasing rates of financialization, speculation, and accumulation from the FIRE sector—affects material footprint loads, progress on carbon and growth decoupling, and asymmetrical material flows across the global economy. Further, qualitative and historical work should continue to consider the obstacles posed by the FIRE sector to environmental justice and sustainable municipal development. At a more theoretical or abstract level, scholars interested in degrowth and environmental political economy, generally, should emphasize capitalism as a quest to secure the circulation of more commodities and, more abstractly, more material. Even in finance, where money appears to beget money, such immaterial processes are linked to material processes elsewhere.

These are just some implications relevant to monopoly finance capital, degrowth, and the stagnation-accumulation treadmill. At this juncture, the fundamentals for economic growth in affluent nations like the United States are, clearly, far from robust. However, the failure to rationally degrow the economy speaks to capital’s adaptive capacity to accelerate accumulation and keep the growth-dependent economy on life support. Each of these pillars of monopoly capital—anemic growth and impressive accumulation—exist co-operatively. A transition to a sustainable society will require challenging both these facets of the stagnation-accumulation treadmill.

Data Availability

All data presented in this paper is secondary and publicly sourced. Links for data sources presented in the figures are provided below.

Figure 1https://databank.worldbank.org/source/world-development-indicators

Figure 2https://fred.stlouisfed.org/series/TCU

Figure 3https://fred.stlouisfed.org/series/C307RL1A225NBEA

Figures 4 and 5https://apps.bea.gov/iTable/?reqid=150&step=2&isuri=1&categories=gdpxind#eyJhcHBpZCI6MTUwLCJzdGVwcyI6WzEsMiwzXSwiZGF0YSI6W1siY2F0ZWdvcmllcyIsIkdkcHhJbmQiXSxbIlRhYmxlX0xpc3QiLCI1Il1dfQ = =

Figure 6https://www.census.gov/housing/hvs/current/index.html#:~:text=National%20vacancy%20rates%20in%20the,quarter%202023%20(6.3%20percent).

Figure 7https://data.footprintnetwork.org/?_ga=2.90435098.180953541.1708114858-900013220.1705694898#/analyzeTrends?type=EFCtot&cn=5001

Figure 8https://www.resourcepanel.org/global-material-flows-database

Notes

Scholars across the degrowth debate generally utilize a Marxian conception of ‘working class’ or ‘workers’ to mean those who lack direct access to the means of production and must therefore earn a wage or salary to survive. For the context of this paper especially, global North workers are particularly vulnerable if they lack ownership or stake in appreciating assets, such as land, housing, or stock options.

I use monopoly capital and monopoly finance capital somewhat interchangeably here, as later theorists built off the monopoly capital foundations to consider the finance sector more directly.

One example of neoliberalism’s political class character in the United States is the collapse of labor union membership, resulting from outsourcing of jobs to lower paying workers. This process essentially lowered capital’s unit labor cost and, with it, the bargaining power of global North labor. See Harvey (2005) as well as Smith (2016) and Suwandi (2019b, a).

Translates to “after me, the flood.” Marx used this phrase to underscore the short-sightedness of capital and its lack of an internal mechanism to self-regulate for benefit of the environment, workers, and avoid crisis “unless society forces it to do so.” (Marx 1977: 381).

References

Ajl, Max. 2021. A people’s green new deal. Pluto Books.

Alexander S, Gleeson B (2018) Degrowth in the suburbs: a radical urban imaginary. Springer

Angus, I. (2017) Memo to Jacobin: ecomodernism is not ecosocialism. https://mronline.org/2017/09/25/memo-to-jacobin-ecomodernism-is-not-ecosocialism/. Accessed 30 Apr 2024

Ariza MA (2020) Disposable city: Miami's future on the shores of climate catastrophe. Hachette UK

Arnsperger, C, Bendell J, and Slater M (2021) Monetary adaptation to planetary emergency: addressing the monetary growth imperative. Institute for Leadership and Sustainability (IFLAS) University of Cumbria. https://insight.cumbria.ac.uk/id/eprint/5993/1/Bendell_occasionalpaper8_revised.pdf. Accessed 30 Apr 2024

