Doing Dividend Aristocrat Investing Better: 5% Yielders For The Long Term

Jose Luis Pelaez Inc

Dividend aristocrats, companies with 25-year-plus dividend growth streaks, are some of the most popular companies for income growth investors, and it’s not hard to see why.

{kind=link}

S&P

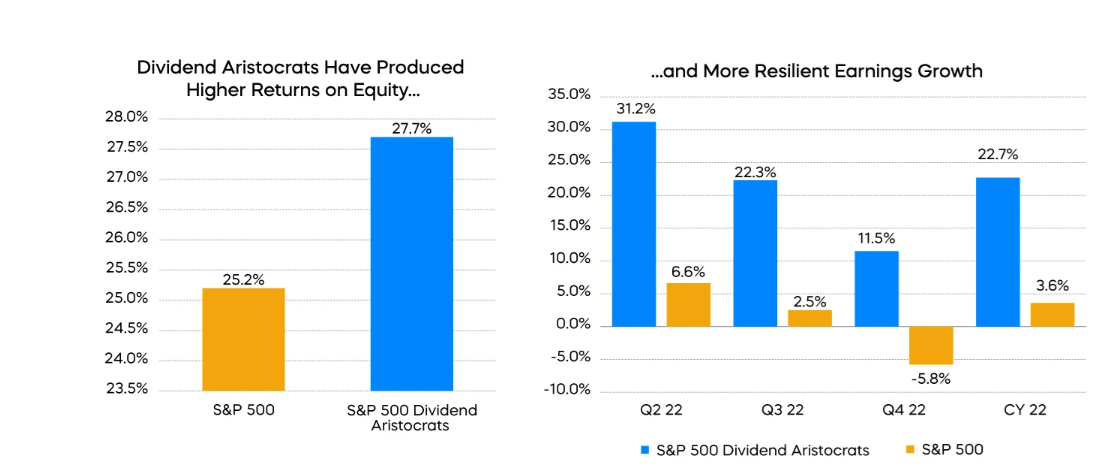

These companies have superior quality, as seen by Wall Street’s favorite quality metric, profitability.

They tend to have more stable cash flow and earnings, which is how you can sustain 25-year-plus dividend growth streaks (average is 41 years).

{kind=link}

S&P

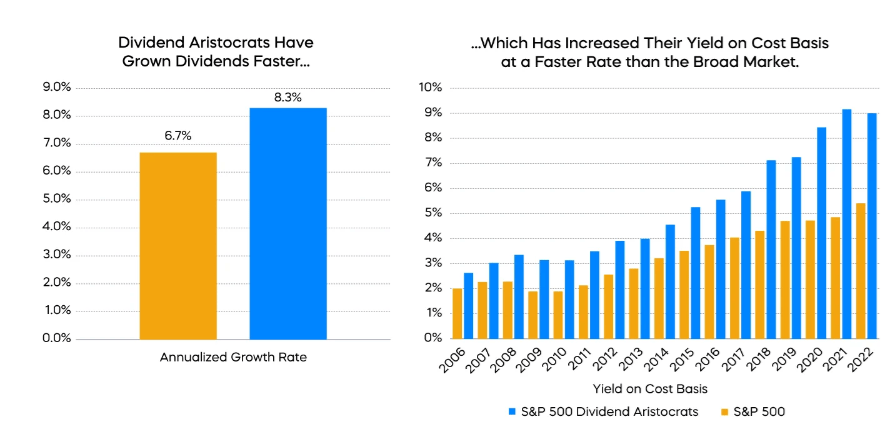

The aristocrats have delivered faster dividend growth, resulting in superior long-term income.

