Online first articles

Articles not assigned to an issue 224 articles

-

-

-

-

-

-

Portfolio Optimization During the COVID-19 Epidemic: Based on an Improved QBAS Algorithm and a Dynamic Mixed Frequency Model

Authors (first, second and last of 4)

-

Pricing Convertible Bonds with the Penalty TF Model Using Finite Element Method

Authors (first, second and last of 4)

-

-

-

Stability and Chaos of the Duopoly Model of Kopel: A Study Based on Symbolic Computations

Authors (first, second and last of 4)

-

Explaining Exchange Rate Forecasts with Macroeconomic Fundamentals Using Interpretive Machine Learning

Authors (first, second and last of 4)

-

An experiment with ANNs and Long-Tail Probability Ranking to Obtain Portfolios with Superior Returns

Authors

-

-

Monitoring the Dynamic Networks of Stock Returns with an Application to the Swedish Stock Market

Authors

-

-

-

-

-

-

-

-

-

-

-

-

-

Correction: Non‑linear Cointegration Test, Based on Record Counting Statistic

Authors (first, second and last of 5)

-

-

Cross-Correlation Analysis of Crude Oil-Related Stock Markets in China Caused by the Conflict Between Russia and Ukraine

Authors (first, second and last of 4)

-

-

Determinants and Pathways for Inclusive Growth in China: Investigation Based on Artificial Intelligence (AI) Algorithm

Authors (first, second and last of 4)

-

-

-

-

Calibration of Local Volatility Surfaces from Observed Market Call and Put Option Prices

Authors (first, second and last of 6)

-

Determining Drivers of Private Equity Return with Computational Approaches

Authors (first, second and last of 4)

-

-

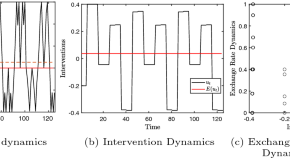

Stochastic Exchange Rate Dynamics, Intervention Dynamics and the Market Efficiency Hypothesis

Authors

-

Risk Forecasting Comparisons in Decentralized Finance: An Approach in Constant Product Market Makers

Authors

-

-

A Redefined Variance Inflation Factor: Overcoming the Limitations of the Variance Inflation Factor

Authors

-

-

-

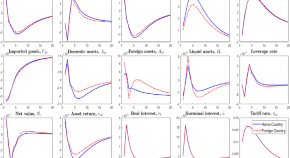

Design of Neuro-Stochastic Bayesian Networks for Nonlinear Chaotic Differential Systems in Financial Mathematics

Authors (first, second and last of 5)

-

-

-

-

Using Decision Trees to Predict Insolvency in Spanish SMEs: Is Early Warning Possible?

Authors (first, second and last of 4)

-

-