Asif M, Muneer T (2007) Energy supply, its demand and security issues for developed and emerging economies. Renew Sustain Energy Rev 11(7):1388–1413

Aukema, J (2023) Why capitalism loves degrowth. compact magazine. https://compactmag.com/article/why-capitalism-loves-degrowth. Accessed 30 Apr 2024

Baran PA, Sweezy P (1966) Monopoly capital. An essay on the American economic and social order. New York, Monthly Review Press

Baran PA 1957. Political economy of growth. NYU Press

Bastani, A. (2019) Fully automated luxury communism. Verso Books

Bellofiore R, Halevi J (2010) Magdoff-Sweezy, Minsky and the real subsumption of labour to finance. Minsky, crisis and development. Palgrave Macmillan, UK London, pp 77–89

Botella, E (2021) Investment firms aren’t buying all the houses. But they are buying the most important ones. Slate. https://slate.com/business/2021/06/blackrock-invitation-houses-investment-firms-real-estate.html. Accessed 30 Apr 2024

Brenner R (2003) The boom and the bubble: The US in the world economy. Verso Books

Burkett, P. 2005. Marx’s vision of sustainable human development. Monthly review 57(5). https://monthlyreview.org/2005/10/01/marxs-vision-of-sustainable-human-development. Accessed 30 Apr 2024

Buttel FH (2000) Ecological modernization as social theory. Geoforum 31(1):57–65. https://doi.org/10.1016/S0016-7185(99)00044-5

Cahen-Fourot L, Lavoie M (2016) Ecological monetary economics: a post-Keynesian critique. Ecol Econ 126:163–168. https://doi.org/10.1016/j.ecolecon.2016.03.007

Carbon Leadership Forum (CLF) (2020) What is embodied carbon and why does it matter? https://carbonleadershipforum.org/carbonchallenge/#:~:text=Up%20to%20two%2Dthirds%20of,carbon%20(see%20Figure%202)

Center for Climate and Energy Solutions (2018) Decarbonizing US buildings. https://www.c2es.org/wp-content/uploads/2018/06/innovation-buildings-background-brief-07-18.pdf

Chen, S. (2019) One in four of New York’s new luxury apartments is unsold. The New York Times. https://www.nytimes.com/2019/09/13/realestate/new-development-new-york.html. Accessed 30 Apr 2024

Chomsky, N Pollin R (2020) Climate crisis and the global green new deal: The political economy of saving the planet. Verso Books.

Chomsky, N (2022) Noam Chomsky’s green new deal. Interview with David Roberts, Vox. https://www.vox.com/energy-and-environment/21446383/noam-chomsky-robert-pollin-climate-change-book-green-new-deal. Accessed 30 Apr 2024

Chong, H. (2022) Closing the gap: priorities for the U.S. Department of Energy’s building RD&D portfolio. Information Technology and Innovation Foundation. https://www2.itif.org/2022-doe-building-rdd-portfolio.pdf. Accessed 30 Apr 2024

Clarno A (2019) The durability and dynamism of David Harvey. https://journals.sagepub.com/doi/abs/10.1177/0094306119853802?journalCode=csxa

Coldwell Banker Richard Ellis (CBRE) (2021) U.S. real estate market outlook 2022. https://www.cbre.com/insights/books/us-real-estate-market-outlook-2022. Accessed 30 Apr 2024

Cooper D, Dynan K (2016) Wealth effects and macroeconomic dynamics. J Econ Surv 1:34–55

Desmond M, Wilmers N (2019) Do the poor pay more for housing? Exploitation, profit, and risk in rental markets. Am J Sociol 124(4):1090–1124

Desmond, M (2016) Evicted: poverty and profit in the American city. Crown

Dezember, R (2021) If you sell a house these days, the buyer might be a pension fund. The Wall Street Journal. https://www.wsj.com/articles/if-you-sell-a-house-these-days-the-buyer-might-be-a-pension-fund-11617544801. Accessed 30 Apr 2024