{kind=link}

S&P

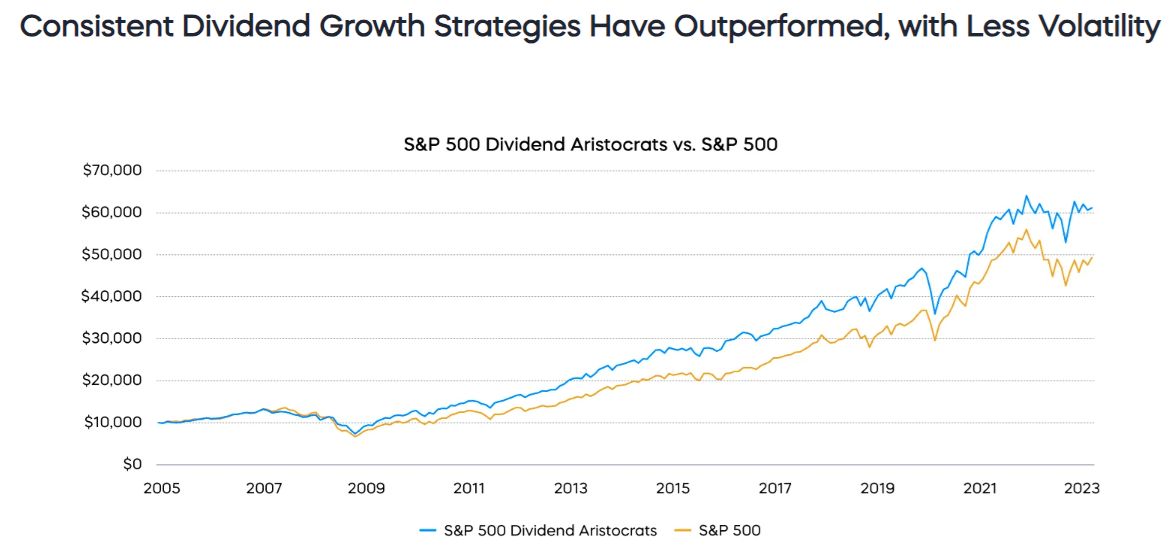

Higher dividend yield, faster dividend growth, more resilient earnings, higher quality, and higher long-term returns with lower volatility.

What’s not to love?

Limitations Of Aristocrat Investing

{kind=link}

Ploutos

While 20-year returns clearly show that alpha factors exist and some strategies can beat the market over time, there’s a significant catch.

“Long term” is longer than most people imagine.

Probability Of Alpha Factors Underperforming The S&P Since 1926

{kind=link}

Research Affiliates

Even alpha factors can underperform the market for 20 years.

They keep working over decades because investors occasionally conclude that “value is dead, all in on growth,” like during the tech bubble.

{kind=link}

MSCI

In the last decade, the only factors that beat the market were quality (profitability) and momentum.

And why was that?

The Difference Between Correlation And Causation

Quality companies are high-profitability companies. Like big tech. And what was the No. 1 sector of the last decade? Big tech.

Aristocrats have beaten the market for decades. The main reason is faster dividend growth, a function of faster earnings growth.

{kind=link}

Ritholtz Wealth Management

Yield, growth, and valuation changes ultimately drive total returns. Safety, quality, and low volatility are all merely connected to these fundamentals.

Think of it like this. The Nasdaq 100 ETF has been unbeatable for the last decade. Is that because the Nasdaq stock exchange is superior in some way to any other?

Mastercard (MA) is on the New York Stock Exchange and, thus, not on the Nasdaq. So is UnitedHealth (UNH).

Not because they’re bad companies but because they’re listed on a different exchange. The Nasdaq 100 is not a growth index. It happens to be an index with the most big tech stocks, and that’s why during the tech boom, which is likely to continue for the foreseeable future, the Nasdaq has been a great “growth” ETF to own.

Nasdaq 100 has zero growth screens, it’s just the 100 largest market cap companies on the Nasdaq stock exchange.

The dividend aristocrats are not that great of a strategy on their own because of a few fundamental limitations.

The Problem With Aristocrat Investing

The ProShares S&P Aristocrats ETF (NOBL) seems like a simple way to own aristocrats, and it is.

But there are a few critical issues with it.

First, it’s equally weighted, and its annual rebalancing means that its actual dividends are not as stable as its underlying constituents.

{kind=link}

Portfolio Visualizer Premium

An entire portfolio of aristocrats, and yet some sizeable income volatility, because of rebalancing and equal weighting.

Market-cap weighting (as most ETFs do) means bigger, more stable companies are overweight, resulting in more dependable dividends.

Imagine AT&T (T) and Walgreens (WBA) slashing their dividends and being equally important to an ETF’s income stream as Johnson & Johnson (JNJ) and Coke (KO)

NOBL Annual Growth Rates

{kind=link}

DPS = dividends per share (FactSet Research )

Because of this equal weighting strategy, NOBL has had two consecutive years of declining dividends during earnings recessions like 2016 and 2020.