Dorninger C, Hornborg A, Abson WHV, Schaffartzik A, Giljum S, Engler JO, Feller RL, Hubacek K, Wieland H (2021) Global patterns of ecologically unequal exchange: implications for sustainability in the 21st century. Ecol Econ 179:106824. https://doi.org/10.1016/j.ecolecon.2020.106824

Estes, Nick. 2019. Our history is the future: Standing Rock versus the Dakota Access Pipeline, and the long tradition of indigenous resistance. Verso Books

Eviction Lab (2022) (Retrieved). https://evictionlab.org/eviction-tracking/. Accessed 30 Apr 2024

Foster JB (1987) What is stagnation? In: The imperiled economy, book I macroeconomics from a left perspective. URPE, New York. https://johnbellamyfoster.org/wpcontent/uploads/2014/07/Foster_What-is-Stagnation.pdf

Foster JB (2011) Capitalism and degrowth: an impossibility theorem. Monthly review 62(8):26 (https://monthlyreview.org/2011/01/01/capitalism-and-degrowth-an-impossibility-theorem/#en3)

Foster JB, Magdoff F (2008) Financial Implosion and Stagnation. Monthly Review 60(7):1–29

Foster JB, Suwandi I (2020) COVID-19 and catastrophe capitalism. Monthly review 72(2):1–20 (https://monthlyreview.org/2020/06/01/covid-19-and-catastrophe-capitalism/)

Foster, JB, McChesney, RW (2012) The endless crisis: how monopoly-finance capital produces stagnation and upheaval from the USA to China. Monthly review press

Foster, JB, McChesney, RW (2012) The endless crisis. Monthly review. https://monthlyreview.org/2012/05/01/the-endless-crisis/

Foster, JB (2023). Planned degrowth: ecosocialism and sustainable human development. Monthly review 75(3). https://monthlyreview.org/2023/07/01/planned-degrowth/political economy. Organization & environment, 18(1), pp.7–18.

Gabor D (2021) The Wall Street consensus. Dev Chang 52(3):429–459. https://doi.org/10.1111/dech.12645

Givens JE, Huang X, Jorgenson AK (2019) Ecologically unequal exchange: a theory of global environmental injustice. Sociol Compass 13(5):e12693. https://doi.org/10.1111/soc4.12693

Global Footprint Network (2024) Glossary. https://www.footprintnetwork.org/resources/glossary/

Goodman L, Zhu J (2021) The future of headship and homeownership. Indiana University Bloomington and Urban Institute. https://www.urban.org/research/publication/future-headship-andhomeownership/view/full_report

Haberl H, Wiedenhofer D, Virág D, Kalt G, Plank B, Brockway P, Fishman T et al (2020) A systematic review of the evidence on decoupling of GDP, resource use and GHG emissions, part II: synthesizing the insights. Environ Res Lett 15(6):065003. https://doi.org/10.1088/1748-9326/ab842a

Hansen AH (1938) Full Recovery or Stagnation? New York: W. W. Norton. 1955. The stagnation thesis. In, Readings in fiscal policy, American economic association (ed.). pp. 540–557. Homewood, IL: Richard D. Irwin, Inc.

Harvard University (2023) The state of the nation's housing 2023. https://www.jchs.harvard.edu/sites/default/files/reports/files/Harvard_JCHS_The_State_of_the_Nations_Housing_2023.pdf

Harvey D (2007) A brief history of neoliberalism. Oxford University Press, USA

Henderson T (2022) Investors bought a quarter of homes sold last year, driving up rents. PEW Trusts. https://www.pewtrusts.org/en/research-and-analysis/blogs/stateline/2022/07/22/investors-bought-a-quarter-of-homes-sold-last-year-driving-up-rents. Accessed 30 Apr 2024

Hickel J (2020) Less is more: how degrowth will save the world. Random House

Hickel J (2021a) The anti-colonial politics of degrowth. Political geography 88. http://eprints.lse.ac.uk/110918/1/1_s2.0_S0962629821000640_main.pdf. Accessed 30 Apr 2024

Hickel J (2021b) What does degrowth mean? A Few Points of Clarification. Globalizations 18(7):1105–1111. https://doi.org/10.1080/14747731.2020.1812222

Hickel J, Kallis G, Jackson T, O’neill DW, Schor JB, Steinberger JK, Victor PA, Ürge-Vorsatz D (2022) Degrowth can work—here’s how science can help. Nature 12(7940):400–403. https://www.nature.com/articles/d41586-022-04412-x

Hickel J (2023) On technology and degrowth. Mon Rev 75(3):44–50

Hornborg A (2009) Zero-sum world: challenges in conceptualizing environmental load displacement and ecologically unequal exchange in the world-system. Int J Comp Sociol 50(3–4):237–262. https://doi.org/10.1177/0020715209105141

Hubacek K, Chen X, Feng K, Wiedmann T, Shan Y (2021) Evidence of decoupling consumption-based CO2 emissions from economic growth. Adv Appl Energy 4(19):100074. https://doi.org/10.1016/j.adapen.2021.100074

Huber MT (2017) Value, nature, and labor: a defense of Marx. Capital Nat Social 28(1):39–52

Huber MT (2021) The case for socialist modernism. Polit Geogr. https://doi.org/10.1016/j.polgeo.2021.102352

Huber MT (2022a) Climate change as class war: building socialism on a warming planet. Verso books

Huber M. (2022b) Mish-Mash Ecologism. New Left Review. https://newleftreview.org/sidecar/posts/mish-mash-ecologism. Accessed 30 Apr 2024

Jackson T (2016) Prosperity without growth: foundations for the economy of tomorrow. Routledge

Jackson T (2019) The post-growth challenge: secular stagnation, inequality and the limits to growth. Ecol Econ 156:236–246

Jacobin Magazine (2017) Earth, wind and fire. Issue 26. https://jacobin.com/issue/earth-wind-and-fire. Accessed 30 Apr 2024

Jorgenson AK (2016) The sociology of ecologically unequal exchange, foreign investment dependence and environmental load displacement: summary of the literature and implications for sustainability. J Polit Ecol 23(1):334–349. https://doi.org/10.3390/su8030227

Jorgenson AK, Clark B (2012) Are the economy and the environment decoupling? A comparative international study, 1960–2005. Am J Sociol 118(1):1–44. https://doi.org/10.1086/665990

Kalecki M (1939) Essays in the theory of economic fluctuations. Russell and Russell, New York

Kallis G (2011) In Defence of Degrowth. Ecol Econ 70(5):873–880

Kallis G, Kerschner C, Martinez-Alier J (2012) The Economics of Degrowth. Ecol Econ 84:172–180

Kallis G (2017) In defense of degrowth: Opinions and minifestos. Uneven Earth Press

Klitgaard KA (2023) Planning degrowth: the necessity, history, and challenges. Monthly Review 75(3):85. https://monthlyreview.org/2023/07/01/planning-degrowth-the-necessity-history-and-challenges/. Accessed 30 Apr 2024

Klitgaard KA, Krall L (2012) Ecological economics, degrowth, and institutional change. Ecol Econ 84:247–253

Korver GE (2022) Opinion: the 1936 manual that enshrined racism in America’s housing. https://www.cnn.com/2022/08/24/opinions/racism-in-home-appraisal-real-estate-korver-glenn/index.html. Accessed 30 Apr 2024

Korver-GE (2021) Race Brokers. Oxford University Press. https://doi.org/10.1093/oso/9780190063863.003.0001

Logan A (2021) Predicting building emissions across the US. MIT climate portal. https://climate.mit.edu/posts/predicting-building-emissions-across-us. Accessed 30 Apr 2024

Longo SB, Clausen R, Clark B. 2015. The tragedy of the commodity: oceans, fisheries, and aquaculture. Rutgers University Press

Magdoff F, Foster JB (2023) Grand theft capital: the increasing exploitation and robbery of the U.S. working class. Monthly review. https://monthlyreview.org/2023/05/01/grand-theft-capital-the-increasing-exploitation-and-robbery-of-the-u-s-working-class/. Accessed 30 Apr 2024