Note that in 2025 and 2026, 8% EPS growth is expected.

S&P Annual Growth Rates

{kind=link}

FactSet Research

VIG Annual Growth Rates (Market Cap Weighted Aristocrats & Future Aristocrats)

{kind=link}

FactSet Research

DGRW Annual Growth Rates (Owns Meta And Other Big Tech Names That Aren’t Yet Aristocrats)

{kind=link}

FactSet Research

In other words, the aristocrat’s ETF has a growth problem. With 8% growth expected going forward and a yield of about 2%, 10% long-term returns are likely over time.

That’s compared to the S&P’s current big tech boosted 12% growth rate and 13.5% expected return.

How You Can Do Dividend Aristocrat Investing Better

There are superior dividend growth ETFs, like Vanguard’s Dividend Appreciation ETF (VIG).

However, while expected to deliver superior 12% long-term returns, VIG might still disappoint investors who expect to beat the S&P 500 as aristocrats have historically done.

This is where individual stock picking can help.

How To Find The Best Aristocrats For Your Needs In Minutes

Let me walk you through how I screen for these top aristocrats for the potential for market-beating returns in the next five years.

I begin with a core safety and quality screen, focused on safety and quality first, prudent valuation, and sound risk management.

So start with the dividend champions, all aristocrats, even foreign ones, and those not in the S&P (MLPs like EPD will never be official aristocrats).

Next, fair value or better because overpaying for a company creates a negative margin of safety and reduces future expected returns.

Next, blue-chip quality, or better, is based on our safety and quality model, which factors in over 1,000 fundamental metrics.

Then, investment grade credit ratings (BBB- or better credit rating), meaning S&P estimates an 11% or smaller risk of a company going bankrupt in the next 30 years.

S&P

Buffett considers bankruptcy risk fundamental, and I agree that this is a useful metric to always remember.

Next, eliminate turnaround speculative stocks like Walgreens, 3M (MMM), or Leggett & Platt (LEG), all recently failed aristocrats.

Now we have investment grade, non-speculative, blue-chip quality, reasonably to attractively valued aristocrats.

However, that only means high confidence in these businesses’ safety and dependability. It does not tell us anything about likely future returns.

Imagine an AAA-rated 3.3% yielding dividend aristocrat with exceptional risk management, a recession-resistant business model, and a 62-year dividend growth streak. But it’s growing at 3.4%.

That describes Johnson & Johnson (JNJ), which is expected to deliver low volatility and 6.7% long-term returns. However, it could underperform a 60-40, much less the S&P.

That’s why I will next screen for yield plus long-term median FactSet growth consensus (total return potential consensus) of 10%-plus, which is the market’s historical return.

Finally, the metric in today’s article is 5-year total return potential.

What 5-Year Consensus Total Return Potential Is And Is Not

Let me be very clear: I never make forecasts.

A 12-month fundamentally justified return potential differs from a 12-month analyst price target.

Analyst 12-month price targets are guesses about the price if their expected earnings have an X or Y multiple.

A 12-month fundamentally justified return potential means “if and only if a company grows as expected and returns to 10-year historical average market-determined fair value, this is the return that would be 100% justified by fundamentals.”

In other words, the returns you’d theoretically make if a company and the stock market did exactly the historical average and what analysts expect regarding earnings growth at this exact moment.

It’s a constantly changing target and consensus total return potential.

Fed Probabilities Are Always Changing, So Is Consensus Total Return Potential

{kind=link}

CME Group

The correct way to read this table is “based on current interest rates, the bond market is, at this very moment, estimating a 71.57% probability that the Fed will cut twice by the end of the year.”

The probability curves on Wall Street are constantly shifting.

S&P 500 75-Year Monte Carlo Simulation: 10,000 Simulations Based On 1972 to 2024 Data

{kind=link}

Portfolio Visualizer

{kind=link}

Portfolio Visualizer

Probability curves are how all professional financial advisors and institutions operate. They think about risk management and probabilities, never, ever certainties.

Five-year consensus total returns are just like bond markets pricing in 72% probability of two rate cuts by December.