Magdoff F (2006) The explosion of debt. Monthly review. https://monthlyreview.org/2006/11/01/the-explosion-of-debt-and-speculation/. Accessed 30 Apr 2024

Mau, S. (2023) Mute compulsion: a Marxist theory of the economic power of capital. Verso books

Mészáros, I. (1995). Beyond capital: toward a theory of transition. NYU press

Mishel L, Gould E, Bivens J (2015) Wage stagnation in nine charts. Economic Policy Institute 6:2–13

Mol APJ (2002) Ecological modernization and the global economy. Glob Environ Polit 2(2):92–115

Mol APJ, Spaargaren G (2000) Ecological modernisation theory in debate: a review. Environ Polit 9(1):17–49

Mull A (2022) The HGTV-ification of America. The Atlantic. https://www.theatlantic.com/technology/archive/2022/08/hgtv-flipping-houses-cheap-redesign/671187/. Accessed 30 Apr 2024

Nelsen A (2024) Extraction of raw materials to rise by 60% by 2060, says UN report. The Guardian. https://www.theguardian.com/environment/2024/jan/31/raw-materialsextraction-2060-un-report

Newmark. 2022. The future of industrial real estate: trends for 2022 and beyond. https://www.nmrk.com/insights/thought-leadership/the-future-of-industrial-real-estate-trends-for-2022-and-beyond. Accessed 30 Apr 2024

Nguyen D (2022) The light: demand shifting from owning to renting. John Burns real estate consulting. https://www.realestateconsulting.com/demand-shifting-from-owning-to-renting/. Accessed 30 Apr 2024

Nordhaus T, Smith A. 2021. The problem with Alice Waters and the slow food movement. Jacobin magazine. https://jacobin.com/2021/12/organic-local-industrial-agriculture-farm-to-table. Accessed 30 Apr 2024

Odum HT, Odum E (2011) A prosperous way down : principles and policies. University Press of Colorado, Sebastopol

Patnaik U, Patnaik P (2021) Capital and imperialism: theory, history, and the present. Monthly review press

Phillips L (2015) Austerity ecology & the collapse-porn addicts: a defence of growth, progress, industry and stuff. Zero Books

Phillips L (2019) The degrowth delusion. Open democracy. https://www.opendemocracy.net/en/oureconomy/degrowth-delusion/. Accessed 30 Apr 2024

Phillips L (2023) Degrowth is not the answer to climate change. Jacobin. https://jacobin.com/2023/01/against-degrowth-eco-modernism-socialist-planning-green-economy

Piper K (2021) Can we save the planet by shrinking the economy? Vox. https://www.vox.com/future-perfect/22408556/save-planet-shrink-economy-degrowth

Polat G, Damci A, Turkoglu H, Gurgun AP (2017) Identification of root causes of construction and demolition (C&D) waste: The case of Turkey. Procedia Eng 196:948–955

Probst J (2019) Secular stagnation: it’s time to admit that Larry Summers was right about his global economic growth trap. The Conversation. https://theconversation.com/secular-stagnation-its-time-to-admit-that-larry-summers-was-right-about-this-global-economic-growth-trap112977#:~:text=Invoking%20a%20previously%20discredited%201930s,more%20investment%20and%20consumer%20spending. Accessed 30 Apr 2024

Rathi A (2024) Climate capitalism: winning the race to zero emissions and solving the crisis of our age. Greystone Books

Rosenberg N, Wilson BS (2021) Don’t trust the antitrust narrative on farms. Law and political economy project. https://lpeproject.org/blog/dont-trust-the-antitrust-narrative-on-farms/. Accessed 30 Apr 2024

Ryan-Collins J, Lloyd T, Macfarlane L (2017) Rethinking the economics of land and housing. Bloomsbury Publishing

Sahoo M, Saini S, Villanthenkodath MA (2021) Determinants of material footprint in BRICS countries: an empirical analysis. Environ Sci Pollut Res 28:37689–37704

Saito K (2023) Marx in the Anthropocene: towards the idea of degrowth communism. Cambridge University Press