Based on today’s estimates, at this exact moment, analysts expect certain growth rates for every company. And if those companies grow as expected over the next five years and return to a 10-year average historical fair value, then that’s the total return you would theoretically expect.

{kind=link}

JPMorgan Asset Management

Over five years, fundamentals explain 29% of returns, with 71% being a function of momentum, luck, and sentiment.

Now that you hopefully understand that I’m not predicting anything, I’m simply highlighting aristocrats who, per the FactSet consensus, have the potential to deliver market-beating returns over the next five years. Let’s get to the main event of this article.

5% Yielding Dividend Aristocrats That Could Double In The Next 5 Years

{kind=link}

Dividend Kings Zen Research Terminal

4.5% average yield for these aristocrats which are 18% historically undervalued and offer 27% fundamentally justified upside return potential over the next 12 months.

They have an average 96% safety score, meaning a 1% risk of dividend cuts even in another Great Recession or Pandemic lockdown economic downturn.

According to S&P, they have BBB+ stable credit ratings, 4.6% 30-year bankruptcy risk, and long-term risk management (based on over 1000 metrics) in the top 34% of global companies.

Their average dividend growth streak is 43 years since 1981.

That’s dividend hikes every year through:

- Four recessions.

- Great Recession, Pandemic, 9/11, Fastest Rate Hikes in 42 years.

- Eight bear markets, dozens of corrections, and pullbacks.

- Inflation from -3% to 15%.

- Interest Rates from 0% to 20%.

The long-term growth consensus is 7.8%, the same as the aristocrats. The difference is that a 4.5% yield is 3X more than the S&P and twice the official aristocrat ETF.

That’s why analysts expect a 4.5% yield + 7.8% growth = 12.3% long-term returns and income growth.

For those living on income, 8% dividend growth is expected, and for those reinvesting dividends, 12% to 13% income growth is expected.

The five-year consensus total return potential is 15.6% annually for the next five years, compared to the S&P’s 12.5%.

- S&P consensus: 80% potential total returns in the next five years.

- These aristocrats: 106% potential total returns in the next five years

Historical Returns Since 1998

Historical returns do not guarantee future results, but for stable blue-chip companies, historical returns and income growth can confirm whether analyst forecasts are reasonable and have increased validity.

{kind=link}

Portfolio Visualizer

12.2% annual returns, just like analysts expect in the future, with lower volatility and much smaller peak declines in the Great Recession. The negative volatility-adjusted returns (Sortino ratio) are 2x better than the S&P.

{kind=link}

Portfolio Visualizer

The worst five-year return was 3.2% per year compared to -7% annually for the S&P.

S&P’s worst five-year return was -29%, not adjusted for inflation, while the aristocrat’s worst was +17%.

The average annual return was 13%, well above the market’s 9%.

{kind=link}

Portfolio Visualizer

Conditional value at risk is basically “what does a bad month in a bear market look like,” lower volatility aristocrats historically capture just 46% of the market’s downside and 74% of the upside.

Since 1998, it has been safe to withdraw 8.5% of one’s portfolio compared to just 5% for the S&P.

Historical Income Growth: 13.1% Annually With Dividend Reinvestment

{kind=link}

Portfolio Visualizer

13% income growth with dividend reinvestment, just like the 13% average annual returns.

Total returns track income growth very closely.

Historical Income Growth: 8.1% Annually Withdrawing All Dividends

{kind=link}

Portfolio Visualizer

7.3% long-term dividend growth is expected, similar to the historical rate over the last quarter century.

Of course, the entire point of these ten high-yield aristocrats is that they’re coiled springs that won’t take decades to make investors glad they invested.

Consensus 2026 Total Return Potential

- Not a forecast.

- Consensus return potential.

- These are the expected returns if and only if these companies grow as expected and return to historical fair value by the end of 2026.

- Fundamentals would justify that.

Average: 73% = 20% annually vs 40% or 12% annually S&P.

1-Year Fundamentally Justified Upside Potential: 27% vs 8% S&P.

Altria (MO)

{kind=link}

FAST Graphs, FactSet

Enterprise Products Partners (EPD)

{kind=link}

FAST Graphs, FactSet

Enbridge (ENB)

{kind=link}

FAST Graphs, FactSet

Philip Morris International (PM)

{kind=link}

FAST Graphs, FactSet

National Fuel Gas (NFG)

{kind=link}

FAST Graphs, FactSet

NextEra Energy (NEE)

{kind=link}

FAST Graphs, FactSet

Cincinnati Financial (CINF)

{kind=link}

FAST Graphs, FactSet

Sysco (SYY)

{kind=link}

FAST Graphs, FactSet

American States Water (AWR)

{kind=link}

FAST Graphs, FactSet

PPG Industries (PPG)

{kind=link}

FAST Graphs, FactSet

Risks To Consider

The five-year consensus data we use in the Research Terminal is updated quarterly during the quarterly fundamentals updates.

We’re working on fully automating the return potential forecasts, though current technology currently makes this impossible.

For most companies, the five-year consensus return potential estimates only change from 1% to 3% for an entire year.

However, for other companies, especially those crashing or soaring due to significant changes in growth outlooks, the change can be as significant as 5% to 7% in a single quarter.

That’s why every recommendation should be considered holistically within the framework of your personal optimized portfolio.

- What are your financial goals.

- What returns and income do you need to achieve those goals?

- What asset allocation will likely achieve those returns while letting you sleep well at night (not panic sell during bear markets)?

- What ETFs do you want, if any, as the core of your portfolio?

- What individual stocks do you want, if any, to maximize the fundamentals of your portfolio that you care about most?

Hedges = 50% long bonds, 50% managed futures (Portfolio Visualizer )

Here’s an example of sound asset allocation optimization, starting backward, from the average maximum decline in bear markets since 2000 (we’ve had six of them) you wanted to experience.

Mind you, those are averages, and the results will vary in any individual bear market.

The one thing everyone cares about and that we have no control over is actual returns. We can stack the odds 97% in our favor by focusing on the fundamentals of sound investing principles and optimizing portfolios for our changing needs.

However, needs change, risk profiles change, and never forget that all finance is probability curves.

60-40 75-Year Monte Carlo Simulation: 10,000 Simulations Based On Data Since 1972

Consider the traditional 60% stock, 40% bond retirement portfolio.

{kind=link}

Portfolio Visualizer

Analysts expect 8% to 9% long-term returns from a 60-40 retirement portfolio, above the 7% historical returns it’s delivered.

However, note the wide range of outcomes, including peak declines. Anywhere from a 23% bear market to a 41% bear market (like in the Great Recession).

{kind=link}

Portfolio Visualizer

Note that there is a 10% probability that the 60-40 portfolio will suffer a greater than 41% crash in the next 75 years.

That’s how finance works. It’s a constantly shifting series of probability curves.

That’s why asset allocation and a resilient portfolio based on the optimal (never perfect, perfection is impossible, you can only approach it at any given time) is essential to sleeping well at night while achieving your goals.

{kind=link}

Brent Beshore

If this sounds scary or complex, it’s not. It’s the truth — just like the truth about businesses — that they are complex, much more than you might realize.

That’s why shareholders pay someone like Satya Nadella $50 million annually to navigate the complexities and shifting waters of running the world’s most valuable company.

The executive team at Microsoft (MSFT) makes $113 million per year, but they’re some of the world’s most skilled tech risk managers.

Shareholders pay them this fortune to stay on top of Microsoft’s more than 1,000 risk metrics.

According to S&P, almost every company has more than 1,000 things that might go wrong, risks that must be constantly adapted to.

S&P

Bottom Line: These 5% Yielding Dividend Aristocrats Could Potentially Double In The Next 5 Years

When you understand how complex the real world of business and finance is, you realize it’s unsurprising that a handful of aristocrats failed in the last few years. It’s surprising that there are any aristocrats at all.

But that’s the miracle of the stock market.

Anyone with any savings can buy part of a business — not just any business, but some of the best businesses in history.

Businesses run by skilled, adaptable, and trustworthy executives staffed by armies of skilled and intelligent workers.

All are working hard to solve problems for customers and, ultimately, the world.

This is the genius of global capitalism, and the stock market lets you harness this genius to live your dreams.

Fortunately, it’s never been easier for anyone with savings to make money while they sleep, entrusting their money with some of the greatest companies in world history.

man