Schaeffer K (2022) Key facts about housing and affordability in the U.S. Pew Research Center. https://www.pewresearch.org/fact-tank/2022/03/23/key-facts-about-housing-affordability-in-the-u-s/. Accessed 30 Apr 2024

Schandl H, Fischer-Kowalski M, West J, Giljum S, Dittrich M, Eisenmenger N, Geschke A et al (2018) Global material flows and resource productivity: forty years of evidence. J Ind Ecol 22(4):827–838. https://doi.org/10.1111/jiec.12626

Schmelzer M, Vetter A, Vansintjan A (2022) The future is degrowth: a guide to a world beyond capitalism. Verso Books

Schor JB (2010) Plentitude. Penguin Press, The new economics of true wealth

Schwartz A, McClure K (2021) Why building more homes won’t solve the affordable housing problem for people who need it most. Columbia Missourian. https://www.columbiamissourian.com/opinion/guest_commentaries/why-building-more-homes-wont-solve-the-affordable-housing-problem-for-people-who-need-it/article_7e240f80-463a-11ec-8e37-8f6255a00783.html. Accessed 30 Apr 2024

Smith R (2010) Beyond growth or beyond capitalism. Real-World Econ Rev 53(2):28–42

Smith J (2016) Imperialism in the twenty-first century: globalization, super-exploitation, and capitalism’s final crisis. NYU press

Soper K (2020) Post-growth living for an alternative Hedonism. Verso books

Stein, S (2019) Capital city: Gentrification and the real estate state. Verso Books

Stratford B (2020) The threat of rent extraction in a resource-constrained future. Ecol Econ 169:106524. https://doi.org/10.1016/j.ecolecon.2019.106524

Sullivan E (2018) Manufactured insecurity: mobile home parks and Americans’ tenuous right to place. University of California Press

Suwandi, I. (2019). Value chains: the new economic imperialism. Monthly review press

Suwandi I (2019) Value chains: the new economic imperialism. Monthly review press.

Sweezy PM (1991) Monopoly capital after twenty-five years. Mon Rev 43(7):52–58

Tafesse S, Girma YE, Dessalegn E (2022) Analysis of the socio-economic and environmental impacts of construction waste and management practices. Heliyon 8(3):e09169

Tooze A (2018) Crashed: how a decade of financial crises changed the world. Penguin

Trapasso C (2022) About half of black renters were priced out of homeownership in the past year. My San Antonio, Provided by Realor.com. https://www.mysanantonio.com/realestate/article/About-Half-of-Black-Renters-Were-Priced-Out-of-17388101.php. Accessed 30 Apr 2024

University of Michigan Center for Sustainable Systems (2023) Sustainability factsheets. https://css.umich.edu/sites/default/files/2023-10/2023_Bound_Factsheets.pdf

Wang Q, Su M (2020) Drivers of decoupling economic growth from carbon emission–an empirical analysis of 192 countries using decoupling model and decomposition method. Environ Impact Assess Rev 8.1. https://www.sciencedirect.com/science/article/abs/pii/S0195925519303282

Warren E (2007) The new economics of the middle class: why making ends meet has gotten harder. Testimony before senate finance committee, May 10, 2007.

Wiedmann TO, Schandl H, Lenzen M, Moran D, Suh S, West J, Kanemoto K (2015) The material footprint of nations. Proc Natl Acad Sci 112(20):6271–6276. https://doi.org/10.1073/pnas.1220362110

Young L (2022) Surging retail inventories are swamping U.S. warehouses. The Wall Street Journal. https://www.wsj.com/articles/retailers-seeking-more-warehouse-space-to-stow-excess-inventory-11659460929. Accessed 30 Apr 2024

Funding

Open access funding provided by the Carolinas Consortium.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing Interests

The author declares no competing interests.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Clark, T.P. Degrowth or secular stagnation? The political economy of monopoly finance capital and the stagnation-accumulation treadmill. J Environ Stud Sci (2024). https://doi.org/10.1007/s13412-024-00931-3

Accepted:

Published:

DOI: https://doi.org/10.1007/s13412-024-00931-3